Accounting is something of an art, and companies always save some accounting tricks – perfectly legitimate items that meet the discerning eye of financial standards – to goose their numbers when they really need it. When they really need to tell a turnaround story. And so it is with Intel in the second quarter of 2023.

Yes, the PC market is less horrible than it was and yes, Intel is executing to its server roadmap and is on track to compete with rival Taiwan Semiconductor Manufacturing Co within two years in terms of process technology. We said “compete with,” and we said it on purpose. Intel keeps saying it can beat TSMC on chip manufacturing with its 18A process by 2025, but TSMC keeps saying not a chance, its 2N process will whip anyone out there. (There’s only two other companies out there, Samsung and Intel.) History – backwards looking time – suggests TSMC is right, but only forward looking time (from our current point of view) lived in the moment then (in the future that will become present), will tell who is right.

As we have said before, the only perfectly accurate way to predict the future is to live it. Which is what makes life exciting.

That Intel is not doing as badly as either itself or Wall Street expected is, of course, a good thing. The IT sector needs Intel to compete, and compete well, to help drive the cost of compute in the datacenter downwards and the performance of those compute engines up. AMD has been doing a pretty good job in Intel’s stead in recent years, which is what we expect AMD’s numbers to show next week. But even with this explosion in AI spending, the underlying server market is sluggish, and even the cloud builders and hyperscalers are taking it a bit easy here in the first half of the year.

In the quarter ended in June, Intel’s posted $12.95 billion in sales, off 15.5 percent, but even after some pretty substantial cost-cutting, the company still posted an operating loss of $1.02 billion, an increase of 45.1 percent compared to the 700 million operating loss in the year-ago period. Intel had a $224 million gain from interest, which help cushion the blow a little, and posted a $2.29 billion benefit from income taxes, which switched it from what would have been a pretty big net loss to a net gain of $1.48 billion.

What matters most of course is how the underlying businesses are doing, and when it comes to Intel what we really care about are the Data Center & AI group and the Network and Edge Group.. We like when the other parts of Intel are growing and making money, of course, because that makes Intel more resilient. But what we really always care about is trying to ascertain how its “real” datacenter business is performing financially.

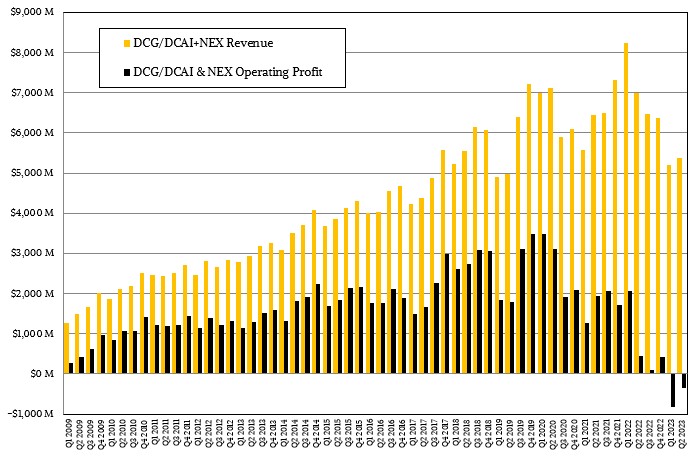

Intel merged portions of the former Accelerated Computing and Graphics group (AXG) into its DCAI and Client Computing Group (CCG) starting in the first quarter and is recasting these figures as the quarters roll on – it has not put out a summary table that goes back into the prior year as yet. So the comparisons in the chart above are a little wonky. We will fix it by January next year when the last change rolls through for Q4 2023. The next effect is that the DCAI and CCG groups have more revenue but also losses they didn’t have before – and the losses are bigger than the revenue gains.

As currently reported, The DCAI group had sales of just over $4 billion, down 14.7 billion, and this key historical profit engine for Intel had an operating loss of $161 million, a little more than double the loss from the year-ago period. That loss was driven by higher unit costs, which in turn were driven by lower factory utilization at the Intel fabs and a product mix towards more capacious (and more expensive to manufacture) compute engines.

“While we performed ahead of expectations, the Q2 consumption TAM for servers remained soft on persistent weakness across all segments, but particularly in the enterprise and rest of world where the recovery is taking longer than expected across the entire industry,” Pat Gelsinger, Intel’s chief executive officer, said on the call with Wall Street analysts. “We see the server CPU inventory digestion persisting in the second half, additionally, impacted by the near-term wallet share focus on AI accelerators rather than general purpose compute in the cloud. We expect Q3 server CPUs to modestly decline sequentially before recovering in Q4. Longer term, we see AI as TAM expansive to server CPUs and more importantly, we see our accelerated product portfolio is well positioned to gain share in 2024 and beyond.”

Gelsinger said that its datacenter AI pipeline is now over $1 billion, including Flex and Max Series GPU accelerators and Gaudi matrix math engines, and that the Gaudi chips are driving the lion’s share of this opportunity. That is not a surprise, given that the Max Series GPUs, formerly known as “Ponte Vecchio” and used in the “Aurora A21” supercomputer at Argonne National Laboratory, are very expensive to make and are being consumed almost entirely by that supercomputer at the moment. As we have said, Gaudi is going to get some supply wins as are every other kind of engine that can do AI training math because of the high cost and dearth of Nvidia GPU engines. We think AMD’s Instinct MI300 series GPUs are set to benefit more than Intel’s Max Series GPUs and Gaudi2 and Gaudi3 accelerators, but we also think that Intel could sell all of the AI compute engines it could make. The question is: Can it or will it make more?

More broadly, Gelsinger said that server buying by hyperscalers, cloud builders, and enterprises are expected to all be softer in Q3, and the recovery of the economy in China is also taking longer, so the server recession is going to go into its third consecutive quarter. AI server sales is helping, particularly with so many designs using Intel’s “Sapphire Rapids” Xeon SPs. But plenty of designs are using AMD “Milan” Epyc 7003 CPUs, and we expect to see “Genoa” Epyc 9004 series CPUs going into more AI systems as soon as volumes become more readily available.

Gelsinger said that Intel was getting ready to ship its 1 millionth Sapphire Rapids CPU, which was launched officially in January but which we think has been shipping to cloud builders and hyperscalers since about this time last year.

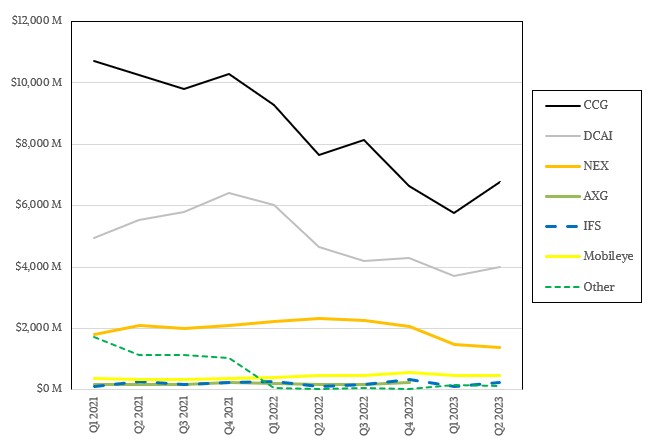

The NEX group, which has exited the datacenter switching business Intel had invested very heavily in, still does network interface cards, DPUs, and customized gear for the edge and other embedded use cases (including the Xeon D processor), had a much tougher quarter.

Revenues were down 38.3 percent to $1.36 billion, and NEX shifted from a $294 million operating profit to a $187 million operating loss in the June quarter. Ouch. Intel said that there was not as much uptake on edge use cases as it had hoped and there was softness in demand among telcos and other service providers, too. The former Altera FPGA business, which was known as the Programmable Solutions Group before it was folded into NEX last year, had its third consecutive quarter of record results since it was acquired by Intel, and that helped prop up NEX sales and profits.

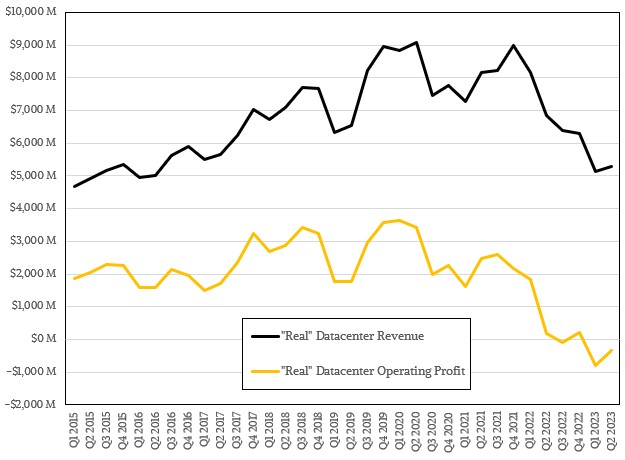

Intel dices and slices its datacenter business in a bunch of ways, and for the past eight years, we have been trying to suss out what Intel’s “real” datacenter business is. This gets trickier and tricker, but we think it is an illustration of a point as much as it is an attempt to quantify that which Intel should already do as part of its financial reporting.

Our best guess is that Intel’s real datacenter business – literally all of the stuff that ends up in datacenters and doing server-type work in the datacenter and now at the edge – came to $5.29 billion, down 22.9 percent year on year, and that operating income for this “real” datacenter business went from a $177 million gain a year ago to a $329 million loss this time around.

At its peak in 2019 and early 2020, using our old way of categorizing the datacenter, the datacenter business at Intel was pushing close to $9 billion a quarter in sales and somewhere around $3.5 billion in operating income. Just to have a sense of how far Intel has fallen here.

Wall Street might be celebrating that Intel beat expectations. But this is still pretty tough, and it looks like it will be tough slogging for a while yet. In fact, Intel may be slogging it out for the next five to ten years if its competitors stay focused and keep the heat on. They look inclined to do just that.