NEXTPLATFORM AD

HPE Works Harder And Smarter To Chase Datacenter Profits

The compute engine and networking ASIC makers are profiting mightily from the GenAI boom, and so is Taiwan Semiconductor Manufacturing Co, the world’s largest and most important foundry. Everyone else downstream from them has a very tough time squeezing profits from sales. Even if business is up, costs for memory and flash are going up faster, and companies like Hewlett Packard have to work harder to find and select profitable deals. And they have to walk away from deals that do not make sense economically.

Every quarter for many years now, we look at the financials of maybe two dozen key, publicly traded IT suppliers to try to ascertain how their datacenter businesses are doing so we can give you a better sense of what is going on out there as you navigate the churning seas of the GenAI boom and try to negotiate around some rocks below the water line.

NEXTPLATFORM AD

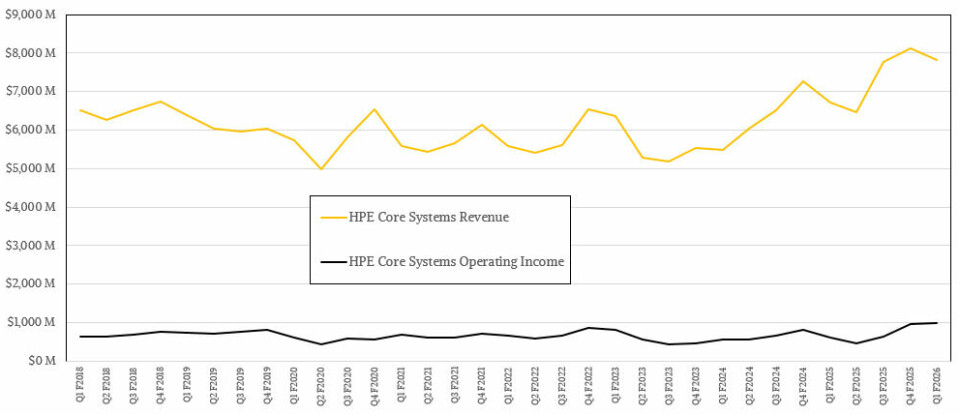

Our summary chart of the “core systems” business at Hewlett Packard Enterprise is usually the last thing we show you in our financial analysis of the company, but this time around we are going to start here because it frames the conversation. Take a look:

You can see how the GenAI boom and then the acquisition of Juniper Networks in the past two quarters have helped push up the revenue line for the servers, storage, switching and now routing, security, systems software, and financing that HPE sells into the datacenter. These numbers do not include branch, edge, and campus networking revenues from the newest HPE or other corporate investments.

This particular dataset has only been cast backwards to the time when Antonio Neri took the helm as the company’s chief executive officer, which was after the company bought HPC supplier Silicon Graphics but before it bought its bigger competitor Cray.

This has been a tough row to hoe for Neri & Co, hasn’t it? Kudos to Neri and his predecessors for staying in the game and trying to make some money while building complex systems for some of the most important organizations in the world.

NEXTPLATFORM AD

As you can see, the HPE datacenter systems business is now trending along at about $8 billion a quarter or so, and operating income is trending around $1 billion, which sure beats half of that and which explains why, in part, why HPE shelled out $14 billion in cash to buy Juniper. To be more specific, we think this core systems business drove $7.81 billion in Q1 F2026, up 16.2 percent, and that operating income for this datacenter stuff was $997 million, up 63.4 percent. The networking profits are helping, clearly.

Looking ahead, HPE wants to use Juniper to capture more networking revenue. Speaking generally, the AI systems market might grow to $1 trillion a year by 2030 or so, and $200 billion of that might be for networking. Even if you are a pessimist and say only a quarter or a third of that network spending will be done by traditional large enterprises, that is still a hell of a lot more total addressable market than either HPE or Juniper had been chasing with their respective networking businesses over the past decade. The trick will be to get GPU and maybe XPU allocations to build the systems that allow HPE to drive revenues with AI servers and drive profits with AI networking.

That is how Broadcom is doing it with its nascent custom AI systems business, and that is how Marvell is doing it, too.

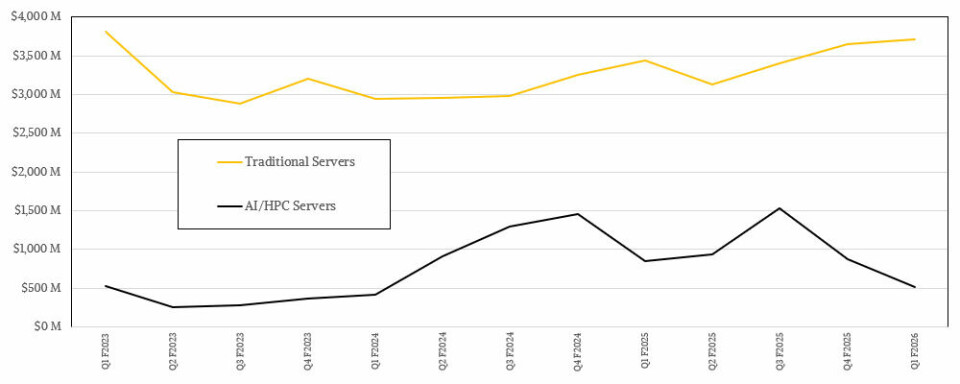

HPE did not provide revenue figures for AI servers and AI networking in its financial presentation for the first quarter of fiscal 2026, which ended on January 31, which would make life easier, but we can make some pretty good guesses about how traditional servers did and then subtract it out to get AI server revenues. With this methodology, what we can tell you is that AI server sales were not great, even though most of them were to enterprise customers (which is good if you want AI to mainstream) and not to service providers with bigger budgets.

NEXTPLATFORM AD

By the way, when HPE says AI servers, it means AI servers and HPC servers, which includes big clusters (and little ones) for simulation and modeling workloads. HPC’s share of the accelerated system pie changes radically from quarter to quarter, as it did for SGI and Cray.

If my model is right, and I obviously think it is pretty close, then AI/HPC server sales – what HPE used to call APU system sales – were down 39.2 percent to $517 million, and that was down from a pretty weak $850 million in AI/HPC server sales in the year ago period and down 40.4 percent sequentially from a pretty weak $867 million in Q4 F2025 ended in October last year. In the trailing twelve months, HPE’s AI/HPC sales are off 14.5 percent to $3.85 billion in fact.

But this may be on purpose as HPE is walking away from bad service provider deals and focusing on more profitable enterprise and sovereign deals. Neri did say on the call with Wall Street analysts that the $5 billion backlog it has for AI/HPC systems is primarily comprised of deals with enterprises and sovereigns.

Our best guess is that traditional ProLiant servers drove $3.72 billion in sales in Q1 F2026, up 8 percent year on year and up 1.9 percent sequentially from a pretty good $3.65 billion in Q4 F2025. Maybe it is a good thing that HPE didn’t do a lot of AI/HPC system sales in the quarter because it would have hurt profits, particularly with DRAM and flash memory prices skyrocketing.

NEXTPLATFORM AD

Here how Neri characterized the impact of memory and flash shortages and price spikes on HPE:

“The IT market is facing a sharp acceleration in supply tightness and increasing component costs, most notably in DRAM and NAND. We expect elevated prices to persist well into 2027. We are taking a series of distinct actions to address the current industry dynamics.”

“First, we are focused on securing supply. We have expanded our long-term multiyear agreements with our key silicon and memory partners to secure the capacity needed to meet customer demand. Second, we are protecting our margins. We have adopted an agile pricing posture with price adjustments across the entire portfolio with shorter quote commitment cycles. We have amended our quoting terms with a right to reprice existing orders for commodity cost increases between quoting and shipment. And third, we are proactively communicating with customers and channel partners, providing lead time and cost visibility along with alternative configuration recommendations to shape demand.”

“DRAM and NAND now make up over half of the bill of materials cost of a traditional server, and the share will continue to rise as component costs increases. As a result, we expect higher average unit prices in both our server and storage products. Networking is more insulated, with memory comprising a significantly smaller portion of the bill of materials. Given the supply dynamics, our fiscal 2026 strategy prioritizes higher margin product orders, which have an impact on our AI systems revenue growth rate for the year.”

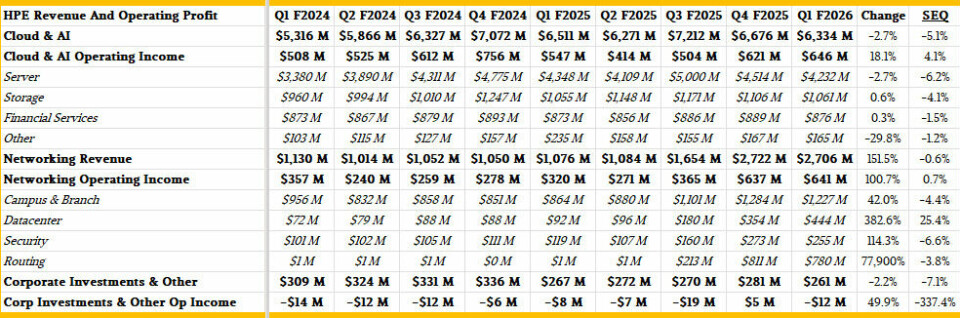

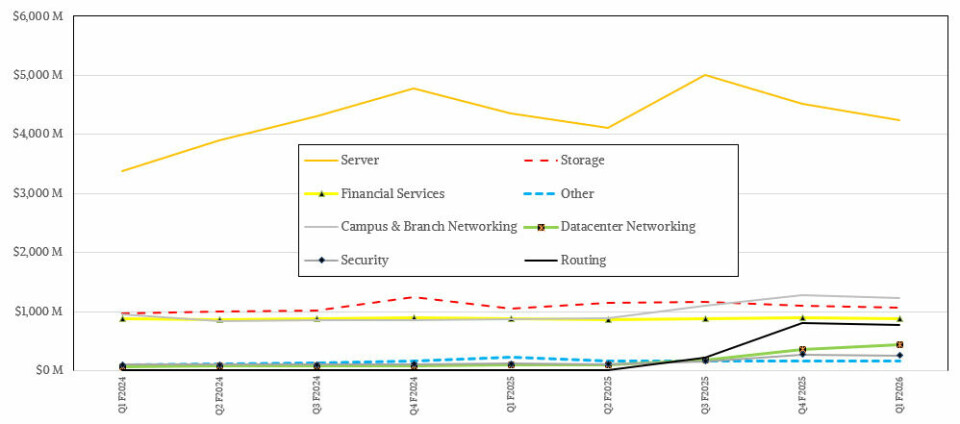

Here is a full breakdown of the revenues and profits of the new HPE groups and divisions, which were announced this week:

Let’s ponder this new Networking division. Neri said that networking, including HPE and Juniper products, now accounts for nearly 30 percent of the company’s revenue and more than half of the company’s profits. Obviously, over the next two quarters, as the Juniper numbers are added to the financials, it will grow by around 2.5X year on year, but it is not clear how much the combined businesses are actually growing. Basically, this buys HPE two more quarters of easy compares and then we will know how Networking is really performing. (I still don’t know what will happen to the “Rosetta” Slingshot Ethernet interconnect for HPC systems, now that I think on it. . . .)

HPE’s datacenter switching business was up 4.8X to $444 million. HPE had a teeny tiny routing business (probably based on Broadcom chips) that only drove $1 million a year ago, but after the acquisition, it is up 77,900 percent to $780 million in Q1 F2026.

Servers are still the revenue driver, as you can see, and brought in $4.23 billion in the period, but it was down 2.7 percent because of (purposely) sluggish AI/HPC system sales. Storage in the aggregate doesn’t change much at HPE quarter to quarter and year to year, and was up six-tenths of a point to $1.06 billion this time around. Financial services, which also trundles along, was up three-tenths of a point to $876 million in the quarter.

Add it all up, and HPE had 9.3 billion in sales, up 18.4 percent, with operating income of $470 million, up 8.5 percent, and net income of $452 million, off 27.9 percent and bolstered by some tax accounting stuff. The company exited Q1 F2026 with $4.84 billion in cash and $17.71 billion in long term debt, most of which came through the Juniper acquisition.