In the wake of the Technology and Manufacturing Day event that Intel hosted last month, we were pondering this week about what effect the tick-tock-clock method of advancing chip designs and manufacturing processes might have on the Xeon server chip line from Intel, and we suggested that it might close the gaps between the Core client chips and the Xeons. It turns out that Intel is not only going to close the gaps, but reverse them and put the Xeons on the leading edge.

To be precise, Brian Krzanich, Intel’s chief financial officer, and Robert Swan, the company’s chief financial officer, said on a call with Wall Street analysts going over the first quarter 2017 numbers that Data Center Group would be a fast follower on 10 nanometer process node and would come out ahead of the client chips with the 7 nanometer node. This represents anywhere from a two year to two and a half year acceleration of the Xeon processor roadmap in terms of historical trends, as we discussed in that related story that we did earlier in the week about mapping the Xeon chips to the new tick-tock-clock method.

The immediate impact, as Intel explained to Wall Street, is that the development and ramping costs for 10 nanometer and 7 nanometer processes are being more heavily allocated to Data Center Group and not being put as a heavier burden on the Client Computing Group that makes chips for desktops and laptops, which has historically had a lead of anywhere from 18 to 24 months on Xeons in getting a process. Intel used the high volumes of the PC group to drive down the costs of a process, but now, because of increasing demands for more compute from high end hyperscale and HPC customers and because of increasing – and now credible – competition entering the field from AMD and the ARM collective.

So, the datacenter compute price war will be augmented with a process war, and that is one that Intel can demonstrate it has been winning and can continue to win.

The other effect of this process switcheroo is that the profitability of Client Computing Group will rise, since it is not shouldering more of the costs of developing and ramping each process node as it has been doing. Swan said on the call with Wall Street that operating income for Data Center Group was down by 9 percent in the quarter, year on year, and that 7 percent of that decline was due to the shift in allocation of costs for 10 nanometer ramping and 7 nanometer development. Operating income for Data Center Group stood at 35.1 percent of sales for the first quarter, down from 44.1 percent in Q1 2016. Data Center Group revenues were up 5.8 percent to 4.23 billion, and operating income came in at $1.49 billion, down 15.7 percent. Over the long haul, Intel things that operating income for Data Center Group will settle in at somewhere between 40 percent and 45 percent of revenues, down from the 50 percent or more it has been traditionally been able to extract.

So one other effect of this change will be that the Xeon server business will look a little less juicy than it has, and it will also be less able to maneuver in a competitive datacenter price war. Then again, once could say that this change was compelled by that coming war.

The first volley comes with the Skylake Xeon E5 processors, which Krzanich said would have a “mid-summer launch.” Summer runs from June 21 to September 21, so the end of July to early August seems likely if that means what we think it means.

Intel is counting on a pretty significant ramp for the Skylake Xeons to get the Data Center Group back on track for “high single digit growth” for Data Center Group for the full 2017 year. “From the standpoint, we have been sampling Skylake to the cloud guys now for some period of time – in fact, back into the latter half of last year,” Krzanich explained. “But you really don’t see the ramp of Skylake in volume at any of the customers, whether it be the cloud guys or the rest of the enterprise and networking and all, until the second half. That is really when the volume kicks in on the server side, and that is absolutely what we had forecasted and there is no change in that forecast whatsoever.”

This is a pretty heady scenario if you do some projecting. If you assume that the target Intel wants to hit is 8 percent growth for Data Center Group, and you assume pretty flat sales in Q2 – maybe 5 percent revenue growth – and similarly low operating profits – maybe 35 percent of revenue – and then an acceleration in the third and fourth quarters, Intel has to have a tiny bit above 10 percent revenue growth on average in the second half and operating profits north of 44 percent, or a little better than it did in 2016 for the full year without the burden of putting the Xeons on the front line of processes and allocating more costs to them. If Intel can do what we think it is trying to do, it will have 8 percent revenue growth in Data Center Group, to $18.6 billion, and operating income of $7.47 billion, down a smidgen and representing 40 percent of those revenues.

This assumes that ARM and AMD don’t get much traction in the face of the Skylake ramp. We shall see about that.

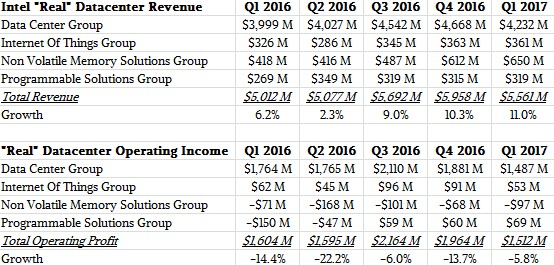

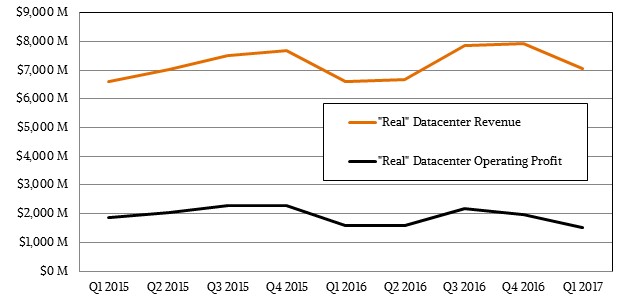

Intel’s “real” datacenter business is a lot larger than what it reports in Data Center Group, of course. It sells IoT gear into glass houses, it sells FPGAs to enterprise, hyperscale, HPC, and cloud customers, and it sells flash drives and sticks to the same customers, too. We like to take a stab at figuring out what the real Intel datacenter business might look like, and if you allocate 50 percent of IoT revenues and 75 percent of non-volatile storage and FPGA sales to enterprises and then add in the actual Data Center Group, here is what it looks like for the past five quarters:

This aggregate business is growing much faster than the Data Center Group as reported, thanks to the ramp of flash storage, and 3D XPoint memory with the Optane brand will help here, too, when it starts shipping in volume with what we presume will be pretty high margins. The operating profits for these businesses are, however, under pressure as Intel makes substantial investments in its memory business and the IoT business is not particular large or profitable yet. But it is growing fast and is larger and more profitable than the FPGA business that Intel spent $16.7 billion to acquire.

In the trailing twelve months, this real datacenter business at Intel has brought in $22.29 billion in revenues and $7.23 billion in operating income. Over that same twelve month period, the entirety of Intel brought in $60.48 billion in sales and $13.91 billion in operating profit.