Broadcom turned in its financial results for its third quarter last night, and all of the tongues in the IT sector are wagging about how the chip maker and enterprise software giant has landed a fourth customer for its burgeoning custom XPU design and shepherding business. The word on the street is that this fourth deal is for OpenAI’s forthcoming homegrown “Titan” AI inference chip, which is expected to be launched in the second half of next year.

While Nvidia has gone to great lengths with the “Blackwell” GB300 NVL72 rackscale system to drive up FP4 performance and therefore drive down inference costs, the hyperscalers and cloud builders – and now the world’s largest independent AI model builder – wants to break its dependence on Nvidia GPUs.

OpenAI did a $40 billion Series F funding round in March, driving its pre-public valuation to around $300 billion, and in September it allowed current and past OpenAI employees to sell up to $10.3 billion in their shares, placing it at a $500 billion valuation; this secondary offering lets OpenAI employees cash in some of their stock riches ahead of an initial public offering that could happen, well, whenever.

Here’s the thing: that secondary offering does not help OpenAI raise money for infrastructure, and we would argue makes it harder to do a Series G round because OpenAI would have to push its valuation up towards $1 trillion to raise maybe another $100 billion. At this point in the GenAI game, that is only a piece of the four year, $500 billion Stargate effort announced back in January by OpenAI & Friends.

The point is, OpenAI has the money to design its own AI training and inference chips, and it cannot afford to wait. The company lost $5 billion against $4 billion in sales in 2024, according to reports in The Information. Even with the expected $11.6 billion in sales in 2025 reported by the New York Times, OpenAI’s losses are probably going to be huge. Given the high cost of renting capacity on the public clouds or even the neoclouds, the company is at a scale that almost requires it to co-design its own hardware to better match its own software and also reduce its costs. It was one thing when Microsoft pumped $13 billion into OpenAI for a stake, which was mostly turned around to buy capacity on the Azure cloud to train models. But now OpenAI has to spend its own money on infrastructure and it needs to be more frugal and at a much larger scale to meet its Project Stargate goals as it races towards artificial general intelligence or superintelligence or whatever the hell people are calling it today.

The point of this story is that it looks like Broadcom is going to be a big beneficiary of all that OpenAI needs to do to get control of its infrastructure costs. But perhaps by not as much as the headlines were suggesting today.

Let’s walk through the numbers for Broadcom’s Q3 and see what Hock Tan, Broadcom’s founder and chief executive officer, actually said about the deal that is probably for OpenAI’s custom XPU.

In the third quarter ended on August 3, Broadcom had $15.95 billion in sales, up 22 percent year on year. Operating income was nearly doubled to $5.89 billion, and net income at $4.14 billion compared to a $1.88 billion loss due to the writedown of assets and restructuring costs from the VMware acquisition. Net income share of revenue was 26 percent, which is a little light compared to recent quarters and showing how maybe this hyperscaler and cloud builder – and now model builder – custom XPU and networking business is not as profitable as it might be.

Broadcom ended the quarter with $10.72 billion in cash and equivalents in the bank, and it paid down a little more than $3 billion of its debt, which is still piled up to $64.22 billion after that.

Broadcom is still reporting numbers for its two groups – Semiconductor Solutions and Infrastructure Software – but is no longer breaking out its divisions – Networking, Server Storage Connectivity, Wireless, Broadband, and Industrial – specifically by numbers in its presentations. It made some vague statements of sequential growth and decline, which we have took a stab at quantifying in our model. (More on that below.)

Semiconductor Solutions posted sales of $9.17 billion, up 26 percent, with operating income of $5.23 billion, up 29.3 percent. Infrastructure Software, which includes a bunch of mainframe stuff, Unix stuff, and VMware server virtualization, added up to $6.79 billion in the quarter, up 17 percent, with operating income of $5.23 billion, up 33.8 percent.

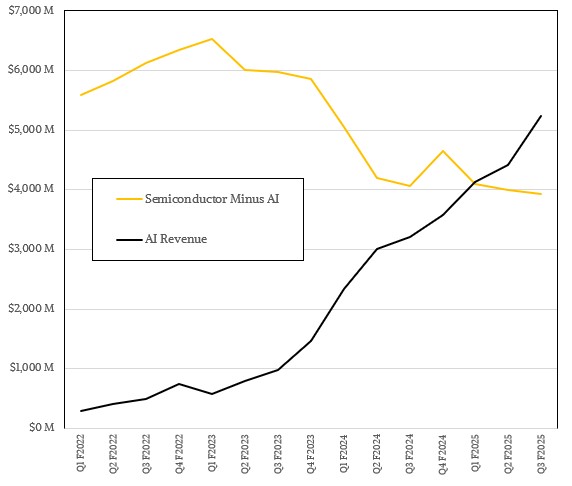

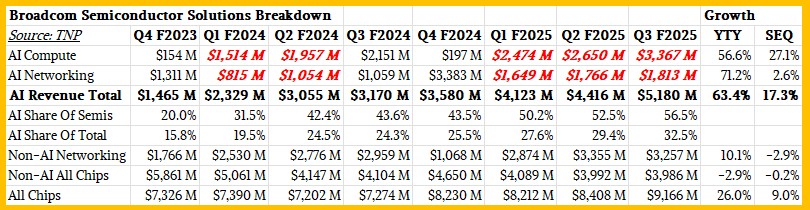

Broadcom said that sales of AI-related chips – custom XPUs, switch ASICs for AI clusters, other stuff – rose by 63.4 percent, which we peg at $5.18 billion. This obviously drove a lot of the growth in Broadcom’s chip business. This chart makes that obvious:

That AI revenue curve is not as smooth as it looks. Within that black line, there is an ebb and flow to AI compute and AI networking, which are operating at different cycles. You can see it in the chart below, which attempts to break out AI networking distinct from AI compute at Broadcom:

If we estimate the revenues for the five Broadcom groups, as we have done, and you do the math, then revenues for non-AI networking were up 10.1 percent to $3.26 billion. This is not too shabby and is still considerably larger than the $1.81 billion (up 71.2 percent) that Broadcom booked in AI networking chippery sales. We think it will not be long, with the Tomahawk Ultra and Tomahawk 6 and Jericho 4 switch ASICs coming next year, that the AI portion of the networking pie is draws even with the non-AI part. And we would not be surprised to see AI networking be larger than non-AI networking in the long run, either, given the high-end nature of Broadcom’s datacenter networking ASICs.

AI compute comprised $3.37 billion in sales, up 56.6 percent, and AI networking made up the remaining portion outlined above.

AI is being very good for Broadcom, obviously, with three hyperscalers and cloud builders (Google, Meta Platforms, and ByteDance) doing custom XPUs in conjunction with Broadcom and paying it we presume pretty well to help in the designs and shepherd them through the Taiwan Semiconductor Manufacturing Co foundries and their packaging affiliates.

Looking ahead, Tan is forecasting that AI chip revenues will be $6.2 billion in Q4 F2025, up 66 percent and that non-AI chip revenues will “grow low double digits” sequentially to hit around $4.6 billion. That’s $10.8 billion for chips in Q4.

Looking further out, Tan said this on the call with Wall Street analysts: “Now further to these three customers, as we had previously mentioned, we have been working with other prospects on their own AI accelerators. Last quarter, one of these prospects released production orders to Broadcom, and we have accordingly characterized them as a qualified customer for XPUs and, in fact, have secured over $10 billion of orders of AI racks based on our XPUs. And reflecting this, we now expect the outlook for our fiscal 2026 AI revenue to improve significantly from what we had indicated last quarter.”

OK, so unlike the impression that was given in many titles in the IT trade and economics press, the $10 billion order that everyone presumes is OpenAI is for complete systems, not what Broadcom gets for the custom XPU, presumably the Titan inference chip as we said. Tan said the revenue for this deal would start coming in during the third quarter of fiscal 2026, to be precise.

We will start digging around for more information on the Titan XPU from OpenAI. We don’t expect for it to be open sourced, just like OpenAI’s GPT large language models are not.

One last thought, and it is an interesting and possibly exciting one if you are enthusiastic about optical interconnects for XPUs and their memories to open up AI server architecture.

Way back in 1990, when the Internet was yet to be commercialized, data was not yet big, and parallel processing was limited to a handful of compute engines, Richard Ho got his master’s degree in microelectronics systems engineering from the University of Manchester, and in 1996 he got his PhD in computer science from Stanford University. Ho was co-founder and chief architect for a company called 0-In Design Automation, developing the technique of assertion-based verification for RTL designs for chips. Mentor Graphics acquired the company in September 2004 and hung around for a year before joining DE Shaw Research as a research engineer for the Anton 1 and Anton 2 bespoke supercomputers for doing molecular dynamics. Specifically, Ho worked on the verification of the components in the Anton designs, with a specialty in tricky bits that are hard to simulate. In 2013, Ho was tapped by Arm server CPU upstart Calxeda to verify the system fabric used with the Calxeda EnergyCore processors.

Calxeda ran out of money and customers a year later, so Ho got a gig as a senior staff engineer at Google, and jumped in as one of the dozens of researchers working on the Tensor Processing Unit, which first went into production at the search engine giant in 2015. Ho rose through the ranks at Google, becoming senior director of engineering, streering the development and delivering of many generations of TPUs as well as the Video Coding Unit for YouTube, the EdgeTPU for Pixel phones, and the IPU with partner Intel. After nine years at Google, Ho jumped to silicon photonics startup Lightmatter to be vice president of hardware engineering and then senior vice president of silicon and software engineering.

After a little more than a year, in November 2023, Ho was approached by OpenAI to be head of hardware, in charge of developing its silicon roadmap.

It would be hard to find someone more suited to the task. And, we think, it is possible that OpenAI will beat Nvidia to the table innovating with silicon photonics in AI systems — perhaps even licensing the Passage interposer and optical interconnects from Lightmatter to get a leg up.