When we try to predict the weather, we use ensembles of the initial conditions on the ground, in the oceans, and throughout the air to create a kind of probabilistic average forecast and then we take ensembles of models, which often have very different answers for extreme weather conditions like hurricanes and typhoons, to get a better sense of what might happen wherever and whenever we are concerned.

Trying to figure out markets is no different. More data is better, and you have to look at ensembles of data and their underlying assumptions to try to reckon what might happen. There is a certain amount of gut instinct about human behavior and economic vectors as well, which is not precisely scientific but that’s people for you. And so we try to look at as much data as we can in sussing out a market, fill in gaps where we see them, inform this with what we know about underlying component and system suppliers, and give you a likely scenario so you can plan your IT spending, your own compensation, and therefore your own life. (That’s also why we keep track of things, to be honest.)

With that, we turn our attention to the latest AI spending forecast from the market researchers at Gartner, which you can see a bit of in the public statement it made about a much deeper report it has done. The upshot is that Gartner has updated its forecast for a more ebullient AI spending environment. A day doesn’t seem to go by when someone isn’t throwing a few billion, or tens of billions, or even hundreds of billions of dollars around over the next four or five years.

Where all of this money is supposed to be coming from is still not clear, and that is either hope or deliberate obfuscation. It is hard to say because companies like OpenAI and Anthropic and xAI, which are driving a lot of spending on AI hardware and software, are privately held and have no obligation to talk about where they anticipate their funds for massive AI installations – often in multi-gigawatt capacity chunks – will come from. Thus far, none of their services generates anything close to the revenue streams necessary to support the kinds of investments we are chronicling here at The Next Platform. For their part, Nvidia, Oracle, and the neoclouds that are involved are talking about their investments and their orders, which for OpenAI in particular are stunning in their magnitude.

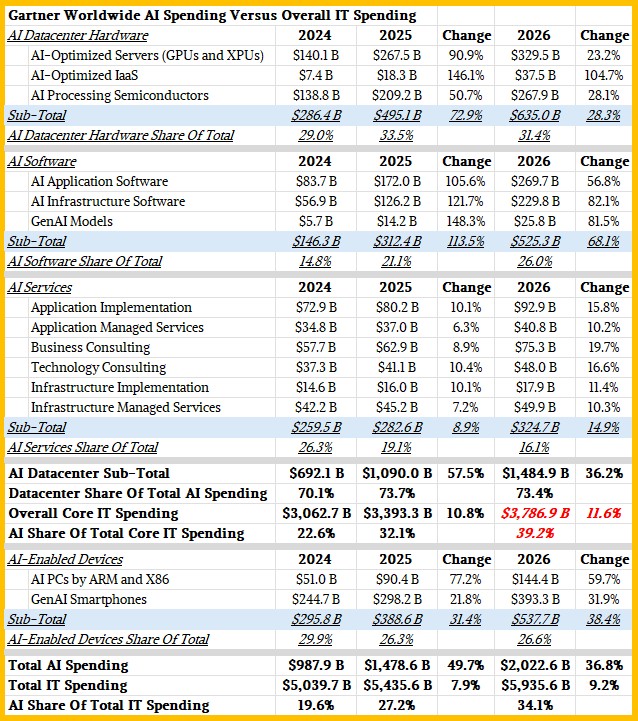

Like us, and like you, companies like Gartner have to look at all that is being announced and try make sense of it – in Gartner’s case by jamming it into a global IT spending model. Here is the AI spending Gartner thinks happened in 2024 and will happen in 2025 (which is nearly three-fourths over) and in 2026 (which everyone is absolutely salivating over):

The spending data from both IDC and Gartner always includes datacenter gear – the five Ss of servers, switching, storage, software, and services – and end user device gear – meaning desktop PCs, laptop PCs, tablets, and smartphones. They don’t agree on whether or not to count telecom services in the IT spending pie – IDC does, Gartner doesn’t – and that skews the numbers between the two quite a bit.

As you can see from the table above, we are talking about a lot of AI spending in 2024 and being forecast for 2025 and 2026. Gartner reckons that AI spending across all categories amounted to an absolutely huge $987.9 billion last year, and believes that based on current trends and the eight months under our belts here in 2025 will grow by 49.7 percent to a stunning $1.48 trillion in 2025. But the bucks do not stop there. Gartner is forecasting that AI spending will keep motoring with 36.8 percent growth in 2026 to crest above $2 trillion.

It sure does look like a bunch of people are going to get rich.

We want to point out a few things – questions, really, which we asked of John-David Lovelock, distinguished vice president analyst at Gartner who puts together the company’s forecasts.

First, we did not know what “AI Processing Semiconductors” literally means, and with the large numbers associated with this category, we want to know. We thought that this might be the aggregate value of all embedded AI-capable devices sold, including GPUs and XPUs that companies such as hyperscalers, cloud builders, and AI model builders, contract directly with their designers for use in their own devices and systems. “This is a spending forecast, not a value-add projection,” Lovelock explained to The Next Platform. “The forecast represents the money that semiconductor companies will make in a given year and the amount of money that companies selling servers will make in a year.”

We interpret this – and the fact that all of these numbers are added up to get an overall AI spending figure – to mean there is no overlap with this AI chip figure and the AI-Optimized Server numbers. You can’t count the GPU and XPU devices twice if this is end user sales or factory revenues (which are not the same thing because there is often a channel partner in the middle that adds their margin).

We thought that the AI-Optimized IaaS figure – meaning AI infrastructure sold under a cloud pricing model – for 2024 was quite a bit lower than we expected, particularly considering that the big model builders like OpenAI and Anthropic are largely buying capacity from Amazon Web Services, Microsoft Azure, and Google Cloud to do their training and run their inference for their API access, which in turn drives model sales and API token processing sales for them.

Lovelock explains:

“The IaaS number represents the revenue booked by hyperscalers for selling AI-Optimized IaaS. If the server capacity is used for internal purposes, that use does not generate revenue and is therefore outside of the IT spending forecast. For example, the server farms at Microsoft are being used to run Copilot – the revenue shows up in the email and authoring forecast, not in the IaaS forecast. Google is running Gemini as an enterprise and consumer product on their server farms. The forecast does not make any attempt to track internal use or interdepartmental transfers.”

“The hyperscalers are building massive datacenters not to rent out the capacity and earn IaaS revenue – that would be following the traditional server business model. Instead, they are bringing GenAI products, tools, and services to market and making money on those services.”

So, it looks like that first wave of AI investments in 2023 and 2024 was really about pushing AI into customer-facing applications at the hyperscalers and cloud builders.

Lift And Shift And Expand

We want to organize this IDC data a bit and expand it with some data Lovelock graciously supplied, and then compare it to overall IT spending data from Gartner, which released its most recent forecast back in July. (See How To Cash In On Massive Datacenter Spending.) So here is a table that brings this all together and organizes it in a way that we think makes more sense for analysis:

We assume that the bulk of the AI Processing Semiconductor revenues belongs in the AI Datacenter Hardware category that we created, and that assumption may not turn out to be correct. But for the moment, assume that it is. Then datacenter hardware supporting AI workloads was $286.4 billion in 2024 and represented 29 percent of overall AI spending and will grow by 72.9 percent to $495.1 billion this year. Next year, datacenter hardware for AI will grow by only 28.3 percent, but will reach a staggering $635 billion. The cloudy IaaS part of this sub-market is growing the fastest, by 2.5X in 2025 and more than 2X in 2026, but is still dwarfed by AI server and AI chip revenues.

You will note that the AI hardware part of the overall AI spending pie is growing, but will shrink a bit as AI-enabled software becomes more important in the future.

If you look at AI software, what this shows is two things. First, infrastructure and application software will be infused with AI functions, and as that happens, more revenue for this enterprise software will end up in the AI category and not be relegated to the non-AI part of the market. (Much as more than half of the server capacity sold in the world today uses a cloud or cloud-like utility pricing model.)

You will note that revenues coming directly from the sale of GenAI models is relatively small, will have a burst next year, and start cooling almost immediately.

We think that GenAI API revenues are included in the AI Services sub-market along with various consulting, implementation, tech support, and model hosting services that companies are peddling (including the big cloud builders and even hyperscalers like Meta Platforms, which doesn’t have a cloud utility that you can buy from but which does offer a Llama model API service to chew on and generate tokens.)

As you can see from the table that we made, the AI Services sub-market will grow, but only modestly and its share of the AI spending pie will actually shrink because of that. That is very unlike the Dot Com boom, which had a lot of services companies helping do the heavy lifting as the new technology was absorbed.

If you add up datacenter hardware, software, and services from this IDC data, then you get an aggregate spending of $692.1 billion in 2024, growing by 57.5 percent to $1.09 trillion this year and then growing by 36.2 percent in 2026 to $1.49 trillion. The datacenter share of overall AI spending is growing, but will stabilize at just shy of three-quarters of the AI spending pie, according to IDC’s numbers.

Just for fun, we added in the Core IT datacenter spending figures we extract from Gartner’s IT spending forecasts to our table so you can have a “compared to what?” that is so vital for context in these numbers. IT spending is being buoyed by AI spending, no question about it. But it will be a while before it dominates all of IT spending the way Gartner calculates it. By our math and IDC own data, AI drove 22.6 percent of datacenter spending in 2024, and this will grow to 32.1 percent in 2025 if the forecasts turn out to be right. IDC did not provide a breakdown for IT spending in 2026 that would let us calculate datacenter spending within that, so we have done our best to estimate that for 2026, as shown in bold red italics. We think AI will drive nearly 40 percent of datacenter spending across systems, software, and services in 2026, and it will probably come close to half of datacenter spending in late 2027 or early 2028.

We find the AI-Enabled Devices category, as we are calling it in our table, amusing. Eventually, all personal devices will have vector or matrix math engines allowing for AI processing locally on those devices to some degree, so tracking this is a short-term phenomenon. (Just like eventually all systems will have some form of virtualization and some form of utility pricing that lets them be called “cloud” instead of “non-cloud.”) We separate the personal device stuff out for a reason when we do our analysis, and this is why. Also, we care about the datacenter here, not the stuff that links to it.

Anyway, if you add devices to datacenter stuff, then AI drove 19.6 percent of IT revenues in 2024 and will drive 27.2 percent of IT revenues in 2025 and 34.1 percent in 2026.