Hot on the heels of an updated contract with OpenAI that will see the AI model builder commit to spending an incremental $250 billion for Azure infrastructure, Microsoft has reported that it has a revenue backlog dominated by its Azure cloud that stood at $392 billion as the first quarter of its fiscal 2026 year ended in September. It may not be clear how OpenAI is going to get the money to honor those contracts, but Big Bill is sitting pretty with a $642 billion revenue backlog this week that is still growing as we speak.

Under that deal, Microsoft will have a 27 percent stake in OpenAI worth $135 billion based on the current $500 billion valuation that OpenAI had after its latest funding round in March this year, bringing its total to $57.9 billion not including share sales by early investors. That deal also includes giving Microsoft exclusive IP rights and model API exclusivity on the Azure cloud until artificial general intelligence – models matching the skills of humans – is reached. Microsoft also has secured GPT model rights out to 2032 in the event that AGI is not reached by 2030. Microsoft no longer has the right of first refusal on OpenAI buying compute capacity, and OpenAI can give API access to GPT models to an US national security customer (this was not defined in the statement, but was no doubt outlined clearly in the contract to include DHS, NSA, FBI, and CIA users).

The number of years for that incremental $250 billion to be spent was not revealed, but we think, as do others, that this runs out to 2032.

Satya Nadella, Microsoft’s chief executive officer, explained on the call with Wall Street analysts going over the Q1 numbers that Microsoft is not just running around trying to buy every GPU it can, building every datacenter it can, and chasing every GenAI customer that it can. The company has a decidedly calmer and methodical approach, which is why the company’s margin is not as diluted as the OpenAI deal (which no doubt has equity as a compensation for what would otherwise be a higher price for compute) and a heavy GPU fleet dominated by a few customers might imply. Take a listen:

“For us, again, it just always goes back to the core principle, which is build a fleet that is fungible across the planet and works for third party and first party and research. So that is essentially what we have done.”

“And so when some demand comes in a shape that doesn’t fit that goal, where it’s too concentrated, not just by customer, by location, by type of skewing. . . . When you think about the margin profile of a hyperscaler, you have got to remember this: The AI accelerator piece, but there’s compute, there’s storage. And so if all of the demand just comes for just one metric, that’s really not a long-term business we want to be in. That’s even from a third party. We have to balance it with all of our first-party stuff because that is, after all, a different margin stack for us. And then we have to fund our own R&D and model capability because in the long run, that is what is going to differentiate us.”

“And so I look at all of those, and we use all of that to make sure we are saying ‘Yes’ to all the demand that we want, we say ‘No’ to some of the demand that may be something that we could serve but it’s not in our long-term interest. And so that’s sort of the decision-making we have done, and we feel very, very good about the decisions. In some sense, I feel even better. Each time we say ‘No,’ the day after, I feel better.”

To fulfill that expanded OpenAI contract – as well as thousands of other “smaller” ones that would be very large in any other context – Microsoft is going to have to spend big bucks on infrastructure for Azure, and it indeed has done that in its first quarter. Microsoft spent an incredible $34.9 billion on capital expenses in the September quarter, which was 74.5 percent larger than the year ago period. And even with that, thanks to its $72.3 billion portfolio of investments that keeps swelling, the company was able to end the quarter with $102 billion in cash and equivalents as the September quarter came to a close.

One of the reasons why this is the case is that Microsoft has a vast base of productivity and enterprise application customers as well as the Windows platform on PCs and the Windows Server platform on servers, and now compute and storage capacity rentals on the Azure cloud.

In the September quarter, Microsoft posted sales of $77.67 billion, up 18.4 percent, and operating income was $37.96 billion, up 24.3 percent. After paying taxes and dividends, doing share buybacks, and some other stuff, Microsoft had a net income of $27.75 billion, up 12.5 percent and representing 35.7 percent of revenues.

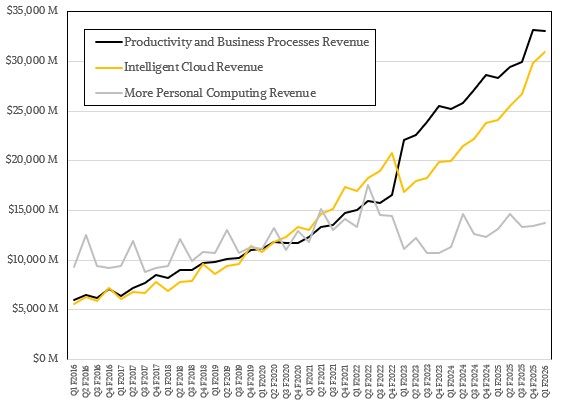

As The Next Platform, part of Microsoft that we care about most as the chronicler of platforms is the Intelligent Cloud group, which includes the Windows Server stack and Azure together. To be more precise, Intelligent Cloud encompasses Windows Server, SQL Server, Visual Studio, and other middleware and tools sold into the datacenter as well as compute, storage, and networking capacity on the Azure cloud, plus related platform PaaS and SaaS services Microsoft peddles into the datacenter and on Azure.

The Intelligent Cloud revenues were up 28.2 percent to $30.9 billion, with operating income of $13.39 billion, representing 43.3 percent of revenues and up 27.5 percent year on year.

To further confused everyone, Microsoft lumps all of its cloud-based software and services into a single category called Microsoft Cloud. This category (which is not a formal business group), includes Azure but it is not solely Azure. It absolutely includes anything sold under a utility model from Microsoft using its infrastructure – so think of it as infrastructure, software, and platform as a service for both servers and PCs all rolled up into one.

Microsoft Cloud revenues were just a tad over $49 billion, up 26 percent, with gross profits of 68 percent, which works out to $33.35 billion. (With all those billions, you can see how Microsoft can play the GenAI platform game.)

Microsoft does not break the Azure cloud out separately from this generic cloud category, but our model shows Azure brought in $20.72 billion, up 39 percent, and posted an operating income of $9.43 billion, up 45.1 percent and comprising 45.5 percent of Azure revenues. Azure has doubled in size in two years by our math, and there is no reason to believe it will not double in half the time given the GenAI boom.

Azure is only one way of using a Microsoft platform. The other way is to buy some servers, switches, and storage and build it yourself on a Windows Server stack. If you add up Azure with the Windows Server platform, you get what we call Microsoft’s “real” systems revenues and operating profit.

We think, based on our model, that Microsoft’s “real” systems sales in Q1 F2026 were $23.67 billion, up 43.3 percent, and operating profit for this collection of products and services had an operating income of $10.26 billion, up 42.4 percent and accounting for 43.3 percent of sales. This includes base operating systems and middleware, not databases and development tools that run on Windows Server, whether it is on premises or on the Azure cloud.