Sometimes, competing for business means coming up with better products than your rivals. And other times, competing means just not screwing up while your competitor stumbles. For the heated battle between AMD and its archrival, Intel, when it comes to compute engines in the datacenter, AMD is in the fortunate position of being able to leverage both tactics at the same time.

And we say fortunate, we mean that AMD is raking in money and rapidly re-investing it into the further expansion of its business as well as buying up the stock that will allow it to reward employees who have worked hard for this day to come.

Seven years ago, when the Epyc comeback plan was formulated, AMD could not have dreamed in a million years that Intel’s vaunted foundries would run into so many troubles with 10 nanometer and then 7 nanometer processes. The current situation has created as big of a gap for AMD to exploit as Intel’s stubborn decision to put forth the Itanium architecture as the future of datacenter compute back in the late 1990s and early 2000s, which gave AMD the immense opportunity to peddle 64-bit Xeon-compatible Opteron processors against 32-bit Xeons (which Intel initially refused to bit-wise embiggen) and 64-bit – and mostly non-compatible – Itaniums.

We would say that such opportunities come along only once in a lifetime, but they don’t. Intel kicked AMD out of the datacenter in 2009 because it had its foundry humming and a completely redesigned 64-bit Xeon line (which borrowed plenty of ideas from the Opteron, of course) at the same exact time that AMD started having issues with the Opteron architecture and everyone was really risk averse in the datacenter. And so, as the Great Recession was in full swing, Intel spanked AMD and sent it to bed outside of the datacenter with no dinner or desert.

There is a chance – one might even say a high probability – that Intel will get focused with both its chip designs and its foundry processes and come back at AMD fiercely as it has in the past. But that chance is not today with CPUs, GPUs, or FPGAs, and it is probably not going to happen any time soon. We might see an Intel revival gaining traction in 2024 or 2025 at this point, it looks like. And there is always a chance that something terrible will happen with AMD designs or the foundries of Taiwan Semiconductor Manufacturing Co and Globalfoundries, where AMD sources the chippery that goes into its Epyc CPUs, Instinct GPUs, and Versal FPGAs. But we highly doubt it.

And so, AMD chair and chief executive officer Lisa Su can now relax a little bit, put on a green visor, and count the money. (For one day, anyway. Then it is back to the grind. . . . )

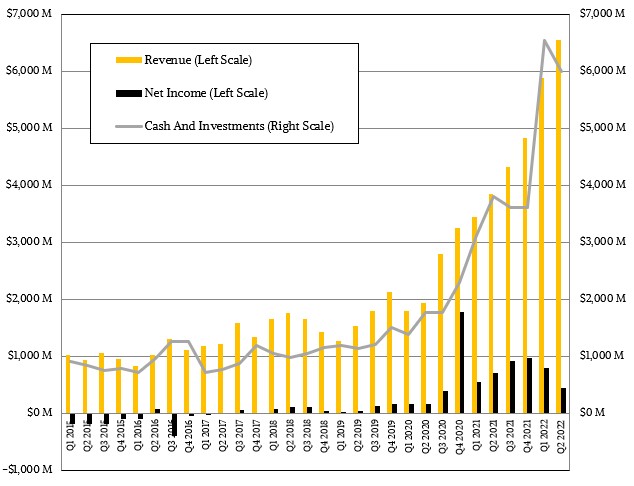

In the quarter ended in June, revenues for AMD were up 70.1 percent to $6.55 billion. Due to higher costs for development of products like the “Genoa” and “Bergamo” Epyc 7004, the “Genoa-X” and Turin tweaks to the Epyc 7004 designs with Zen 4 cores, the “Turin” and “Siena” CPUs with Zen 5 cores coming further down the road in 2024, as well as the still-un-codenamed Instinct MI300A hybrid CPU-GPU compute engine coming next year, net income took a pretty big hit. Research and development cost nearly doubled to $1.3 billion, and marketing and general costs rose by 73.6 percent; there was another $616 million charge to amortize stuff in the acquisitions of Xilinx and Pensando. All of this combined to push down net income by 37 percent to $497 million. AMD took some similar hits to the bottom line in the first quarter, but this was against an easier compare. Hopefully, that is the last of it, and going forward Wall Street can relax as more of the money falls to the bottom line in Q3 and Q4.

AMD will be pre-paying for foundry capacity to ensure its places in line at TSMC and GloFo, so that will something of a drag on current profits, too. But the benefit is that AMD, like other key chip makers, have much better visibility into chip buying plans of hyperscalers, cloud builders, OEMs, and large enterprises, which helps it better manage its supply chain.

AMD ended the quarter with $5.99 billion in cash and investments, and it can easily pay for more foundry capacity should the opportunity present itself.

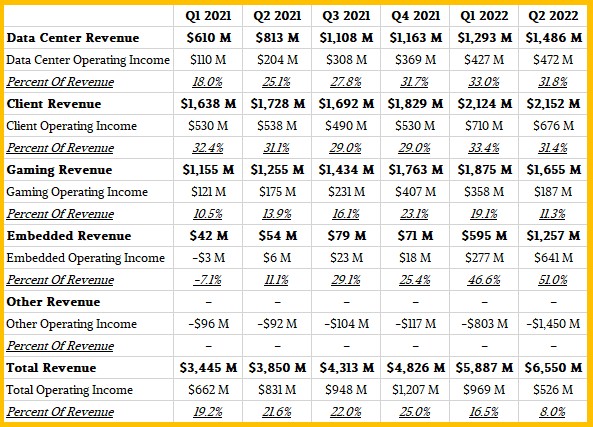

We don’t have to guess any more how AMD’s datacenter CPU and GPU business is doing each quarter. In the wake of the Xilinx and Pensando acquisitions, AMD reorganized its groups and has put CPU, GPU, FPGA, and DPU units sold into the datacenters of the world into a new Data Center group. Revenues and operating income for these groups – Data Center, Embedded, Client, Gaming, and Other – are now provided and have been backcast to Q1 2021 for the sake of comparison. Here is a table that summarizes the financials for these new groups:

And here is a chart that plots out this data so you can absorb it quickly:

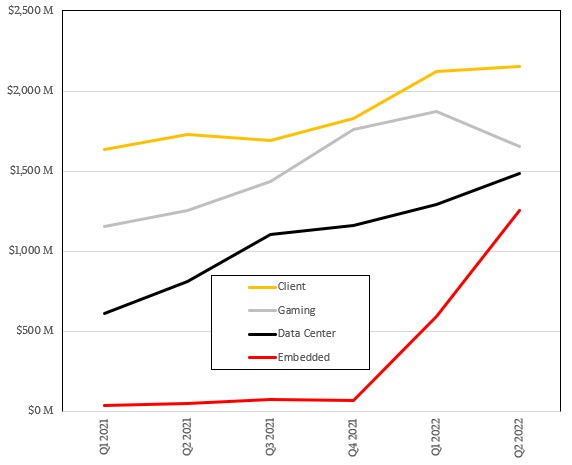

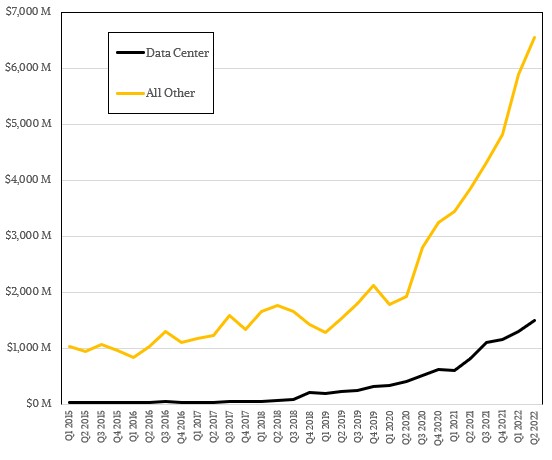

We have data going back to 2015 for AMD’s overall revenues and its sales from datacenter products, and this chart illustrates that very long haul:

One important caveat is that there are embedded CPUs and FPGAs that are sold into network and storage gear that eventually ends up in the datacenter, which means that strictly speaking, AMD sells more chips into the datacenter than even its own financials show. How much, we are not sure. But it is probably not as material as the growth AMD expects to see in core Epyc CPU and Instinct GPU sales in the coming years.

Which brings us to how AMD is driving on its Epyc roadmap. There is “strong customer pull” for the Epyc 7004, Su said on the call going over the numbers with Wall Street analysts, and she added that the Genoa ramp will start its fast uphill climb in the fourth quarter and then keep climbing into the first half of next year.

There is a very good chance that the hyperscalers and cloud builders are going to be able to buy a lot of Milan and Genoa capacity this year and add some Bergamo capacity next year and still have much better bang for the buck per server than in 2020 and 2021, allowing them to do a lot more compute with a little more budget and therefore not spend as much as they might otherwise if AMD had not been in the market the way it is now. This only hurts Intel, particularly if the “Sapphire Rapids” Xeon SPs are delayed into next year for volume production and Intel has to cut price because Sapphire Rapids is not competing against last year’s Milan, but next year’s Bergamo among hyperscaler and cloud builder customers where AMD’s share could be as high as 35 percent right now. The best guesses across the Wall Street people that we talk to (who have access to Gartner, IDC, and Mercury Research server data) are that AMD has about north of a 25 percent share of server sales right now across all server sizes and types, which means Epyc has finally outdone Opteron.

It looks like the Epyc line will have a much longer life, given the seriousness and consistency with which AMD is executing on its roadmaps.

One big change between then, in the early to late 2000s when several very good generations of Opterons came out, and now, from the 2017 launch of “Naples” to the launch of “Genoa” here in 2022 is that the supply chains of the world are screwed up, and particularly for silicon wafers, the substrates that etch and clean them as chips are being made, and the capacity of the fabs themselves. Given this, Su said that AMD now has visibility across its largest customers as far as six and eight quarters out into the future. This is truly amazing, and stands in stark contrast to the situation before the coronavirus outbreak broke the supply chains, tangling up the threads that have stitched together a virtual Pangea over the past several decades. At best, companies like AMD got a warning one or maybe two quarters in advance that they needed to make a certain volume of chips.

“The planning that we are doing jointly with our customers has been very helpful,” Su said in what can only be thought of as an extraordinary understatement. “Much of our conversation right now, frankly, is about 2023 and ensuring that we have enough capacity for some of the build-outs that are out there.” And we are only halfway through 2022, which means that AMD is pretty confident that it will have enough capacity to meet the needs of most of its customers here in 2022, even if it is still a bit supply constrained on CPUs and FPGAs.

Our guess is that AMD will still be supply constrained well into 2023, and that is as much due to Intel’s Xeon SP delays as it is to the timing of the AMD roadmaps. Intel keeps missing its target, which isn’t just a date on a calendar, but a particular CPU with specific features and capacity that is positioned against all other CPUs with their features and capacity. The more Intel keeps doing this and falling behind, the more pressure that will fall on AMD.

Without getting into specifics, AMD said that the Xilinx business grew 20 percent sequentially, and that is spread across the Data Center and Embedded groups.

“We are still a bit constrained in certain parts of the Xilinx portfolio, although we continue to make good progress,” Su elaborated. “And I expect additional supply to come on, especially towards the latter part of the year and into 2023. Our view of the business, again, is I think the quality of the design wins, the quality of the overall diverse market is very strong, and so I think that as we are able to continue to relieve some of those supply constraints into the second half of the year, I think we will see a good growth trajectory for the business.”

We are intrigued about how the datacenter GPU business is doing, and AMD is not going to say much about this still nascent business, aside from constantly reminding us that its “Aldebaran” Instinct MI250X GPUs are in some of the fastest supercomputers in the world right now, with more on the way.

“We continue to make good progress with datacenter GPUs,” Su explained. “The key there for us is to work with some of the large hyperscalers who have been very closely partnering with us on our MI200 product. I think from an overall revenue standpoint, it’s not a big contributor this year. But certainly, we would expect it to be a larger contributor in 2023 as some of those initial engagements turn into more production engagements.”

There is no technical or economic reason why the AMD GPU business can’t be as large as the AMD CPU business – except that Nvidia is a mighty competitor with its act together, and one that is entering AMD’s CPU space. Neither one sees Intel as much of a threat in GPUs, and both will compete fiercely with Intel in CPUs – and with each other and Ampere Computing and homegrown CPUs like Amazon’s Graviton – as 2022 turns into 2023.

This is going to get intense. Which is always good for customers, but not always for the black ink that is supposed to drain to the bottom line at chip designers.