Making money in the information technology market has always been a challenge, but it keeps getting increasingly difficult as the tumultuous change in how companies consume compute, storage, and networking rips through all aspects of this $3 trillion market.

It is tough to know exactly what do to, and we see companies chasing the hot new things, doing acquisitions to bolster their positions, and selling off legacy businesses to generate the cash to do the deals and to keep Wall Street at bay. Companies like IBM, Dell, HPE, and Lenovo have sold things off and bought other things to try to recreate themselves in the market’s image, and while the jury is still out on such strategies, it is safe to say that they rarely produce the kind of rosy outcomes that CEOs espouse. It is far easier to create a niche in the business and build a monopoly or to take one away from someone else.

Hewlett Packard Enterprise is a classic example of a company that has been doing turnarounds so long that you can get a little dizzy watching. But even after shedding its services business a few months ago and even with its plans to exit most of its software businesses, HPE is still a pretty good bellwether for what is happening in compute in the datacenter thanks to its dominant position as the biggest revenue-generating supplier and volume leader in systems.

And HPE’s recent financial results are therefore not necessarily good news for those of us who believe that server sales are a leading indicator for what is going on in the IT sector. We do believe this to be the case, but we also know that the global IT climate is changing and old algorithms of prediction might not necessarily hold.

Commercial OEM suppliers like IBM, Dell, and HPE were faced with the option of exiting the portion of the volume server segment that is comprised by the top eight hyperscalers – Google, Amazon, Microsoft, Facebook, Baidu, Tencent, Alibaba, and China Mobile – who account for around a quarter of server shipments worldwide, or to compete with the ODM suppliers in Taiwan who undercut them on prices and who have been successfully building custom machines for the hyperscalers and now those who want to emulate them in the telco and enterprise sectors. Everyone is trying something to better chase the IT dollars.

- Cisco Systems emerged from nowhere eight years ago and carved out its piece of the server pie brilliantly, but put intense pressure on the OEMs and, equally importantly, forced all of the server makers to come up with their own networking.

- IBM, after a few years of this, threw its hands up and sold off its System x business to Lenovo, which in turn wanted to buy its way into the volume server business much as it bought its way into the volume PC business when it acquired IBM’s PC business a decade ago. This has not gone particularly well for Big Blue, which gave up control over hundreds of thousands of customers and thousands of reseller partners. Lenovo, for its part, is trying to keep Huawei Technologies, Sugon, Inspur, Dawning, and others in China at bay while competing in Europe and the United States against the OEMs and ODMs as well as Supermicro, which falls somewhere between the two categories.

- Dell, which wants to topple HPE as the world’s dominant system maker and which is trying to keep Lenovo at bay, spent tens of billions of dollars to go private and then spent tens of billions more to acquire EMC and VMware to bulk up its datacenter efforts. This strategy could work, but it is an expensive one.

- HPE bought SGI to move upmarket into the HPC and data analytics sectors with the company’s NUMA systems and expertise in simulation and modeling as well as connections in the US government. It has bought 3PAR, SimpliVity, and Nimble Storage to carve out more market share in converged and flash storage. And it has been chasing volume deals with its various OEM-style server lines. But growth has been easier to come by than profits, and then the shortages in DRAM and flash memory hit late last year and it has been exceedingly challenging for HPE and its peers in servers and storage. The spinoffs of HPE’s services and software businesses are happening just as the “Skylake” Xeon launch from Intel and the “Naples” Epyc launch from AMD are set to disrupt the server space, causing a pause in buying. (Timing is everything. The Compaq acquisition by HP closed on September 10, 2001.)

This server buying pause affects all server makers, but HPE is the biggest and most visible supplier and so it seems more alarming. It doesn’t look very pretty at HPE, and that is not good news for the systems business because it probably does not look very pretty at other server makers whose numbers are not public.

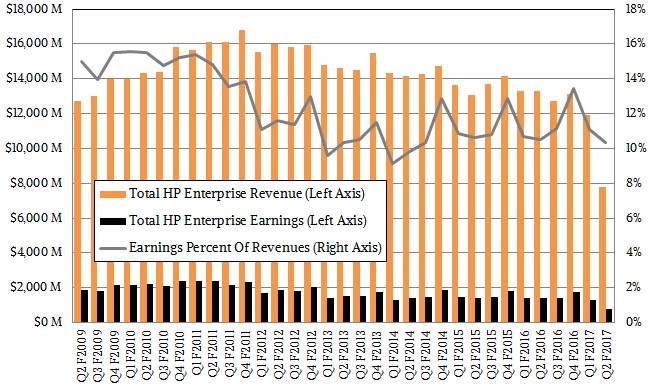

In the chart above, which shows the core HPE business since the Great Recession recovery started, the red Enterprise Services business has been discontinued as this was sold off to Computer Science Corp and the blue boxey line is about ready to go away once the spinoff to Micro Focus is complete. Basically, HPE becomes Enterprise Group, and it is absolutely dependent on shifting iron and selling support and financing for it.

Ask yourself this: What happens when no one who makes systems can make money on making systems? The tens of millions of organizations that use servers to run their businesses can’t all join Open Compute and engage the ODMs, and honestly, the 50,000 or so organizations that comprise the highest end of HPC, hyperscale, cloud, and enterprise computing and that are the main audience for The Next Platform, can’t do this, either. They buy servers in dozens to the hundreds, not in the tens of thousands, and they cannot command the attention of the key ODMs and must rely on the OEMs. It would be fascinating to see how the functionality and price/performance of hyperscale and OEM systems aimed at enterprises have diverged in the past decade, if such data were ever made public. (Which it will not be.)

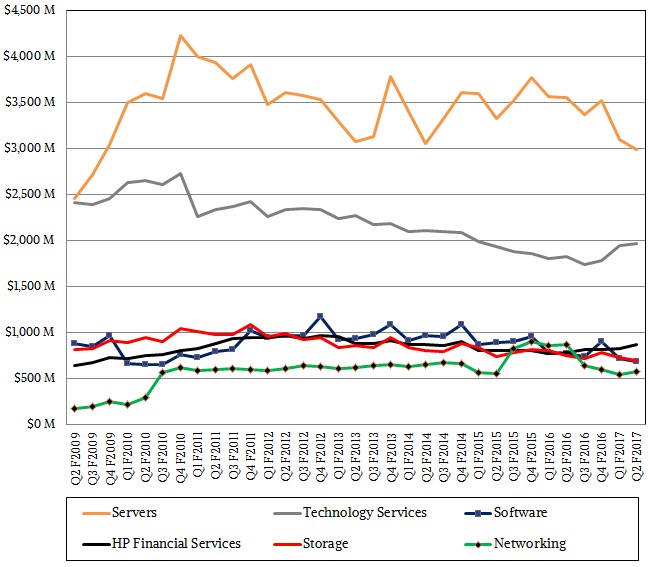

In the second quarter of fiscal 2017 ended in April, server sales were off 14 percent to just a hair under $3 billion, and to put that decline in perspective, that is half the decline seen for several quarters during the belly of the Great Recession back in 2008. While the beginning of the calendar year is never a particularly strong sales period, we think the impending Skylake and Naples launches from Intel and AMD did not help matters and, to make matters worse, those hyperscalers who could get Skylakes early don’t tend to buy their servers from HPE. Moreover, HPE said it had a stall among its tier one server buyers – HPE speak for what we call hyperscalers – and that made matters worse. It seems very likely that Microsoft is ramping up production on Project Olympus servers running AMD and ARM processors and these are not, as far as we know, being manufactured by HPE as the prior generation Open Cloud Servers were. Our point is, this is a big server revenue decline that HPE stomached.

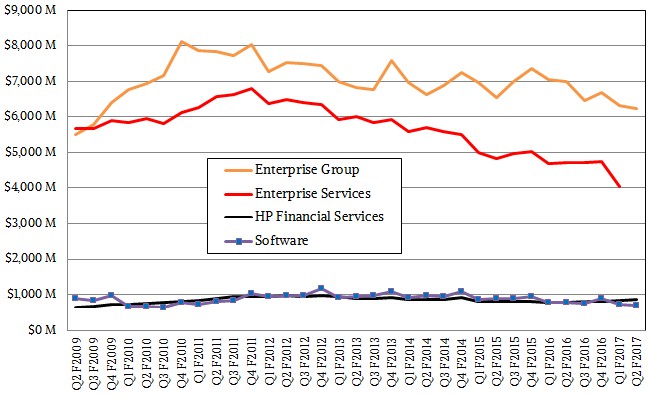

Here is what the new HPE looks like when broken out by operating categories rather than the larger groups:

The run rate in server sales is down by a third since the recovery from the Great Recession, and essentially, HPE has not been able to make it up in volume. Its storage and networking businesses do as well as any other server maker, but they never rivalled Cisco and EMC, the latter of which is now part of Dell. This gives Dell a tremendous amount of leverage in the enterprise datacenter.

Something larger may be at work here that is putting pressure on HPE and its peers. In a modern datacenter with distributed systems, networking accounts for about 20 percent of the cost of a cluster, and is rapidly growing to 25 percent. The remainder is split pretty evenly between servers and storage, and the lines are blurring between these categories, too, making quantification and classification even more difficult. Suffice it to say that you would think that HPE’s goal would be to have its Enterprise Group revenues reflect the market at large. But HPE only booked storage sales of $699 million in the second fiscal quarter, down 13 percent, and networking sales of $582 million, down 30 percent. Assuming that about half of HPE networking sales are for campus and branch office gear we don’t care about here at The Next Platform, then the ratio of networking to storage to server sales at HPE is something like 1:3:10 instead of 1:1.2:1.8 that we expect from the market at large.

HPE doesn’t have a server sales problem so much as a networking and storage sales problem. Taking on Cisco and EMC is not an easy task, or a cheap one. And carving out dominant share positions in a world with increasingly open and commoditized networking and storage makes it even harder to make money.

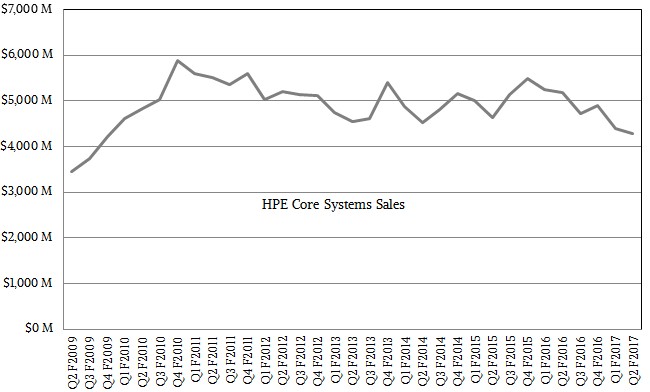

Having said all of that, HPE’s core systems sales has not collapsed as far as you might think. As the chart above shows, that core business of selling servers, switches, and storage exploded after the Great Recession due to pent up demand and acquisitions. The declines were pretty harsh in fiscal 2012 and 2013 as the competition ratcheted up and the hyperscalers had explosive growth and started doing their own things with the ODMs. Growth was tepid in fiscal 2015 and most of fiscal 2016, but really started to get hammered starting a year ago. It is now clear what HPE will do – or what it would be able to do even if it doesn’t think of it – to get its datacenter business in balance.

Cisco could always buy HPE and make some real trouble for Dell. But the larger problem remains. We can put together revenue streams in creative ways, but no one seems to be able to make the money that allows for reward for hard work and pays for innovation. HPE’s operating income used to run about 15 percent of revenues in the wake of the Great Recession, and now it is down to around 10 percent; real income after taxes and countless reorganizations, acquisitions, and divestitures is even lower, although it will be getting some cash for the spinoffs of the services and software businesses.

Our point is that in a world where there is no profit in the core IT systems in the datacenter, the cloud wins, and the big clouds become the primary route to market for compute, storage, and networking and they have tremendous pricing power and customer account control. This is certainly not going to be a friendly world for ODMs or component suppliers, and very likely not to customers, either.