Anybody who can read a financial report knows they are paying too much for compute, storage, networking, and software at Amazon Web Services. It is as obvious as the sun at noon. And it is also obvious – and increasingly so – that the retailing and media businesses at Amazon are as addicted to the AWS profits and the free compute capacity it gives to the corporate Amazon parent as IBM has ever been addicted to the high price of its vaunted mainframe platforms.

And so Amazon and therefore AWS is stuck between a rock – increasing competition from Microsoft Azure and Google Cloud, and to a lesser extent Alibaba, Tencent, IBM Cloud, and a bunch of niche cloud builders – and a hard place – the desire to move back to on-premises IT operations, usually in a co-location facility to try to save money compared to buying cloud capacity and software.

In the past, in a nearly perfect illustration of the elasticity of demand for compute and storage, whenever the AWS business started to slow, the cloud arm of Amazon could cut price, wait a quarter or two, and revenues and profits would resume their growth. But now, AWS is not the only game in town, it is not the only one with sophisticated offerings, and it is not the only one cutting prices.

And the advent of utility-priced systems from Hewlett Packard Enterprise (GreenLake), Dell Technologies (Apex), Lenovo (TrueScale), Cisco Systems (Hyperflex and X-Series and Intersight) can not only take on AWS Outposts, but they can prevent them from ever being installed in the first place. As we have said before, datacenter repatriation is a real thing, and it is just as likely that large enterprises will get utility-priced hardware, software, and services and put stuff in a bunch of geographically distributed co-location facilities as they will move to one or more of the major cloud builders (or even a bunch of smaller ones).

But as in times past, we think AWS itself realizes that if it doesn’t help customers rein in their cloud spending, they will do it all by themselves. And Amazon chief financial officer Brian Olsavsky said as much on the call with Wall Street analysts going over the numbers for the fourth quarter.

“Starting back in the middle of the third quarter of 2022, we saw our year-over-year growth rates slow as enterprises of all sizes evaluated ways to optimize their cloud spending in response to the tough macroeconomic conditions,” Olsavsky explained. “As expected, these optimization efforts continued into the fourth quarter. Some of the key benefits of being in the cloud compared to managing your own data center are the ability to handle large demand swings and to optimize costs relatively quickly, especially during times of economic uncertainty. Our customers are looking for ways to save money, and we spend a lot of our time trying to help them do so. This customer focus is in our DNA and informs how we think about our customer relationships and how we will partner with them for the long term. As we look ahead, we expect these optimization efforts will continue to be a headwind to AWS growth in at least the next couple of quarters. So far in the first month of the year, AWS year-over-year revenue growth is in the mid-teens. That said, stepping back, our new customer pipeline remains healthy and robust, and there are many customers continuing to put plans in place to migrate to the cloud and commit to AWS over the long term.”

We think – and fully admit that it is just a hunch – that more than a few companies have figured out how to go multicloud and play AWS off against its cloud rivals, which often means not making use of high-value and high profit software services atop any particular cloud. Such software offers great functionality and ease of use, but it also ties you very tightly to a cloud. To keep optionality, it is wise to pick software platforms that can be deployed on any of the major clouds, that are available in the cloud stores with quick install and cloud licenses, and just use the clouds to get the least expensive compute, storage, and networking possible. We think that such behavior is also impacting AWS. It is more complex than just proactive belt tightening because of fears of an economic downturn. The belt tightening was going to come even in a boom time, given the high margins that AWS has enjoyed in recent years.

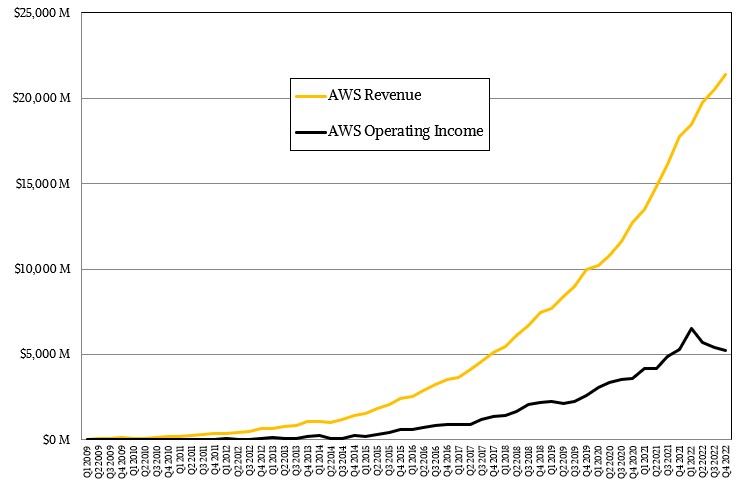

Here is just how much the top line growth has slowed since AWS was bringing in reasonable revenues in 2007:

That said, we believe the Amazon top brass when they say that companies are doing less analytics as their businesses are being impacted by the financial situation. They might be running smaller jobs for short periods of time rather than paying upfront for larger contracts for longer periods of time. This elasticity is why customers like the cloud, as Andy Jassy, Amazon’s relatively new chief executive officer who used to run AWS, correctly pointed out.

“That elasticity is very unusual,” Jassy explained, and what he said next is not precisely true anymore but you get the point. “It’s something you can’t do on-premises, which is one of the many reasons why the cloud is and AWS are very effective for customers. I have spent a fair bit of time with the AWS team on this, and we look closely at what we see. We have a very robust, healthy customer pipeline, new customers, migrations that are set to happen. A lot of companies during times of discontinuity like this will step back and think about what they want to change strategically – to be in a position to reinvent their businesses and change their customer experiences more quickly as uncertain economies emerge. And that often means moving to the cloud. We see a number of those pieces as well. And we are the only ones that really break out our cloud numbers in a more specific way. So it’s always a little bit hard to answer your question about what we see. But to our best estimations, when we look at the absolute dollar growth year-over-year, we still have significantly more absolute dollar growth than anybody else we see in this space. And I think some of that’s a function of the fact that we just have a lot more capability by a large amount, with stronger security and operational performance and a larger partner ecosystem. I think it’s also useful to remember that 90 percent to 95 percent of the global IT spend remains on-premises. And if you believe that – that equation is going to shift and flip, I don’t think on-premises will ever go away – but I really do believe in the next ten to fifteen years that most of it will be in the cloud if we continue to have the best customer experience.”

The bad news for Amazon is that this pinch is coming as the parent company is spending vast sums building its media empire and further automating and expanding its electronic retailing and grocery operations. And a $2.3 billion writeoff from Amazon’s investment in electronic truck maker Rivian Automotive certainly hurt in the fourth quarter, too, and so did a portion of the $640 million charge for layoffs announced last year that will be spread across Q4 2022 and Q1 2023.

In the quarter ended in December, AWS revenues were $21.38 billion, up 20.2 percent year on year, but operating income fell by 1.7 percent to $5.21 billion. If you look at the non-AWS parts of Amazon, combined revenues were $127.8 billion, up 6.8 percent, but these parts of the company had an operating loss of $4.93 billion, significantly worse than the $1.65 billion operating loss in the year ago period.

All told, Amazon raked in $149.2 billion in Q4 2022, and had an operating income of $2.74 billion but only a net income of $278 million. In the year ago period, Amazon had a $14.32 billion net income, with $11.47 billion of that coming from recognition of its investment in Rivian, which had gone public. The air is coming out of that tire as Rivian is struggling with quality control issues.

As we have said many times, Amazon is a platform provider and increasingly an application software provider as well as a place where companies run their own code or that of others. That software is extremely sticky, and for many, the only practical way they can get started on advanced technologies is to do so on a cloud like AWS. And frankly, for many workloads, it really comes down to choosing between AWS, Microsoft Azure, and Google Cloud. And once these workloads get strategic enough and big enough, they start looking at ways to cut the bill and better integrate disparate systems and circumvent egregious data egress charges.