Hold on a second. Nvidia’s sales of chips and systems to supercomputer centers are not as big as we might be thinking. Not even close.

Nvidia may have pioneered the idea of GPU acceleration for HPC simulation and modeling applications. It may have supplied the vast majority of the compute and, by virtue of its Mellanox acquisition, the networking in some very important pre-exascale supercomputing systems that were installed three years ago. It may have even had the dominant share of semiconductor revenues for GPU-accelerated HPC systems over many years as the idea caught on, and it may even be dominant right now, in terms of revenues, until the first waves of exascale machines based on AMD CPUs and GPUs actually get installed and the revenue is recognized after acceptance.

But none of that means that supercomputing centers are a big driver of the Nvidia datacenter business. And, as it turns out, here in the company’s fiscal 2022, supercomputing centers account for a very small portion of Nvidia’s overall revenues. A surprisingly small share, which might show just how slowly the HPC business for Nvidia has grown and just how explosive growth for AI systems has been.

In a conference call going over Nvidia’s financial results for the third quarter of fiscal 2022 ended in October, Nvidia co-founder and chief executive officer Jensen Huang had this to say when asked about the potential for growth in the datacenter and the company’s ability to lock in foundry capacity to meet the huge demand for GPUs:

“With respect to the datacenter, about half of our datacenter business comes from the cloud and cloud service providers and the other half comes from what we call enterprise – companies, and they are in all kinds of industries. And about 1 percent of it comes from supercomputing centers. So 50 percent or so cloud, 50 percent or so enterprise, and 1 percent supercomputing centers. And we expect next year for the cloud service providers to scale out their deep learning and their AI workloads really aggressively, and we are seeing that right now.”

It is important to parse what Huang said very carefully and not to conflate “supercomputing centers” with “HPC applications”. There are somewhere on the order of 3,000 government and academic supercomputing centers in the world, as far as we can tell, and we strongly suspect that the vast majority of them have not ported their applications over to hybrid CPU-GPU systems to accelerate them, even if they have some GPU accelerated nodes in their clusters. Our guess is that maybe something on the order of 5 percent to 10 percent of these supercomputing centers have GPU acceleration at any scale and as a representative portion of their overall compute capacity. That is a nice business, but it is nowhere near as big as the AI portion of Nvidia’s business, apparently.

In the call with Wall Street analysts, Huang did not break the Nvidia datacenter revenue stream down by application type – HPC simulation and modeling, AI machine learning training and inference, database acceleration (analytics and Spark databases), virtual desktops, and such – but he did say that Nvidia has over 25,000 customers who are using its AI platform for machine learning inference, and probably a similar number have been using it for machine learning training. That would imply that the AI part of the Nvidia business has a customer set that is perhaps two orders of magnitude larger in terms of customer count (but significantly less in terms of aggregate compute, we think) than its HPC business. There are some truly large GPU-accelerated HPC systems out there in the world, and they have a lot of oomph.

AI is on a hockey stick exponential growth path, and HPC seems to be growing more linearly.

Admittedly, the lines are hard to draw between sectors and markets and customers. So many of the GPU accelerated machines we do see going into HPC centers and into enterprise (in those rare moments when an enterprise lets Nvidia know – much less us – what they are doing) are really hybrid HPC/AI machines that are going to either do both HPC and AI workloads side-by-side, alternately in either space or time, or mash them up to accelerate HPC simulations with AI algorithms and techniques.

Another fuzzy line between HPC and AI is the clouds. We suspect that some of those hyperscalers and cloud builders are doing traditional HPC on their systems – Microsoft, Google, and Amazon design chips and whole systems, after all – and for the cloud builders, both in the United States and China, they are selling capacity that others may use for running HPC simulations and models as well as AI workloads.

Huang and Colette Kress, Nvidia’s chief financial officer, rattled off a bunch of interesting statistics during the call. Let’s just rattle them off for a second, and forgive us for once for using bullets:

- There are over 3 million CUDA application developers and the CUDA development tools have been downloaded over 30 million times in the past decade and a half. Which means people are keeping current.

- The company’s gaming business is going like gangbusters, and only about a quarter of the installed base has moved to the RTX architecture, so there is just a huge wave of business that can be done here. And it isn’t cryptocurrency, either.

- The cryptocurrency-specific GPUs, which do not have their hashing functions crimped, only generated $105 million of revenue in fiscal Q3, so this is not a mining bubble.

- The AI Enterprise software stack is now generally available and is certified to run atop VMware’s vSphere/ESXi server virtualization stack, making it easily consumable by enterprises.

- The Launchpad co-location stacks with partner Equinix are now available in nine different locations, and of course, all the major clouds also have GPU-accelerated gear long-since.

- In networking, demand for the former Mellanox products outstripped supply, with older 200 Gb/sec Spectrum and Quantum InfiniBand switches and ASICs and ConnectX-5 and ConnectX-6 adapter cards, and the company is poised to ramp up sales of 400 Gb/sec Quantum-2 InfiniBand and their companion ConnectX-7 adapter cards and BlueField-3 DPUs.

- No matter how skeptical you might be about GPU-based inference, the TensorRT software stack and the Triton inference server stack are being adopted by the market, and we think this is not necessarily because the GPU offers the best or cheapest inference processing, but because of its compatibility with machine learning training platforms. Nvidia says that inference revenues are growing faster than the overall growth in the datacenter business.

- There are over 700 companies that are evaluating the Omniverse 3D design and digital twin software stack, and since the open beta started in December 2020, it has been downloaded over 70,000 times. Nvidia estimates that there are over 40 million 3D designers in the world, which is, by the way, a much larger installed base than Java or PHP or C/C++ programmers individually and probably on the same order of magnitude collectively across those three languages, just to give you some scale. The Omniverse opportunity is going to accelerate the Nvidia business further, and it will be half hardware and half software.

We have been wondering why Nvidia is not more freaked out by AMD having such big wins with the exascale-class supercomputers in the United States and smaller machines around the globe in HPC centers. We have spent some time with Huang puzzling out the Omniverse opportunity, and now we understand the scope of the datacenter business. AI, and its extension and merging with HPC and other design technologies and VR/AR adjuncts is just so much more of an opportunity.

There are 300 or so hyperscalers, cloud builders, and service providers who represent more than half of the aggregate compute consumed in the world and probably a little less than half of the revenue. There are somewhere on the order of 50,000 large enterprises that do interesting things that consume most of the other half. The 3,000 or so HPC centers in the world do interesting things and are solving hard problems, but they represent only a sliver of the compute and money.

The Next Platform was founded because we knew these numbers and believed in following only the interesting stuff that happens at scale across those 53,300 organizations and for the people who work at those 53,300 organizations and those smaller organizations that want to emulate them. We have been in the trenches for so long, watching HPC accelerate with GPUs and then AI emerge as a new computing paradigm, that we didn’t see the hugeness of the Omniverse, which will obliterate such distinctions and which is such a huge opportunity that even Nvidia has trouble getting its arms around it. Huang put it this way: In the next five years, tens of millions of retail outlets will have some form of conversational AI avatar speaking to customers instead of actual human beings, who don’t want a low-paying job. The AI avatar doesn’t get tired or sick, like people do, and it will cost less than people do we suspect. And this population of virtual people will require enormous amounts of hardware and software, and companies will spend money on this just like they did 50 years ago to get rid of file clerks shuffling through file cabinets with manila folders and accountants working with pencil on greenbar in the back office. No one will talk about it that way, but it is damned well going to happen. Every avatar will have an Omniverse license, and you can bet it will cost less than health insurance for a real person, and the hardware to drive those avatars will cost less than a salary for a real person.

Against all of that, two exascale deals at the US Department of Energy worth $1.1 billion, which were going to cause a huge amount of grief and result in selling GPUs and networking at cost or below it, is not something to even worry about. Except maybe for the sake of pride. The fact is, AMD is beating Nvidia at its 2017 game. Fine. But the game has moved on, at least for Nvidia. This is something so much bigger, and it is so much more than CUDA versus ROCm, “Ampere” GPU versus “Aldebaran” GPU.

Now, let’s talk about the quarter and how the datacenter business at Nvidia did, and what Nvidia is doing to get itself in position to actually capture some of this business in a time when semiconductors are tough to get made.

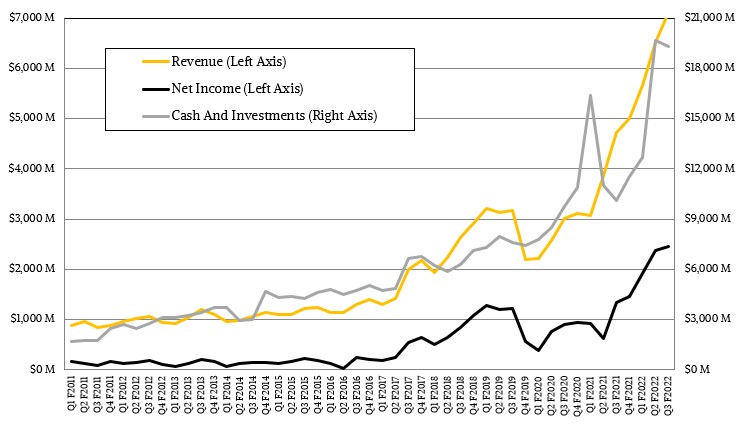

In the period ending in October, Nvidia’s revenue was up 50.3 percent to $7.1 billion, and net income rose by 84.3 percent to $2.62 billion, or 35 percent of revenue. Nvidia is sitting on $19.3 billion in cash right now, which is a little less than half the cost of its proposed acquisition of Arm Holdings, which is going to be bought mostly with stock anyway. So that cash is just there, ready to be deployed. And it doesn’t matter if the Arm deal fails. It opens up some interesting possibilities for Arm and for Nvidia, but all we really need from Nvidia is a great server chip, as the “Grace” processor for HPC/AI workloads could be when it comes out in 2023.

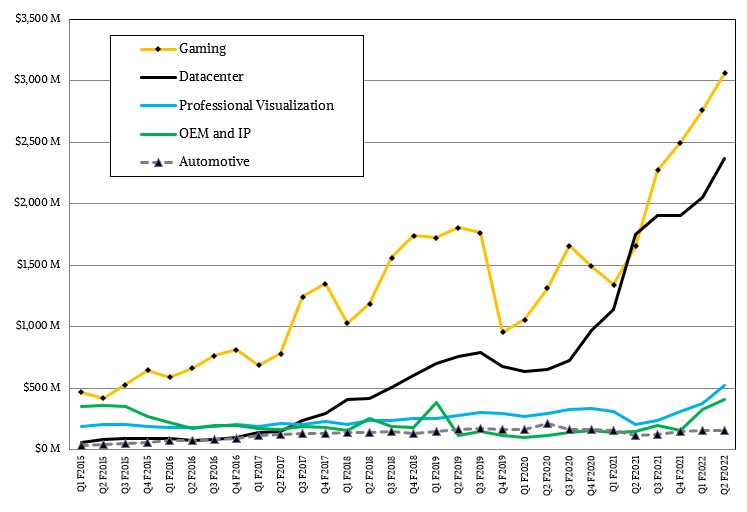

The Datacenter division at Nvidia had $2.94 billion in sales, up 54.5 percent year on year, and up 24 percent sequentially. The Gaming division saw a 41.8 percent increase to $3.22 billion in Q3, while the Professional Visualization division, thanks to people working from home, saw a 2.45X increase year on year to $577 million as shiny new desktop workstations and laptop workstations became the new, well, workstation from home for many people.

The datacenter business grew across the hyperscalers and the enterprise customers, and sales to hyperscalers rose by 2X year on year. Which means the enterprise growth was modest by comparison for the whole datacenter business to “only” be up by 54.5 percent. It depends on where Nvidia draws the line between hyperscalers and big clouds, which are in that hyperscaler category, and “consumer internet and broader cloud providers,” which are part of the vertical industries/enterprise category the way Nvidia talks about its business.

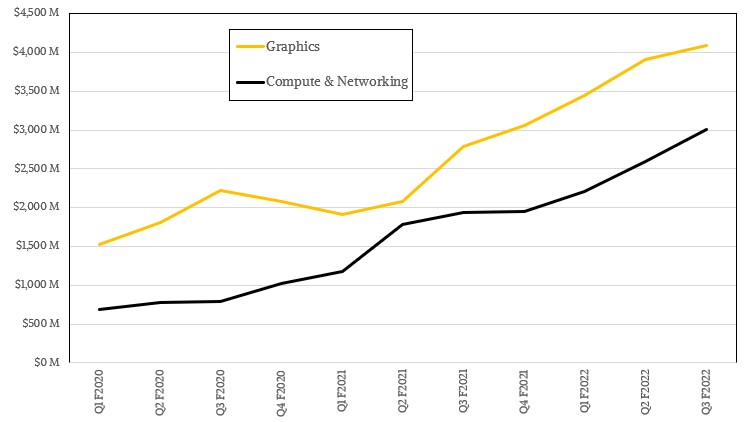

Since Q1 of fiscal 2021 and backcasting a year before that, Nvidia has been breaking its revenues into two groups: Graphics in one big bucket and then Compute & Networking in another big bucket. Like this:

In the quarter just ended, Graphics products had sales of $4.09 billion, up 46.8 percent, while Compute & Networking had sales of $3.01 billion, up 55.3 percent. Nvidia used to give out operating income for these two groups, but to our chagrin has stopped. Perhaps it was because Compute & Networking was not nearly as profitable as Graphics, which seems a bit backwards until you realize how badly gamers and designers want great graphics cards. They will pay a premium for performance – if they can get their hands on it – unlike a hyperscaler, who will not and they know they can get their hands on it because that is one sure way to get high volume for Nvidia.