It is hard to keep a model of datacenter infrastructure spending in your head at the same time you want to look at trends in cloud and on-premises spending as well as keep score among the key IT suppliers to figure out who is winning and who is losing. And so we have built a model that does this, and we are calling it the Datacenter Infrastructure Report Card.

We are not going to be delivering letter or number grades to vendors, because money is how you keep score and that is the only metric that matters in any market in the final analysis. And specifically, we have lined up the quarterly results of the key suppliers in the datacenter – those that sell compute engine chips, OEM systems and related storage and core systems software, datacenter networking, and raw cloud infrastructure capacity – that make up the backbone of the datacenter these days.

This is meant to be fun as well as illustrative. We will continue to provide individual and detailed financial analysis for each other these companies (and others) but will bring the summary datacenter revenue and operating profit streams from these thirteen vendors across these four categories once the last of this group posts its financial results for any given calendar quarter.

Dell, Hewlett Packard Enterprise, and Nvidia have quarters that end at weird times, and we have placed their results for their most recent quarters into the third calendar quarter of 2023 to get everyone lined up on Q3. We realize this is imprecise, but there is no way to figure out how to cut up their quarters and allocate them to calendar quarters. These companies could do us all a favor and just have calendar quarters.

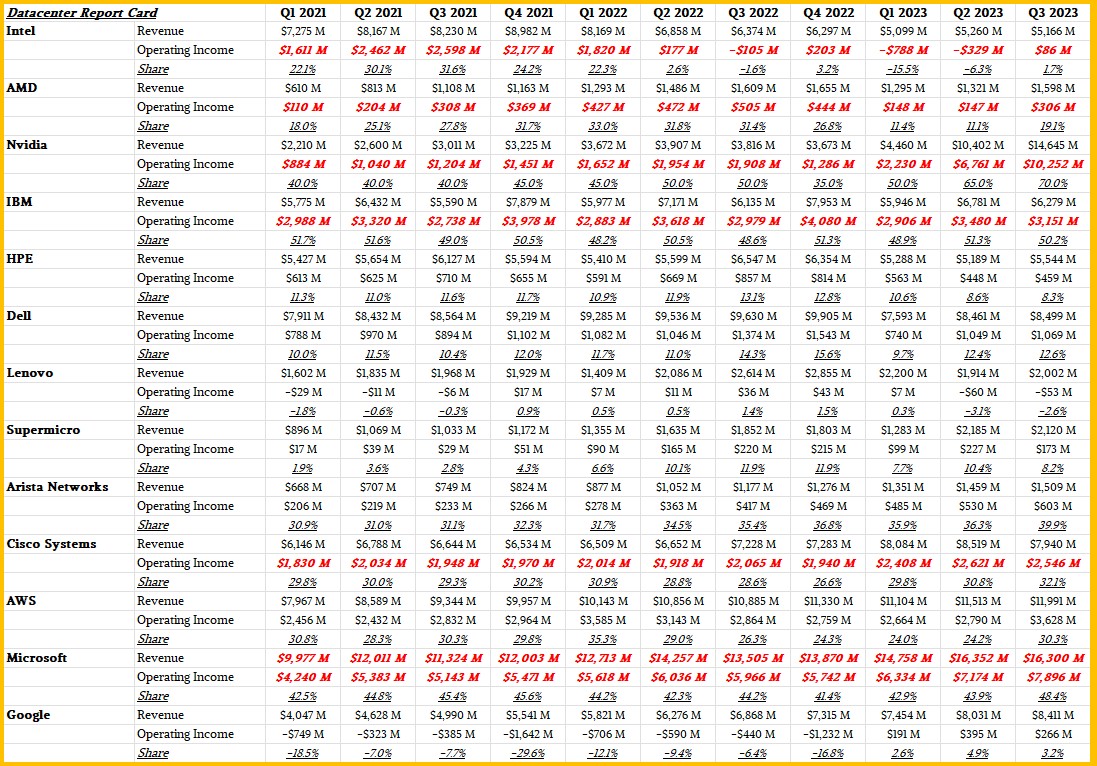

In many cases, vendors provide revenue and operating profit figures for their datacenter divisions. Sometimes they do not provide revenues for datacenter sales and we have to estimate them (as we have long done with IBM and Intel, for instance, call it their “real” systems businesses, for instance). Sometimes vendors do not provide operating income for their datacenter divisions and we have to take our best guess at allocating operating profit or loss from the overall company to the datacenter products. Anything in the table below marked in bold red italics is estimated.

Microsoft, for instance, is all in red in our model, but that does not mean it is a wild guess. Big Bill has a division called Intelligent Cloud that includes Windows Server, SQL Server, Visual Studio, and other middleware and tools sold into the datacenter, including compute, storage, and networking capacity on the Azure cloud and related platforms and SaaS services Microsoft peddles into the datacenter.

We looked up market studies about database management system revenues and share for Microsoft, and the same for application development tools, and backed this out of the Intelligent Cloud revenue stream to arrive at what we think of as Microsoft’s core systems sales across on premises and Azure. We allocated operating income proportionally to revenue because we have no better guide, and we think that profits from the Windows Server stack go a long way to cushioning the blow to operating income from massive investments in infrastructure for Microsoft. Which is something Google does not have and that Amazon Web Services only has a bit of. You will no doubt see this in the numbers.

We have no easy way to extract the Windows Server platform revenue stream from the Azure cloud revenue stream, and so we have left them together for Microsoft in the cloud infrastructure supplier comparison charts. We reckon at this point, about half of the core systems part of the Intelligent Cloud business is for on premises Windows Server and the other half is for raw cloud infrastructure – that is a valid guess based on market trends, but a guess. But arguably, half of Microsoft’s revenues and profits could be considered in the OEM systems camp and half in the cloud camp.

We think these vendors are representative for key trends, but realize they are not the totality of the market. But they do show who is making revenue and who is getting to keep how much money.

Here’s the big table of datacenter revenue and operating profit for the Thundering Thirteen:

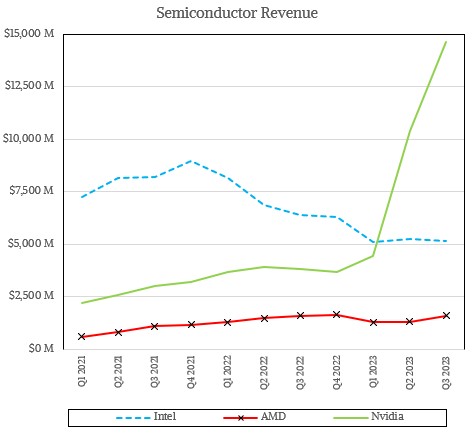

Maybe you are like a large language model and you can take that all in at once, but we need to chew on it with little bites. Let’s look at the three key compute engine makers – Intel, AMD, and Nvidia – first. Take a gander at this:

This chart does not show the full decline that Intel has absorbed, just the past eleven quarters, and you really need to appreciate how difficult it has been for AMD to keep growing its compute engine sales in the datacenter as we have been in a server recession – outside of AI servers, of course – this year. That Intel has been able to level off to around $5 billion in datacenter revenues and that AMD is growing through $1.5 billion a quarter and is on track to kiss $2 billion before too long is remarkable. AMD will be propelled by explosive GPU sales and improving CPU sales, and Intel is not really expected to see much of a CPU or GPU bump until perhaps “Granite Rapids” CPUs next year and maybe its “Falcon Shores” accelerator that comes out after 2025.

Nvidia is just off the charts as the LLM revolution is propelling the most dramatic change in system architecture in the more than five decades of corporate computing.

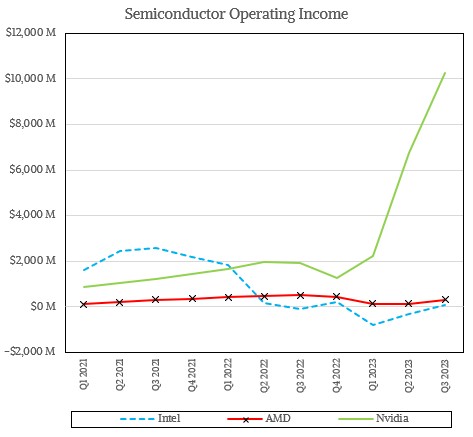

Revenue is one thing, but operating profit is a related and yet different thing. And it is different for each of these three chip makers:

Intel, which used to command operating profits of around 50 percent in its datacenter business has spent the past six quarters at close to breakeven or under water, losing money at the operating level and no doubt losing even more money at the net income level. (Which we are not going to try to calculate for the Thundering Thirteen.)

The OEM system makers, especially those that just push tin instead of having their own big iron hardware, software, and services stacks in the datacenter, have a hard time getting the kind of revenues Nvidia now sees and that Intel used to see and cannot command much of a profit.

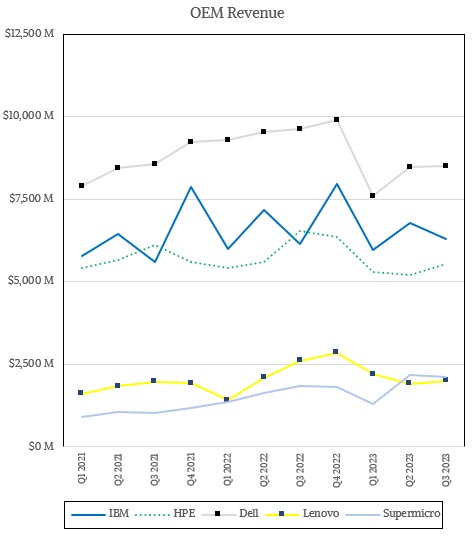

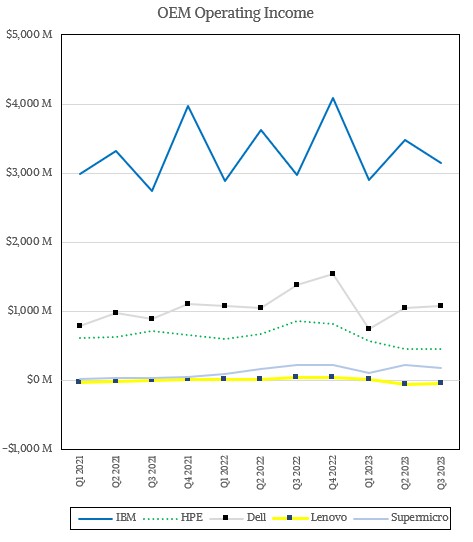

Here are the trendlines for the key system OEMs, which is IBM, HPE, Dell, Lenovo, and Supermicro:

Dell is the undisputed OEM system maker leader by both volumes and revenues, but with the X86 server recession underway, Dell has been hit hard just like HPE has been. And while HPE has been helped in 2022 by its supercomputer sales, and is getting a bit of a bump this year, too, the sales of these other kinds of big iron do not yield much in the way of profits for HPE – just as they did not for IBM, which exited the capability-class supercomputer business for this reason four years ago. Supermicro has grown steadily to give Lenovo a run for the datacenter money, but Supermicro is only moderately profitable and Lenovo has been under water in its systems business for the past two quarters.

IBM has trimmed down to its core System z and Power Systems essentials and added the Red Hat stack, and this operating profit chart shows why:

The IBM numbers include sales for core servers and system software (including Red Hat Enterprise Linux for its own and other machines) but do not include any higher level software such as middleware, database, or application software. As you can see, IBM is by far the most profitable of the OEM system makers, and illustrates the benefit of controlling a full stack with decades of customer experience that is hard to walk away from.

As we have said many times, being an OEM system maker is a very tough business when it comes to turning a profit, and adding HPC clusters does not help on that front. (Being one of the giant ODMs in Asia is no easier, by the way. Imagine having Google, Amazon Web Services, Microsoft, or Meta Platforms as your swing customer. Who owns whom?

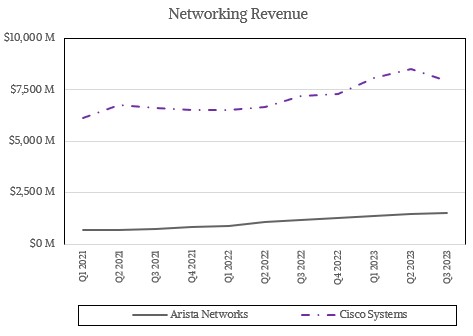

Two companies set the pace for networking in the datacenter, and they are of course Cisco Systems and its archrival, Arista Networks. And they are about as regular as regular can be in 2023:

These revenue streams include campus as well as datacenter and edge networking products, and at some point we may try to sort through these to get a cleaner and purer datacenter trendline.

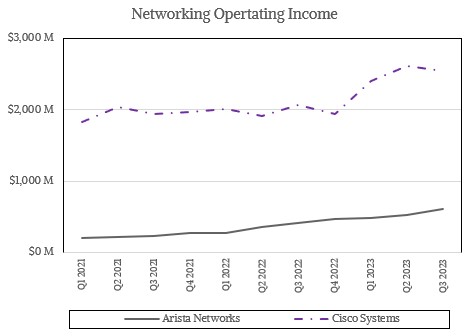

Here is how Cisco Systems and Arista Networks have done in terms of operating profit in the past three years:

As you can see from the chart above, both Cisco and Arista are growing their operating profits in their networking businesses faster than their revenues, which is usually a sign of a healthy market with healthy competition and cost control.

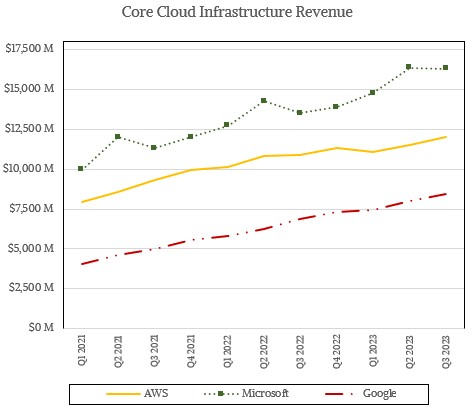

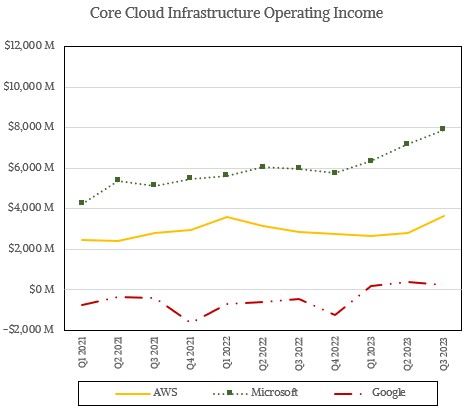

And that brings us to cloud infrastructure, for which we think AWS, Microsoft, and Google are the bellwethers.

If you include the on premises Windows Server stack sales with the Azure cloud infrastructure sales as we talked about above, then Microsoft has a bigger datacenter business that it has been building since 1993 than AWS has been able to build since 2006. It remains to be seen if Microsoft will continue to grow as it has or if AWS will pass it. So far, they are more or less tracking each other’s growth, and if there is a big shift to off premises datacenter infrastructure, Microsoft is well positioned to capture that customer motion and retain those customers.

Google, which arguably invented the second generation of corporate distributed computing in the datacenter, is tracking Microsoft and AWS but does not look like it will suddenly have a breakout revenue spike due to some technology or pricing advantage. And Google Cloud has only recently moved into an operating profit, as you can see below:

By the way, all of this profitability in 2023 for all three is being driven by the use of GPUs to train generative AI models and to run inference for applications in some cases. Without that GenAI bump, Google Cloud would probably still be underwater – even after changing accounting rules to extend their server lifetimes as both Amazon and Microsoft have also done to have better operating profits than they might otherwise have.

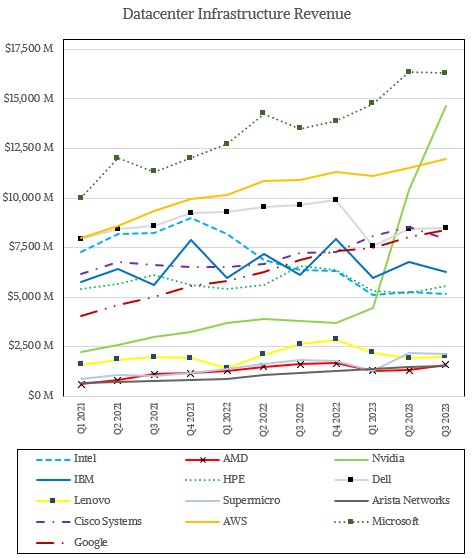

Now here is where the fun begins and you go a bit cross-eyed. Let’s put the revenues for all of the Thundering Thirteen onto the same chart:

With that, you see that Microsoft is the biggest player in the datacenter, with AWS being outpaced by Nvidia in the past two quarters to be the number two player. Dell, Cisco Systems, and Google Cloud are neck and neck at this point.

IBM has slipped down a bit away from this pack as it enters the end of its Power10 and System z16 product cycles and won’t have another bump until Power11 and z16 come in 2025. Intel is trending along with HPE, below IBM, and Lenovo, Supermicro, AMD, and Arista Networks are running together as the second position players in the datacenter in their categories.

Weird alignment, right? It is a bit of the Pareto Principle mixed with heaven only knows what.

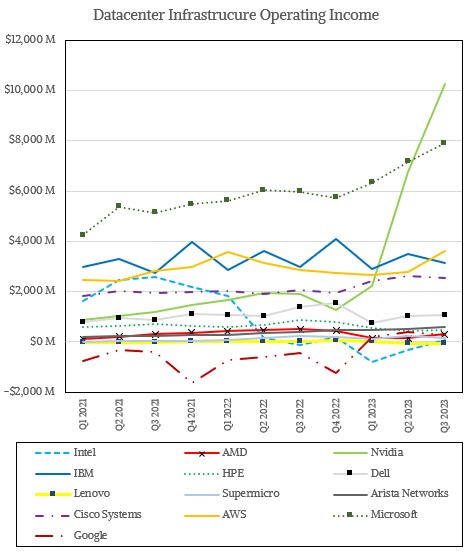

Profits tell a different story across the Thundering Thirteen:

Microsoft has been usurped by Nvidia, and by a signification margin, when it comes to datacenter operating profits. IBM, AWS, and Cisco Systems are trending more or less together, and the rest of the pack is hovering way to close to breakeven by comparison.