For the first time in a very long time, and even including the Great Recession, chip maker Intel booked less revenue in the fourth quarter of the year than it did in the third quarter of that same year. And the culprit is a slowdown on many different fronts in its datacenter business, with enterprises and governments slowing spending at the same time that there is a slowdown in China that is rippling around the world and some of the companies that Intel sells chips too paid a bit slower than is usual.

All of these changes took Intel a little bit by surprise, with the company falling short of the guidance that it gave back in October of last year. And with the company posting a record year with $70.85 billion in sales, up 12.9 percent, and net income of $21.1 billion, up by a factor of 119.3 percent (that’s nearly 2.2X), there is really not much to complain about. Intel has about a quarter of its self-proclaimed addressable total addressable market of $300 billion, and it is every bit as profitable as it has been in recent years despite the difficulties it has had getting its 10 nanometer manufacturing processes to market.

But it is beginning to look like the growth engine is taking a breather for a while as companies consume the 14 nanometer “Skylake” Xeon SPs they have already bought and they await the 10 nanometer “Ice Lake” Xeon SPs that will be available towards the end of this year and early into next. The impending “Cascade Lake” Xeons, while offering some benefits over the Skylakes, look to be coming to market just as the server buying frenzy that occurred in the first three quarters of 2018 starts to slow. It is hard to say what is cause and what is effect here. The differentiation between Skylake and Cascade Lake Xeons may not have been sufficient for the big hyperscalers and cloud builders to spread out their acquisitions, and it could turn out that they just bought tons of Skylakes last year so they could sit out the Cascade Lake generation and wait to do big deals again with the Ice Lake Generation.

“We had three quarters and really, really strong growth in 2018 in the cloud, and that was driven by product cycle, as well as the typical multiyear build out pattern with Xeon Scalable,” Navin Shenoy, executive vice president and general manager of the Data Center Group at Intel, told Wall Street when going over Intel’s Q4 and full year 2018 financial results. “If you look back at all the historical trends we have had in the cloud business, we have always said there is some lumpiness to the business, and there is periods where people build and then there are periods where people consume. The signals we get from our customers are that the period of build for compute is going to shift now to a period of consumption, and that started in the second half in the fourth quarter and we expect that to continue through the first half of the year.”

It is important to not get the wrong idea, buy the normal decline from the fourth quarter of one year to the first quarter of the next year is on the order of 8 percent to 10 percent in the Data Center Group, and Intel’s chief financial officer and interim chief executive officer warned Wall Street that it could be double that in the first quarter of 2019. And it looks like the air pocket will extend out to the middle of 2019, when the Cascade Lake Xeons are expected to be shipping in volume and when AMD will be ramping up its “Rome” Epyc X86 server processors, too, and causing Intel a certain amount of competitive grief.

We have been wondering for years when the peak of the Xeon business would be crested, and we think that we just saw it in the review mirror.

Don’t get the wrong idea, though. This is an incredibly strong and profitable Data Center Group, and just because growth slows doesn’t mean Intel cannot dominate for many years to come. It just will not have the same level of control over the pace of technology and pricing as it has enjoyed for the better part of a decade because it has manufacturing issues and it has competition like it hasn’t seen since then.

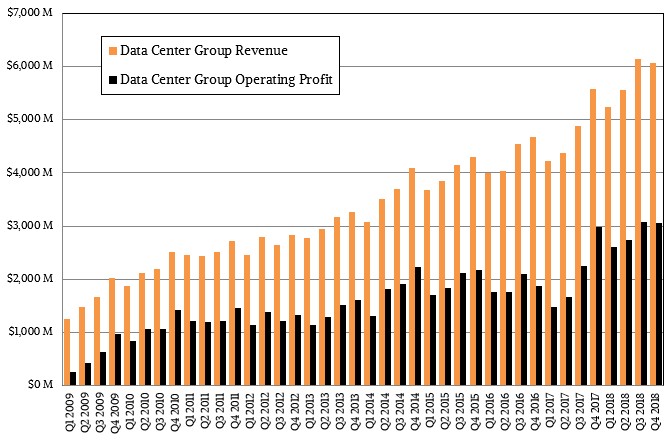

In the fourth quarter, Intel’s overall sales grew by 9.4 percent to $18.66 billion, and net income came in at $5.2 billion, a sharp rebound from the $687 loss it posted in the year ago period. During the quarter, platform sales at Data Center Group – which includes processors, chipsets, and motherboards – rose by 9.9 percent to $5.59 billion, and adjacencies – things such as Omni-Path and silicon photonics networking or Rack Scale Architecture, and custom server manufacturing – posted sales of $475 million, down 2.5 percent year on year. All told, Data Center Group had $6.07 billion in sales, up 8.7 percent, and posted an operating profit of $3.06 billion, up 2.1 percent.

It is hard to complain about the major part of a business growing by only 24 percent, as sales of products to the hyperscalers and cloud builders did for Intel’s Data Center Group did in the fourth quarter of 2018, but you have to remember for the first three quarters of 2018 together sales were up 45 percent – so that is a significant slowdown. And it radically impacts Intel’s sales because hyperscalers, cloud builders, and communications service providers now account for about two thirds of Data Center Group revenue, with enterprises and government only comprising a third of sales; this is a flip in shares of these two broad categories over the past decade. Swan said that server inventories out there in the channel were a little bit higher than usual, and that the company’s free cash flow was down $1.2 billion because of accounts receivable being higher than expected by that amount. It looks to us like server makers had been thinking the Xeon party would just keep on going full tilt boogie, and they bought a little ahead of the demand that can be expected in Q4 2018 and in the first half of 2019.

Communication service provider sales rose 12 percent in the fourth quarter, and enterprise and government sales fell by 5 percent; Swan said that the compares were tough for the latter, but the way Intel has been growing for the past decade, this has mostly always been true in any given quarter. Demand in China is being hurt, and you can bet that China will use alternatives to Intel, such as AMD Epyc chips and their Chinese clones and various Arm server chips and maybe even merchant or clone Power chips, as much as possible going forward.

But the main thing is that Intel believes that sales to hyperscalers and cloud builders will continue to grow, and Swan put a stake in the ground on the call with Wall Street. “In the long-term, the cloud business is going to continue to grow,” Shenoy said. “There is no doubt about that. Both the consumer cloud and the enterprise commercial cloud, we see both of those continuing to grow. And the appetite for compute, I think, is somewhat insatiable. Our five year forecast for compute cycle growth, or MIPS growth, is a 50 percent CAGR over the next five years. And I see nothing slowing that down over the next number of years.”

At some point, when hyperscalers and cloud builders are 90 percent of Intel’s business and enterprises and governments are only 10 percent, the profitability profile of the CPU and related businesses could be very different. Enterprises and governments do not get the same kind of volume pricing the hyperscalers and cloud builders do, and they are still one of the reasons why Data Center Group is so consistently profitable, and indeed, why the OEMs can still sort of make a living pushing tin.

As we have pointed out before, Intel’s actual datacenter business, which includes sales of flash and Optane memory, FPGAs, IoT gear, and other stuff to datacenter customers, is considerably larger than the Data Center Group as reported – and it also has a much lower operating profit, according to our estimates, and that is why you don’t see Intel actually break its revenues down into PCs on one side and datacenter on the other.

As best as we can figure, that “real” datacenter business at Intel brought in $7.77 billion in the fourth quarter, up 9.2 percent, and had an operating income of $3.26 billion, flat year on year and about 42 percent of that revenue.