The only number you need to remember about Intel’s Data Center Group business for the next three years is this one: 15 percent. That is the annual growth rate that general manager Diane Bryant says that the company can deliver, on a compound annual growth rate basis, “out through time,” although the presentations that the top brass from Data Center Group only did comparisons between 2014 and 2018.

To deliver such growth – and consistently year after year, given the uncertainties of the global economy and the tectonic shifts taking place in the datacenters of the world – would be a truly remarkable feat. Assuming that Intel makes its numbers for 2015 and grows Data Center Group revenues by 15 percent, the company has averaged 17.7 percent growth, with a few blips up and down from that average, and even more significantly, has been able to grow its operating income at nearly twice that rate.

Bryant did not mention this statistic at a recent Data Center Day event help for Wall Street analysts, but any time a company can grow operating earnings twice as fast as revenues – and for that matter grow a hardware business at anything approaching 15 percent in a mature market – that company is on to something. But the company has plans to expand its total addressable market, accelerating the buildout of public and private clouds with its Cloud for All initiative, getting a bigger chunk of the datacenter networking market proper through its Omni-Path and Ethernet products, and transitioning the fleets of specialized gear used by telecommunications and service providers to Xeon and, we think, possibly hybrid Xeon-FPGA architectures.

But make no mistake about it. Bryant was clear that Intel will also need for enterprises to keep upgrading their own server fleets, particularly since they account for somewhere north of 40 percent of the Data Center Group’s revenues these days. We suspect that enterprises also account for a slightly higher share of the Data Center Group’s operating income, given the volume leverage that hyperscalers and cloud builders have and that most enterprises do not.

Intel had a blip in enterprise sales in the second quarter, but had a first quarter that exceeded expectations and therefore Bryant thinks Intel can still hit its goal of boosting Data Center Group revenues by 15 percent this year. She added that China is part of the problem, which buys a lot of four-socket and eight-socket Xeon iron and has for years, but this slowed down. (The word we have heard is that many Chinese companies bought half-populated four-socket machines, leaving room to add CPUs in the future. Maybe Chinese hyperscalers are finally doing the math on this one and realizing they do not upgrade processors as much as they thought they might.) “We are keeping our eye on that, but the underlying growth drivers remain the same, and we are still confident on the year,” Bryant affirmed.

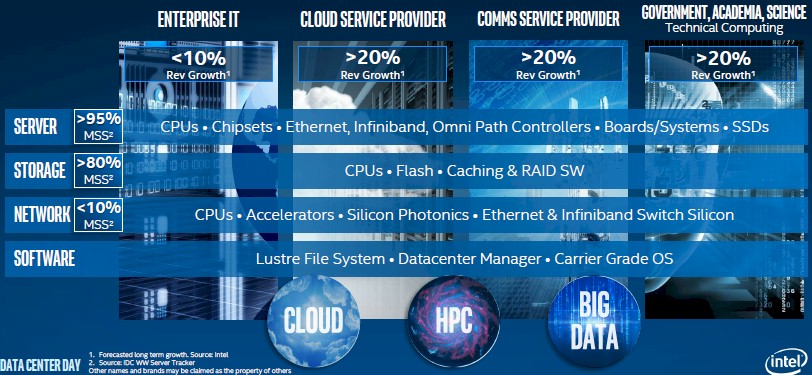

Here is how Bryant characterized Data Center Group’s current market share and growth trajectories based on product sets and markets:

Processors based on the Intel X86 architecture have account for an astounding 99.1 percent share of server shipments and 80.1 percent of revenues, according to the latest stats from box counter IDC. Intel’s chart above merely says it has more than 95 percent share and Bryant said it was 96 percent in her presentation, which occurred just after IDC released its Q2 2015 server statistics. The point is, Intel has this one nailed, and the fact that even 20 percent of the server base is using non-X86 architectures is a testament to the staying capacity of the applications that run on those machines – mostly in large enterprises, mostly running big databases and the back office applications that run on them. (Not exclusively, mind you.)

Back in the mid-2000s, Intel’s share of processing for storage arrays was in the range of 20 percent or so, but it has grown so fast that Intel now has more than 80 percent shipment market share for silicon for the controller brains in storage arrays. While many NAS and SAN storage arrays were based on Power, MIPS, or proprietary chip architectures only a decade ago, almost all of them have ported over to Xeon chips and the new breed of upstarts selling hybrid disk-flash or all-flash arrays use Xeons as their controllers. (There are a few exceptions, but not many.) As a fairly large amount of storage capacity is being sold on beefy servers running open source object, block, and file systems – in the latest quarter, original design manufacturers accounted for 13.3 exabytes of storage, or about 43.8 percent of the total 30.3 exabytes of capacity shipped. The Intel platform is benefiting from this shift, but again, the money goes away. Those ODM server-storage hybrids only generated around $1 billion in revenues, and when you do the math, this ODM storage is about one-sixth the cost of storage with a brand on it.

Intel’s share of the global networking is at 8 percent, Bryant said, and presumably this is some measure of shipments to be consistent with the other data presented for servers and storage. The networking business is the real growth opportunity for Intel, with such a small share, but incumbents like Cisco Systems and Hewlett-Packard, which still make their own network ASICs for some of their products, and rivals such as Broadcom and Cavium Networks (which are driving the new 25G Ethernet standards) and Mellanox Technologies (which is out in front with 100 Gb/sec Ethernet and InfiniBand products) are not going to let Intel take their business without a fight.

“We love the old days of enterprise IT, very predictable buying patterns. We have twenty years of seasonal buying patterns of enterprise IT, and so we could nail each quarter with great predictability. The cloud market, the public could service provider market is much harder to predict, and they will even say they struggle to predict. They’re tuning their algorithms all the time. They’re deploying more infrastructure all the time. They’re trying to gauge how much capacity they need because it’s a big capex spend. They don’t want to spend without the demand being there. So they even have trouble anticipating what next quarter’s demand is going to be.”

Expansion in storage and networking is not just limited to the corporate datacenter, but also to the parallel universe where service providers still use mountains of proprietary gear to deal with voice, data, video, and other streams of data on behalf of consumers, governments, and corporations.

It is hard to draw lines between the categories, and we all know this. “When we say the move to cloud computing, we mean that as a computing architecture,” explained Bryant. “So it is the move to cloud computing of the big public cloud service providers, enterprise moving to private clouds, the communications industry moving to a cloud-based infrastructure. So we mean it as a computing architecture that is pervasive.”

For the past year, Intel has been talking up Jevons Paradox, which basically says that the consumption of a commodity, like coal or computing, can behave elastically if it is made easier to consume. Rather than keeping the usage of the resource the same, people find other uses for the resource even as their use of that resource becomes more efficient. As we have pointed out before, the worldwide server base has increased by about a third in the past decade, but the amount of compute in a server has gone up by several orders of magnitude. This is more or less elastic behavior. Intel is not answering the question of whether or not this can hold forever, and wants to accelerate consumption, not wanting to wait for cloud hardware spending to double between 2014 and 2019. Intel wants to get tens of thousands of organizations worldwide on cloudy infrastructure earlier than that.

Don’t get the wrong impression. The cloud (or cloud plus hyperscale, as we use those definitions here at The Next Platform) has not been a bad business for Intel. Up until now, Intel has identified the big four in the United States – Google, Amazon, Facebook, and Microsoft – and the big three in China – Baidu, Alibaba and Tencent – as the key drivers in its cloud segment. This time, Bryant said that there are more like ten biggies, with JD.com (an online retailer) and Qihoo 360 (a provider of antivirus and security software) added to the mix from China as bulk buyers of compute. The interesting bit is that on a worldwide basis, about two-thirds of cloud infrastructure based on Intel technology is going into consumer-facing clouds and the remaining third is for running enterprise-class services and raw infrastructure for their own applications. “That mix has been pretty constant over time,” Bryant said.

As you can see in the chart above, the enterprise IT sector is the laggard, and is forecast to grow at under 10 percent. The other three pillars of the Intel business – cloud service provider, comms service provider, and technical computing – are all growing at more than 20 percent, making up a lot of the difference to hit that 15 percent growth figure.

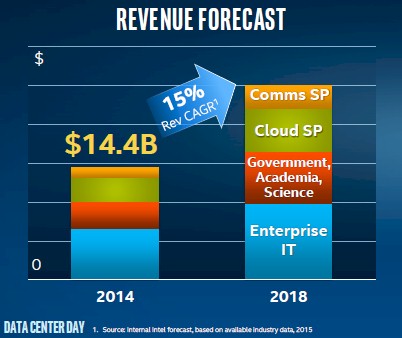

Making forecasts is a tough business, and back in 2011, when Kirk Skaugen was running the Data Center Group, the company was projecting that it would hit $20 billion in revenues by 2015. (It took Intel a decade between 2000 and 2010 to hit $10 billion in revenues for this key part of its business.) This forecast was subsequently revised by Bryant in 2013 after an enterprise spending slowdown that we think is absolutely tied to cloud computing architectures (companies buying public cloud capacity and making their own infrastructure more orchestrated and efficient). If Intel hits its 15 percent growth target for 2015, it should hit $16.6 billion in sales for Data Center Group and if all other trends persist, it should bring in $8.4 billion in operating income from these products.

Intel did not put numbers on its axes, but in the chart above, enterprise was about $6.7 billion in revenues, with technical computing accounting for about $3.3 billion, cloud service providers accounting for about $3.2 billion, and communications service providers accounting for $1.2 billion, adding up to $14.4 billion. Looking ahead to 2018, Intel is forecasting that it will hit $25 billion in sales, with enterprise IT accounting for just under $10 billion and revenues from technical computing nearly doubling, comms service providers more than doubling, and cloud service providers growing more modestly but also up around maybe 75 percent. (It is hard to estimate from these charts, but we tried.)

The levers that Intel will be pulling to hit its growth forecast are many. The first is to ride up the transition in the Xeon product line as more and more customers forego the basic SKUs in its lineup and move to more standard SKUs that have more features and also cost more. Compared to 2010, about 80 percent of the CPU volume sold by Intel has “moved up the stack,” with the top of the stack being the 39 custom CPUs that the company has etched for hyperscalers and system suppliers for a premium; Intel already has ten custom “Broadwell” Xeon designs, with Facebook having input on the Xeon D processor for microservers that was revealed in March and that will begin shipping in volume shortly.

Intel will also pull the cloud lever hard to accelerate those cloud transitions at the 50,000 or so large enterprises in the world, boosting its share in the networking space, converting comms service providers to server-based Xeon gear instead of fixed function appliances, and selling more flash and now 3D XPoint memory in servers, storage, and networking. The way Intel sees it, the advent of 3D XPoint memory alone expands its total addressable market from $37 billion for just logic chips to $49 billion including logic and memory applicable to its markets.

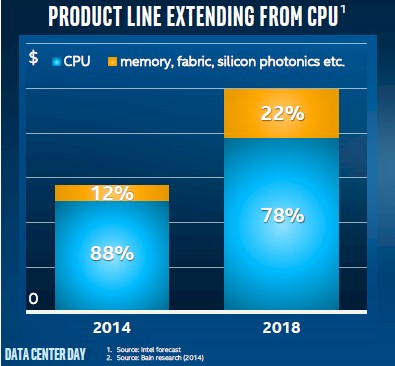

While Intel will still be predominantly a vendor of processors and chipsets, the company is forecasting that by 2018 about $5.5 billion in its revenues will come from chipsets, system boards, Ethernet and Omni-Path controllers and switches, silicon photonics interconnects, and whole machines coming out of its Systems Group. The remaining $19.5 billion will come from CPUs like the Xeon E5s and E7s, although those product categories will probably not be there by then, and possibly FPGAs once it closes its $16.7 billion acquisition of Altera. (It was not clear from Bryant’s presentation if FPGAs were classified as CPU or Other.)

Intel’s strategy involves a lot of different technologies and divisions, and we will be analyzing them since they affect many aspects of The Next Platforms that companies are building.