The cloud gives, and it takes away.

The big hyperscalers, public cloud builders, and telecom, wireless, and cable service providers who are all collectively called “cloud” when it comes to the infrastructure they build, and they are increasingly driving shipments and revenues of all manner of components. But they command, by virtue of their huge volumes, discounts that are much deeper than the typical enterprise customer can get when they buy through an OEM or, if they are large enough, an ODM.

The fact that Intel’s Data Center Group is managing to profit pretty handsomely and reasonably predictably despite this tectonic transformation of the IT supply chain is a testament to its engineering, marketing, and sales organizations. So far, despite the fact that the market keeps indicating its wants an alternative to Intel in the datacenter, the market doesn’t seem to be buying into those alternatives except, thus far, as leverage to make deals.

That could change, of course. But it sure didn’t in the third quarter of 2017, when Intel set all-time sales records for Data Center Group.

In the quarter ended in September, Intel’s overall revenues rose by 2.4 percent, to $16.15 billion, and thanks to a cut in marketing, administrative, research, and development costs as well as the fact that Intel has restructured and had to book those costs in the year-ago period when it started that restructuring, the company was able to boost net income by 33.7 percent. It didn’t hurt that revenues were about $400 million higher than expected, with the cost cutting being better than expected, operating income during the period was $700 million better than Intel was anticipating for Q3 2017. Business is so good right now that Intel told Wall Street that it was raising its revenue guidance for the year to by $700 million to $62 billion flat, with operating income now guiding up $900 million to $18.8 billion for the year. Whatever competitive threats Intel has had in PCs and servers, it has dealt with them successfully, even if it has not cracked the smartphone market as has long been its desire.

As Brian Krzanich, Intel’s chief executive officer, told Wall Street in a conference call this week going over the numbers, the amazing thing is that even with 25 percent of the unit volumes coming out of the PC business in the past few years, Intel has managed to grow its profits as it has stabilized its revenues in PCs. And because chip manufacturing is a volume business because volumes drive down unit costs as they drive up chip yields and therefore profits, the PC is vital to Intel’s Xeon server chip line, just like the PC is vital to Nvidia’s Tesla GPU accelerator line.

Data Center Group is a big contributor to profits but is, as we point out above, dependent on its Client Computing Group and still does not deliver as much operating income as this PC business. But if trends persist, it will not be long before they cross. Perhaps in two years, maybe less. In Q3, the “Skylake” Xeons and their “Purley” server platform components of chipsets and motherboards were still ramping, and it is not clear how much revenue the Xeon SP line drove. It is not the kind of bump we have seen in years past, but then again, Intel has been shipping Skylake Xeons to big cloud builders since about this time last year, notably starting with Google and then Amazon Web Services before the Skylake chips were formally launched in July of this year, so the curves have to, by definition, be a little flatter.

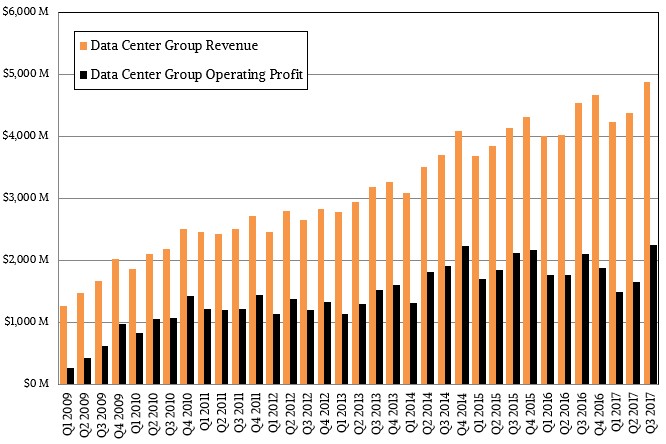

In the third quarter, the platform sales at Data Center Group – meaning Xeon and Xeon Phi processors, chipsets for them, and motherboards based on them – rose by 6.6 percent to $4.44 billion. Other revenues within Data Center Group, including stuff such as Intel’s Omni-Path switches and adapters among other things, rose by a more modest 16.1 percent to $439 million. Add it up, and Data Center Group had $4.88 billion in revenues, up 11.7 percent year on year and against a pretty tough compare when the “Broadwell” Xeon E5 v4 chips were shipping in volume. Operating income for Data Center Group was up 6.9 percent to $2.26 billion, and that was higher than the previous record for profitability for the glass house part of the business back in the fourth quarter of 2014, when it had $4.09 billion in sales and brought 54.5 percent of that to the middle line as $2.23 billion in operating income. Because of the restructurings, the costs of putting 14 nanometer processes in production for the Skylakes, and Intel’s work on 10 nanometer processors for all of its chips (with more allocation going to the servers than the PCs now that the Xeons are moving to the front of the process line, rather than the rear), the Data Center Group is not as profitable as it had once been. But, again, the PC business was shouldering the costs of ramping up yields, which made it look less profitable than it was and made the datacenter business look more profitable than it was.

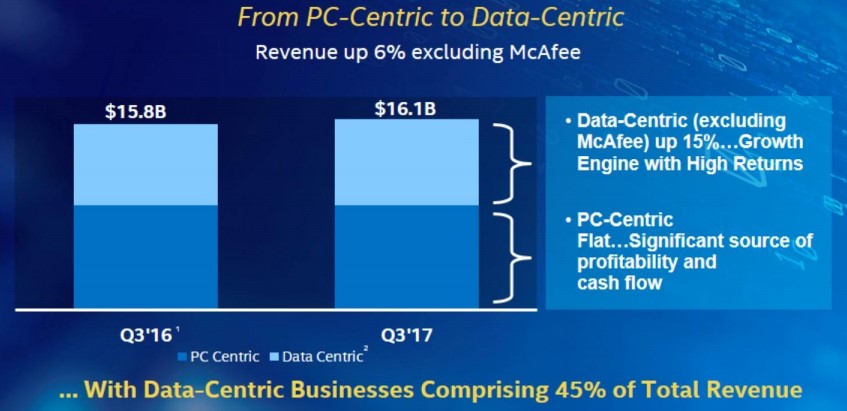

The way Intel talks about its business these days, it breaks the business into two pieces: the PC-centric part and the data-centric part, and here is how the breakdown looked in Q3:

The Q3 2016 data for the PC-centric part of Intel includes revenues for its former McAfee security software business and PC chips and chipsets and very likely some other peripheral sales. The data-centric parts of the business, according to Intel, include Data Center Group, IoT Group, Non-Volatile Solutions Group, Programmable Solutions Group, and a smattering of other stuff. (We have a slightly different way of characterizing this split.) The interesting bit is that the data-centric part of Intel is now driving 45 percent of its revenues, and has grown 15 percent this year and has higher returns in the aggregate compared to the PC-centric part of the business, which has flat revenues and profits. Those are still good profits, mind you. Client Computing Group as a whole had $8.86 billion in sales in Q3, down four-tenths of a point, but operating profits expanded 8.2 percent to $3.6 billion thanks to launches of desktop and laptop processors that are biting into AMD’s share of the PC segment.

“Our strategy is to be the driving force of the data revolution across technologies and industries,” explained Krzanich on the call. “Our data-centric businesses are the company’s growth engine. Individually, these businesses provide great value to our customers, and collectively, they are solving our customers’ problems in a way that no individual business or product could. We have built a collection of capabilities that is unmatched. At the same time, our PC business remains central to our success. It is a source of great profit, cash flow, scale, and intellectual property.”

Here at The Next Platform, we don’t much care about a technology until it passes through the glass house wall. So we are all about watching Data Center Group, and the adjacencies like FPGAs, flash and 3D XPoint memory, and the bits of IoT that relate to the datacenter.

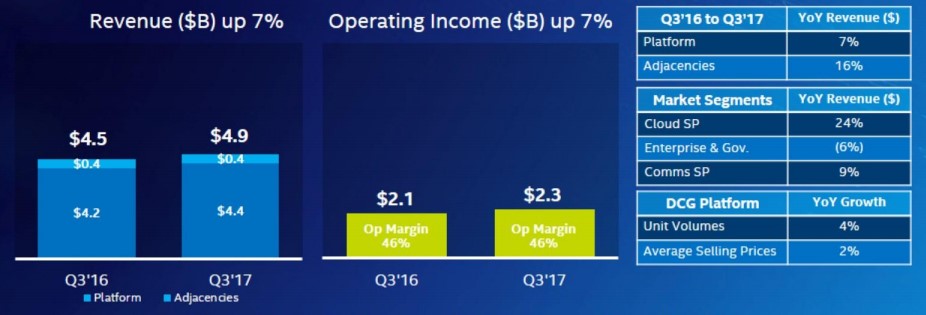

The interesting bit about this chart is that revenues for Intel datacenter products sold to cloud service providers rose by 24 percent, and sales to communications service providers were up by 9 percent. Sales to OEMs and ODMs who build products for enterprise customers and government agencies dropped by 6 percent. As has been the case for several years now, the enterprise sales have been a drag on Intel, and that is not a coincidence. The cloud and comms service providers now account for about 60 percent of Data Center Group Revenues, up from around 35 percent four years ago in 2013. This flipping of the revenue stream size between enterprises and service providers is the direct result of the cloud revolution, where infrastructure, platform, and software services are now commonly available and are being employed.

A few years ago, Intel though it could have its cloud and eat its enterprise, too, and grow revenues at 15 percent annually. But that is not happening because enterprises are shifting more and more compute and storage to the cloud. Enterprises pay more for technologies and give Intel and its OEM and ODM partners higher revenues and margins for any given product, and that is why Intel is only expecting operating margins to be a little north of 40 percent and revenues to grow in the high single digits for Data Center Group going forward.

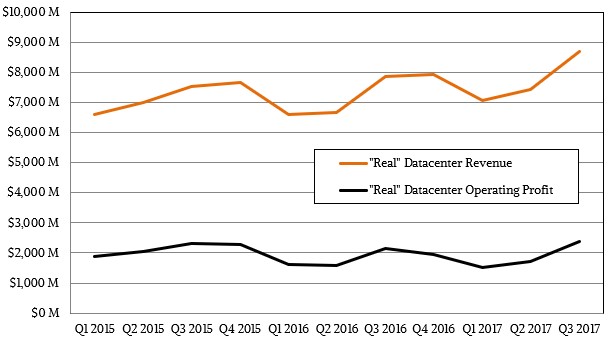

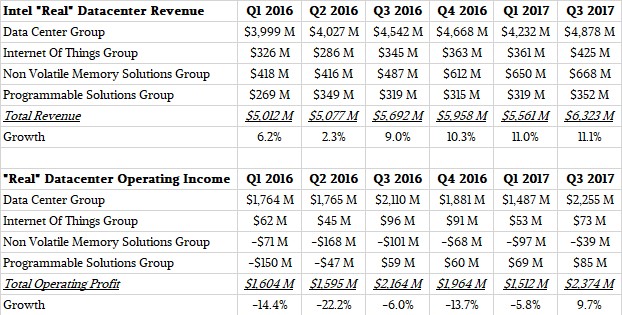

We like to try to reckon how much of Intel’s revenues are in the glass house, and add half of the IoT and 75 percent of the FPGA and non-volatile revenues together, and do a similar proportion of the operating incomes, to try to figure out what Intel’s “real” datacenter group revenues might look like. Here is the curve we come up with based in its 2015 financial formats:

And here is the raw data for this in a table:

Despite the huge premium that Intel and others are charging for flash memory, Intel’s Non-Volatile Solutions Group is still not quite making money, but it is getting closer. Intel says that its core NAND flash business is profitable. For Programmable Solutions Group, revenue was up 10 percent and the former Altera FPGA business had its largest quarter for design wins among large customers in the past three years. Operating margin growth outstripped revenue growth here, rising by 45 percent. This business is finally finding its feet inside of Intel and getting some traction.

In any event, the way we do the math, Intel’s “real” datacenter business had $6.32 billion in sales, up 11.1 percent, and operating income hit $2.37 billion, up 9.7 percent.

The cloud has not hurt Intel any more than anyone else, but the pressure from such customers is always going to be intense, and increasingly so as they grow. Intel may find itself wishing, some day, that enterprises wanted to own their systems rather than rent them. By then, Intel might also be wishing it had started the second cloud revolution – the one that stuck – in 2006 itself instead of leaving that to Amazon Web Services.