We think that server spending is a leading indicator of economic growth or decline, and we are tracking the public companies that peddle systems to try to get a sense of how they are doing to get a better sense of what enterprises, governments, academic institutions, and other organizations separate from the hyperscalers and cloud builders, the latter of which comprise around half of server shipments and slightly less than half of server spending.

With Dell showing server revenue declines in the past two quarters (ending in the first few days of February and May, respectively, for its fiscal 2024 year that will end in late January or early February 2024) and Hewlett Packard Enterprise down in the second quarter ended in April (part of its fiscal 2023 year ending this October), we want to try to figure out what is going on. Today, we are going to look at Lenovo and Supermicro, both of which are only reporting their fiscal quarters ending in March and we won’t have a good gauge until we see what happens in the current quarter. We do have some forecasts here, so it lets us make some guesses and compare these two the most recent quarters from HPE and Dell.

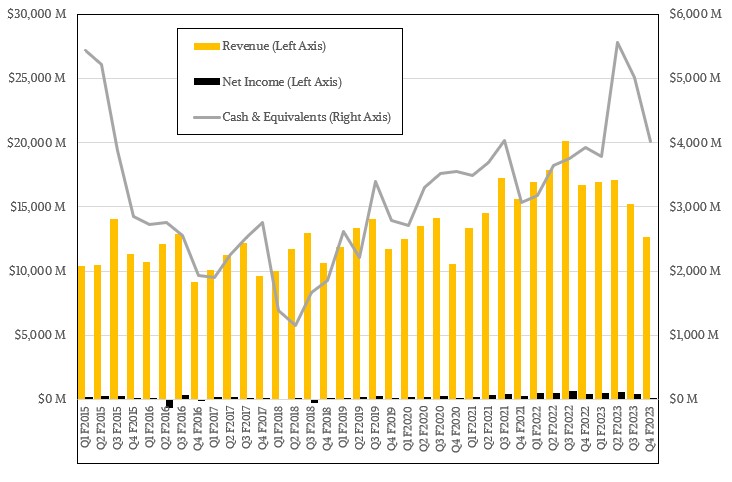

Let’s start with Lenovo. There was certainly no recession for the Sino-American server, storage, and PC maker happening then, and if recession means two consecutive quarters of decline, then by definition there will not be one when it reports its next quarter results, either.

In the quarter ended on March 31, Lenovo’s overall sales fell by 24.2 percent to $12.64 billion, and net income fell by 31.7 percent to a mere $106 million. That certainly hurt, and Lenovo also burned a little more than $1 billion in cash during the quarter, too, but its cash pile is nonetheless 33.6 percent larger than it was in the year ago quarter.

The culprit was the PC business, of course. Lenovo’s Intelligent Devices Group (IDG) stomached a 34.2 percent revenue decline, to just a tad under $9.8 billion, and its operating profit fell by 37.3 percent to $661 million. Despite the decline, Lenovo still maintained its position as the top PC seller in the world, and Yang Yuanqing, chairman and chief executive officer echoed the sentiments of many players in the PC racket that inventory burn down is proceeding and that growth will resume on the second half of this year.

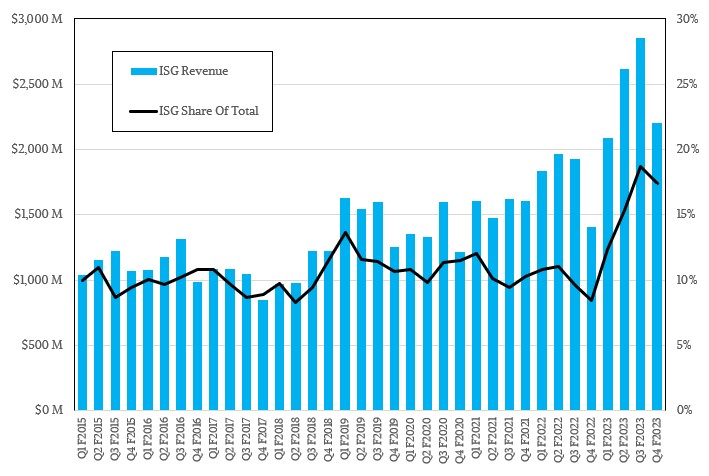

The company’s Infrastructure Solutions Group (ISG) is still growing like crazy, although it has experienced a dramatic decline sequentially from Q3 of fiscal 2023. Sales for servers, storage, switching, and other datacenter stuff at Lenovo rose by 56.1 percent to $2.2 billion, but operating income was flat at $7 million.

ISG accounted for 17.4 percent of total sales at Lenovo, which was down a bit from the 18.7 percent of total revenues in Q3 F2023 where Lenovo hit its all-time highest ISG revenue of $2.86 billion and brought $43 million down as operating profit.

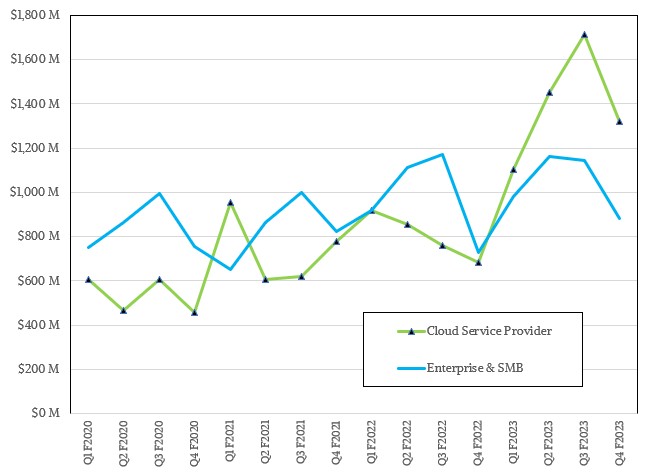

The Lenovo presentation did not talk about sales of infrastructure to cloud service providers in contrast to enterprises and small and medium business (ESMB) customers, but if the trends in Q3 were matched in Q4, then the CSP division accounted for $1.32 billion in sales, up 93.8 percent but down 22.9 percent sequentially, while ESMB rose by 20.9 percent to $880 million, and down by the same amount sequentially. (It is hard to say how to all played out, but we made out best guess based on what Lenovo told Wall Street.)

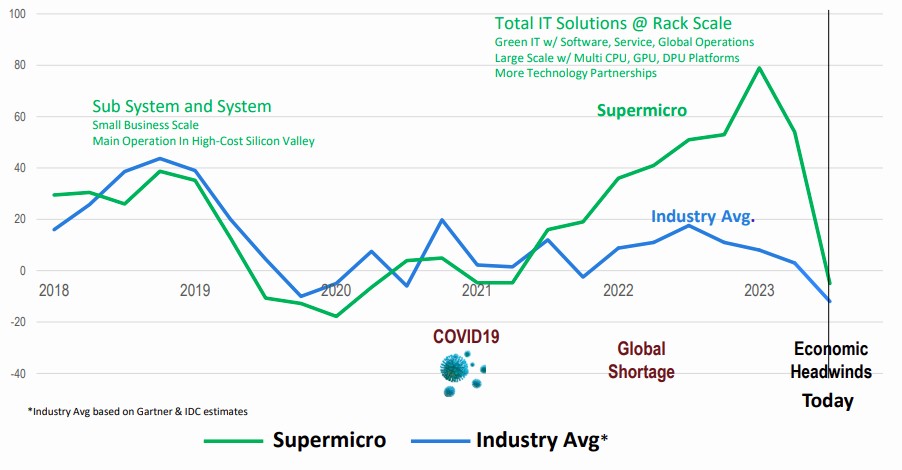

It is absolutely expected that Dell, HPE, Lenovo, and Supermicro would have sequential declines in the new year for their respective systems businesses. That is the normal trend set by IT budgeting practices for the past six decades. The hyperscalers and cloud builders – who are doing more business with Lenovo in China – have their own cycles, and the Intel and AMD CPU roadmaps drive cycles as well. The AMD “Genoa” Epyc 7004 launch last November helped, but the delay of the “Sapphire Rapids” Xeon SP until this January hurt. What is clear from the chart above is that Lenovo has found a new gear in peddling to the hyperscalers and cloud builders, although we don’t know any specifics about who of the Big Ten are buying from Lenovo. Wong Wai Ming, Lenovo’s chief financial officer, did say that CSP and ESMB both had double digit growth, and Kirk Skaugen, general manager of ISG, said that there was softness in ESMB in particular as the market researchers Gartner and IDC have pointed out. (In data that none of us can see any more without paying a fortune.)

“The ESMB segment will also capitalize on growth opportunity in AI-powered edge, hybrid cloud, high performance computing, and solutions for the telco communication sectors,” Wai Ming said on the call going over the numbers. “For the CSP segment, ISG has a unique ODM+ business model to address the growing demand for vertically integrated supply chains. The business will continue to diversify its customer base and capture new accounts through design win across technology platforms. The approach will achieve an optimal balance between general purpose and customized offerings while ensuring an appropriate scale and efficient cost structure to enable revenue growth and profitability expansion.”

Yuanqing added that based on its analysis of market share data, during fiscal 2023, Lenovo moved up to being the third largest server maker in the world, behind Dell and HPE, after being fourth behind Chinese rival Inspur, and moved from number eight to number five among external storage array makers. Skaugen said that in fiscal Q4, Lenovo’s server business grew by 29 percent, its storage business grew by 200 percent, and its related software business for infrastructure grew by 25 percent.

What Yuanqing has his eyes on is that the server space will grow to $132 billion in revenues, the storage space will grow to $36 billion in sales, and the edge will grow to $37 billion in sales as 2025 comes to a close – and Lenovo wants an increasingly large piece of those growing pies.

Lenovo’s Solutions and Services Group (SSG) turned in another good quarter, with revenues up 18.2 percent to $1.65 billion, but operating profit up only 3 percent to $324 million. Lenovo is obviously trying to be more profitable in its systems hardware business, but it has separated out software and services, which is reasonably profitable at the operating level of 19.7 percent of revenues in Q4. Other companies add these things together and we don’t get as much insight.

Lenovo did not provide a forecast for revenues for Q1 of fiscal 2024. So we will have to see how this plays out.

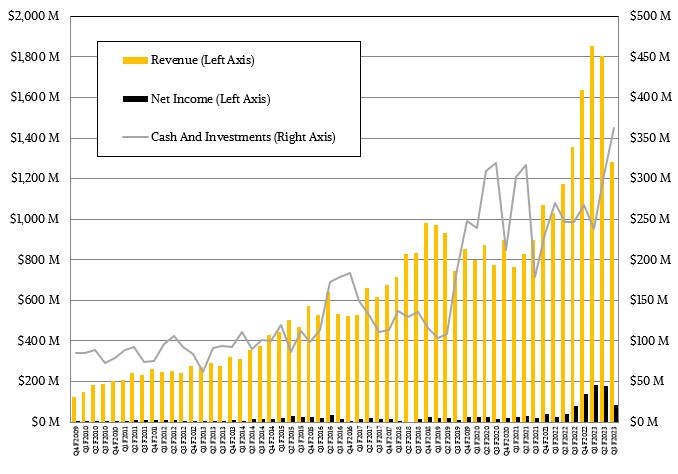

Supermicro had the same kind of sequential decline that its OEM peers did in roughly the same period as the first calendar quarter – which was Supermicro’s third quarter of fiscal 2023 – and the company did not make the numbers it had previously set for itself for that quarter. But unlike its peers, Supermicro did offer some guidance on how it hoped the current quarter was going to play out and how it would finish out the fiscal 2023 when it ends in June.

In the March quarter, Supermicro’s overall revenues fell by 5.3 percent to $1.28 billion, significantly lower than the $1.42 billion to $1.52 billion it was forecasting for that quarter. Supply chain was once again the culprit, although we strongly suspect that it was demand being bigger than supply more than the lack of manufacturing due to the coronavirus pandemic as happened more than once in the past three years.

“While the quarter did not unfold as we expected, I am strongly encouraged by our current business momentum as we navigate market uncertainties with our new generation X13, H13, and H100 leading edge products, especially in artificial intelligence,” Charles Liang, founder and chief executive officer at Supermicro, said on a call with Wall Street analysts. “These new AI product demands from top-tier companies have led us to challenges in terms of new key components availability. Compounded with the economic headwind, our Q3 results were reflective of these difficult yet opportune conditions. The good news is that we have already started to address these component shortage pressures over the past few months and we are in a much-improved situation going forward. We have started to produce and ship some back orders since April.”

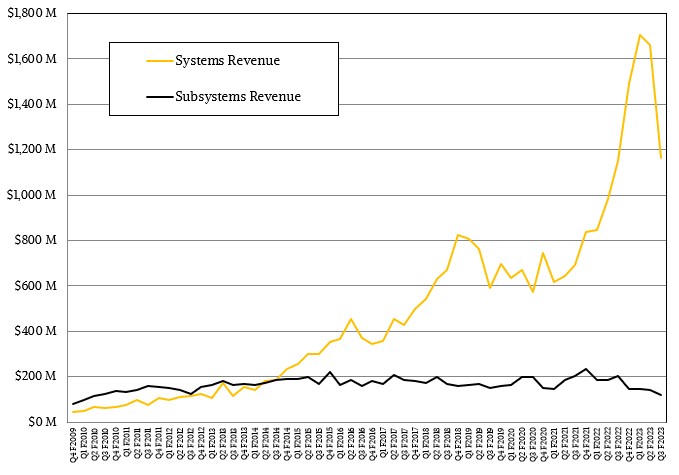

Liang added that Supermicro had just refreshed the entire Supermicro portfolio with new CPUs and GPUs from Intel, AMD, and Nvidia and that it set a record pace (against itself, not necessarily the overall industry) for design wins on GPU-accelerated systems, and said further that its complete, rack-scale integrated systems business continues to outpace its plain vanilla server or system component sales.

To that end, Supermicro is scaling up its manufacturing operations in the United States, Taiwan, the Netherlands, and Malaysia to support that revenue growth, and once again we will point out that there is plenty of empty factory capacity, power, and workforce – and lots of hyperscaler and cloud builder datacenters popping up, with Microsoft adding to facilities from Apple, Meta Platforms, and Google – right here in western North Carolina. Happy to show you around any time, Charles. . . . What’s better than building machines within driving distance from four of the biggest server buyers in the world?

With that out of the way, Liang said on the call that Supermicro was confident that it could drive between $1.7 billion and $1.9 billion in revenues in Q4 of fiscal 2024 ending in June, and said that if supply conditions improve sooner, then Supermicro would be above that range, presumably making up for the missed forecast from Q3. Liang still thinks that Supermicro can grow at least 20 percent this year, and that it can reach its goal of hitting $10 billion in annual sales over the next few years.

David Weigand, Supermicro’s chief financial officer, said that AI systems and pre-integrated rackscale systems together represented 29 percent of overall sales, or $372 million if you do the math, and said further that an existing cloud service provider customer became a greater than 10 percent customer for the first time.

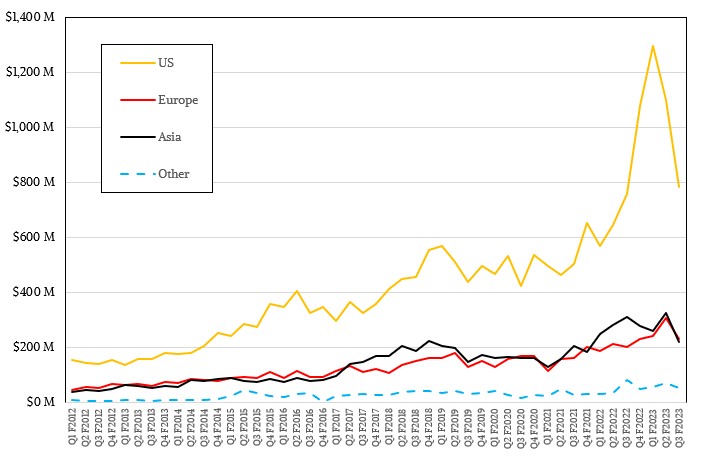

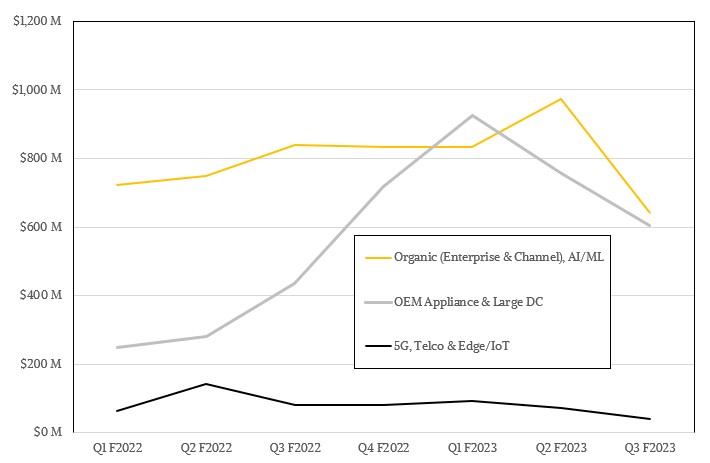

Which means it is not Meta Platforms, which The Next Platform readers who claim to be in the know, said this happened in Q2 already. We looked through the 10-Q filing with the US Securities and Exchange Commission, and it says one customer accounted for 10.7 percent of revenues in fiscal Q3 and one customer accounted for 11.8 percent of revenue for the nine months ended in Q3. Moreover, one customer accounted for 21 percent of accounts receivable in the nine months ended in Q3. That’s $1.04 billion from this one customer so far in fiscal 2023, and at least $130 million from the other customer in this quarter.

Based on the chart above, we strong expect both customers were located in the United States.

The upshot is that Supermicro had a 5.3 percent dip in Q3, which it blamed entirely on component shortages, and it is on track to do somewhere between 4 percent and 16 percent growth in its final quarter of this fiscal year. So unless something really weird happens in the next three weeks – like nuclear war – there is no server recession at Supermicro.

Maybe what is happening to Dell is Supermicro? And maybe what is happening to HPE and its former H3C alliance partner is Lenovo?

Anyway, if all goes as planned, Supermicro will bring in $6.64 billion to $6.84 billion in sales, and will be around two-thirds of the way to its goal of breaking through $10 billion in annual sales. At the midpoint of that Q4 range, Supermicro will grow 29.7 percent in fiscal 2023, and at this pace, it will break through a $10 billion rate sometime in the middle of fiscal 2025.

Charles Liang’s contagious enthusiasm, dynamism, and optimism (as seen in TNP’s interview pairing him with AMD’s Su, for example) is really quite refreshing, and just what the doctor ordered for this industry that, lately, has seemed a bit bipolar: morose, joyless, or tame on one side, and hyper-hallucinating on “superintelligence” and AI LSD on the other. Supermicro’s Liang feels like a breath of classical “can-do-attitude” fresh air in this field, today.