Jayshree Ullal, the chief executive officer of Arista Networks, has been pointing at the $10 billion revenue upper decks since the beginning of the AI boom, but is understandably hesitant about saying when the company would cross that threshold.

Back in February, we did the math and said that Arista could reach that level in 2026 with very little effort given the AI cluster buildouts we know about, the desire to upgrade networks that link other systems together and that also feed into AI systems (both on premises and in the clouds), and the expansion into campus networking where Cisco Systems still rules. As it turns out, Ullal admitted in a call with Wall Street analysts going over the company’s second quarter financial results that the original goal was to break $10 billion in 2028 or so. But the desire to replace InfiniBand with Ethernet for back end AI networks is so strong that Ullal went public and said, as we did, that Arista could in fact do it in 2026.

Concurrent with that steepening of the revenue curve, Ullal revised guidance upwards for the third quarter ending in September to $2.25 billion, and we think that might be a tiny bit conservative considering it is only a smidgen larger than the $2.21 billion it booked in Q2 2025. She also added that even with the loss of one of the five big AI customers that are in various stages of testing and deployment, Arista will hit or exceed its $750 million target for back end AI network gear sales in 2025 and a combined $1.5 billion for back end and front end network sales that are tied to AI workloads.

Small wonder, then, that Arista added $26.3 billion to its market capitalization in the week since it reported its results for Q2, ending today at $177.5 billion. (That’s a lot of unicorns – 177.5, to be precise.)

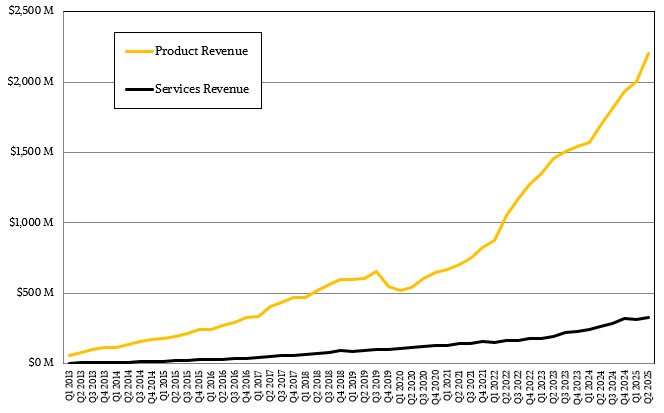

In the June quarter, Arista had $1.88 billion in product revenues, up 31.9 percent year on year and up 10.9 percent sequentially from Q1.

Within that, $31.6 million of revenue came from software subscriptions, up 4 percent from the year ago period. Services revenues, which is predominantly tech support for switches and network operating systems, rose by 22.7 percent to $327.8 million. Software and services together rose by 20.8 percent to $359.4 million and represented 16.3 percent of revenues for the quarter.

When Arista first started talking publicly about this software and services category back in the first quarter of 2021, it represented more than a fifth of revenues. The hardware business is growing faster than the software and services content of deals, which is why the share of overall revenues is shrinking. That’s because Arista’s customers are all speed demons. The software and services money will follow.

All told, Arista booked a tad more than $2.2 billion in revenues in Q2, up 30.4 percent year on year. Operating income was $986 million, up 41 percent, and net income rose by 33.6 percent to $889 million and comprised 40.3 percent of revenues. This is about the same income level the company has had for the prior four quarters and is pretty high for a system maker – particularly one with hyperscalers and cloud builders – what Arista calls the cloud titans – as key volume customers. Back when we first started tracking Arista back in 2013 after it went public, it’s profitability averaged just under 12 percent of revenue.

It is reasonable to wonder how Arista will be able to maintain such a high profitability when there are so many whitebox hardware vendors out there as well as more than a few tech titans making their own switch gear. Arista’s answer to this is to be the preferred hardware platform for key workloads and then allow customers to install their own NOS software on their machines (Microsoft has SONiC and Meta Platforms has FBOSS), creating what it calls a “bluebox” alternative to whitebox machines from Edgecore Networks, Quanta, Delta Networks, Celestica, Inventec, Wistron, and a few up and coming players.

Ullal had this to say on the call when asked about the competitive landscape.

“We have always lived in a very competitive industry whether it was – I shouldn’t say it was Cisco or specific networking vendors. And we acknowledge Nvidia’s participation both with InfiniBand and with bundling with the GPUs. We have always acknowledged the co-existence with whitebox. So from our perspective, the competitive landscape has not changed, it’s more of the same. But I recognize that the chatter was louder, and we understand that given the volatility of some of our customers, some years and some quarters are better.”

“So I think some of the chatter was louder because our Meta share wasn’t growing the same way as it did year-over-year in the prior years. But from our perspective, our innovation and differentiation has never been stronger at a platform performance level, at a feature level. And I want to add a third one, which is at a customer intimacy level. They are so appreciative of the support, the quality, and the way we approach how to solve their problems. So no change in our environment on innovation. There’s plenty of chatter outside. I appreciate that. I understand that. And I hope we have proved the naysayers wrong.”

With one more quarter down and a forecast for the third, we are also tweaking our model upwards a bit for Arista. We conjecture that it will bring in at least $8.5 billion in revenues in 2025. There is no reason to believe that services revenues cannot continue to grow at 35 percent or so, which puts them at $1.5 billion this year, with $7 billion left over for products. What this means is that if services continue to grow at the same pace, then they will rise above $2 billion in 2026, leaving $8 billion in hardware. That only requires 15 percent growth in products in 2026, which we think is absolutely doable given the next wave of heavy AI spending slated for 2026, when a slew of new products from Nvidia, AMD, Broadcom, and others are due. And that will give Arista a little less than a fifth of the $54 billion total addressable market it has set as a target, which includes datacenter and cloud networks, campus networking and routing, and software and services for the whole shebang.

We are not convinced that the network market watchers have this next AI bubble in 2026 baked into their numbers them as yet. It doesn’t look like it from the data from 650 Group that Arista cited in the financial report accompanying its Q2 2025 results:

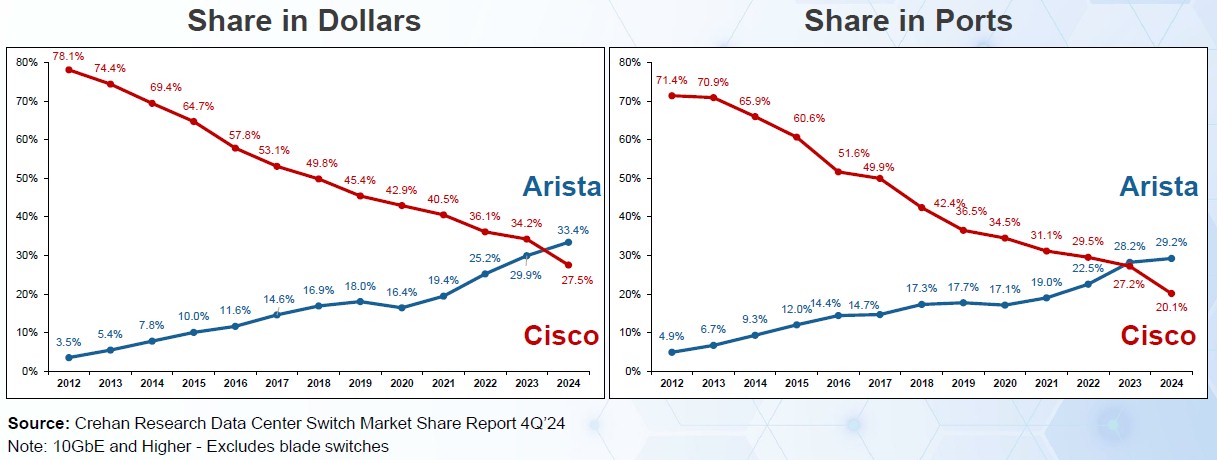

That presentation shows in the following chart just how much grief Arista has given archrival Cisco Systems in high-speed Ethernet ports in the datacenter over the past four years. This is based on data from Crehan Research:

That data above is for 100 Gb/sec, 200 Gb/sec, and 400 Gb/sec datacenter Ethernet switches, not for the market at large where there are a slew of vendors and Cisco has a much higher share.

This chart below, also based on data from Crehan Research, must keep Cisco executive up late at night and help the executives at Arista sleep pretty well:

This is for switches with 10 Gb/sec or faster ports, and it shows Arista made more money on such machines than Cisco starting in the middle of 2023 and shipped more ports at the beginning of 2023. This data excludes blade server switching, which means it does not include switches sold for Cisco’s UCS blade server platforms. Argue amongst yourself how fair this may or may not be.

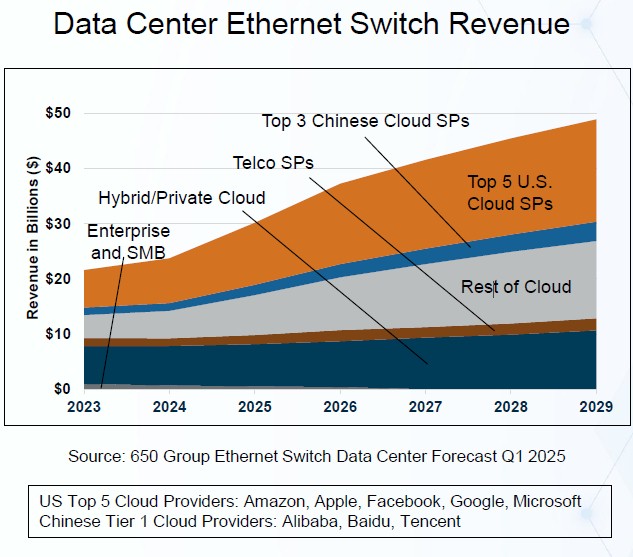

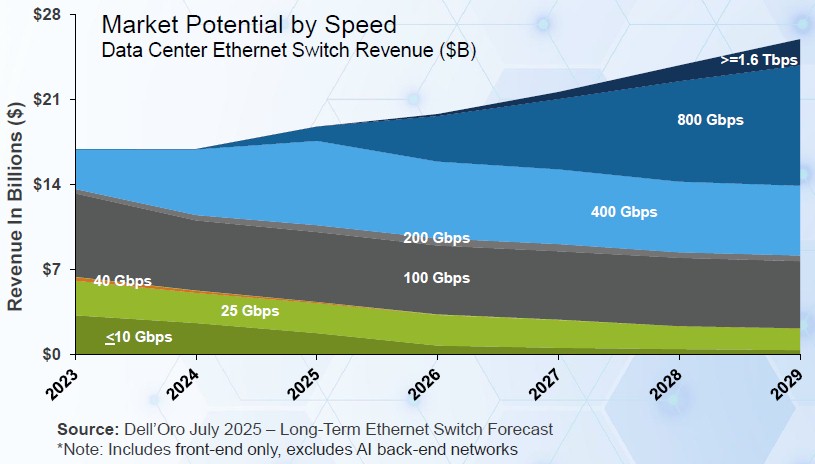

And finally, here is a pretty revenue bandwidth parfait over time for Ethernet switching in the datacenter, which puts some bones on the TAMs that Arista and others talk about:

This data is from Dell’Oro Group, just completed in July, and only considers revenues for front end networks and does not include back end networks for AI clusters. We would love to see that data separately and see it superimposed on the front end network data.

We also look forward to announcements from Arista for scale-up networks for rackscale AI systems based on UALink switching and Ethernet supporting Broadcom’s Scale Up Ethernet (SUE) approach. Arista has made no formal commitments to either, but SUE is almost certainly going to be something Arista wants to commercialize, given its Ethernet base. We will reach out to Arista to get its thoughts on UALink and SUE, which could represent another product line that could bring hundreds of millions to billions of dollars a year to the company.