Intel can talk all it wants about how it beat its own expectations or those of Wall Street, but the fact remains that the first quarter of 2023 was downright ugly for the chip designer and maker. You can’t polish it, and you can’t roll it in glitter. But Intel can hope that this is as bad as it is going to get, or at least that it will only be this bad for another quarter or two.

In the quarter, Intel’s sales across all product lines fell by 36.2 percent to $11.721 billion, and the company swung from an $8.11 billion net gain in the year ago quarter to a $2.76 billion loss this time around. To be fair, the year ago quarter had a $4.32 billion gain on investments, which makes for a tougher compare than usual. After intense cost cutting, Intel has managed to retain $27.53 billion in cash and investments, although that cash pile is 38.4 percent lower than it was a year ago.

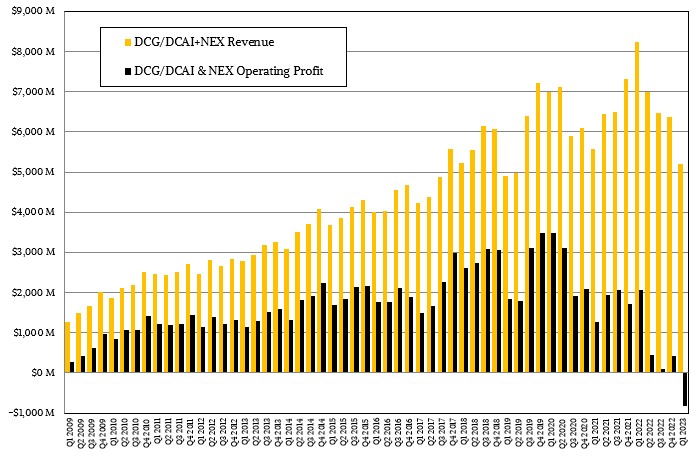

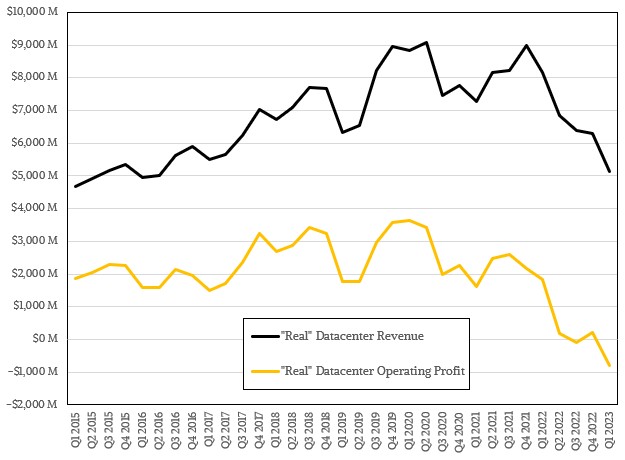

In the quarter ended in March, the Data Center & AI group, which is where server infrastructure mostly live and which is predominantly driven by sales of Xeon SP CPUs, revenues declined by 38.4 percent to $3.72 billion. According to Intel’s 10-Q filing with the US Securities and Exchange Commission, and picked up by our good buddy Aaron Rakers over at Wells Fargo, Intel’s Xeon XP server shipments were off 50 percent in the quarter. By comparison, server CPU shipments in all of 2022 were off 16 percent.

Small wonder, then, that the DC&AI group had an operating loss for the first time and in fact this is the first time we can remember that Intel’s datacenter business, under any name, posted an operating loss. DC&AI had an operating loss of $518 million, compared to a gain of $1.69 billion in the year ago quarter. On a trailing twelve month basis, which is perhaps the best way to gauge Intel right now because the remainder of 2023 will at best be a mirror image of the last two quarters of 2022 plus the first quarter of 2023, DC&AI had $16.88 billion in sales, down 29.1 percent, and operating profits have declined by a factor of 100X to a mere $84 million.

The Programmable Solutions Group, the former Altera FPGA business and something that should be called a division not a group if it is tucked inside of the DC&AI group, was a bright spot, with record revenues for the second quarter in a row and an increase of 36 percent year on year. Intel has been able to drive up average selling prices for FPGAs while at the same time getting better supply of the devices, thus eating into order backlogs and driving up those revenues.

The Network and Edge group, abbreviated NEX and comprised of products that would have been in the old Data Center Group or scattered into other groups, had sales of $1.49 billion, down 32.7 percent, with an operating loss of $300 million, from a gain of $366 million in the year ago period. On that same trailing twelve month basis, NEX sales are down 2.9 percent to $8.15 billion and operating profits are down by a factor of 25X to $74 million.

Considering how profitable Data Center Group was for so long, this is a bit of a shock to the Intel financial system and to its ego. It would have been better for Intel to have remembered that it needed to keep pace with Taiwan Semiconductor Manufacturing Co with process nodes and with investments in its foundry. One is reminded of the hubris of International Business Machines in the late 1980s and early 1990s. But Pat Gelsinger, who trained by the side of Intel’s founders, is back and cleaning up the mess as best he can and one is hopeful that a competitive compute engine designer and manufacturer can emerge from that mess. History suggests that Intel can revive itself – that is how it moved from being a memory maker to being a CPU maker in the 1980s and also how it recovered from the first attack on its server base from AMD in the 2000s, emerging with a product line that made historical levels of profits. And frankly, if AMD can recover, so can Intel. But when it does, there will be two strong X86 players that will turn around to see the Arm collective and the RISC-V collective coming for them both. . . .

But as far as we can tell, there is a lot more pain still to come and Intel is going to have to work very hard to restore its reputation as a semiconductor manufacturer and a chip designer. This would have been easier if there was not a collapse in the PC market at the same time Intel was facing such intense competition in datacenter compute and trying to get its foundry back to the leading edge.

“As the industry continues to navigate through multiple global challenges and headwinds, we remain cautious on the macro outlook, even as we expect some modest recovery in the second half,” Gelsinger explained on a call with Wall Street analysts going over the numbers. “We are seeing increasing stability in the PC market, with inventory corrections largely proceeding as we had expected. However, the server and networking markets have yet to reach their bottoms as cloud and enterprise remain weak. As a result, our Q2 revenue guide embeds continued inventory corrections in our core markets and a range of normal seasonal to better-than-seasonal growth off depressed Q1 revenue levels. We remain focused on what is within our control and steadfast in our commitment to advancing our strategy.”

When you are going down the Colorado River in a raft, all you can do sometimes is hold on and hope the pilot is steering correctly.

Intel still believes that the PC market will rebound at some point – and there are some who don’t – and Gelsinger said that the “Q1 consumption TAM” for servers declined both sequentially and year over year at an accelerated rate and said further that Intel expected that the TAM for servers for the first half of 2023 would decline, with a recovery in the second half of this year. “While all segments have weakened, we would reiterate that the correction in enterprise and rest of world, where we have stronger positions, is further along and will likely recover more quickly. Lastly, in our broad-based markets like Industrial, Auto and Infrastructure, demand trends are relatively stronger. Although, as anticipated, NEX did see a Q1 inventory correction that we expect will continue for the next couple of quarters and likely will cause NEX revenue to decline this year.”

Gelsinger went over the good news, such as it is, about the process and server processor roadmaps, which we covered here a month ago, and we are not going to repeat it for emphasis as Intel keeps doing because, well, what else do you expect it to say? Gelsinger did add the fact that Arm Holdings has signed a multi-generational agreement with Intel to be able to get its chip IP compatible with Intel’s 18A RibbonFET technology, which is a gate all around (GAA) transistor architecture that Intel says will reach parity or exceed whatever the industry – meaning TSMC – can deliver at the time in 2025.

We shall see at the time, and it would be funny as hell if someone would make a chip using TSMC 2 nanometer and Intel 18A so we could compare the differences, literally. But that would be a service that might cost $50 million to $100 million, and no one in the chip industry is in the mood to waste money to prove who has the best chippery transistory.

Some other housekeeping items that are relevant.

First, AXG has been split into two and part of it has gone into the Client Computing group (CCG) and another part has gone into the DC&AI group. In the wake of Raja Koduri leaving Intel a month ago, the company has hired Deepak Patil, who was running the APEX cloudy infrastructure business at Dell and who headed up engineering for Virtustream, who built Oracle’s cloud, and who was a founding member of the team at Microsoft, to run AXG. We have said that AXG was created solely to keep the heavy investments in GPU technology from hitting the operating income of the DC&AI and CCG groups, and now that AXG has been sliced up and jammed into them, you can see the effect on the operating income is not good.

It is not entirely clear what running AXG means. Is it really a division that spans DC&AI and CCG? And what is Patil’s role? We hope to speak to him about how this will all work. AXG should be an architecture group that feeds down (or up or across) into DC&AI and CCG, and maybe that is what it is now. Jeff McVeigh, who has been running AXG for the past month, goes back to running the Super Compute Group, which is focused on HPC simulation and modeling and AI training and inference in the datacenter.

Second, Intel has shut down its server manufacturing business. It has signed an agreement with Mitac, the Taiwanese system and motherboard maker that owns Tyan, to have it work with Intel’s server customers and use Intel’s designs to allow them to add machines to their fleets.

Third, the silicon photonics business that was part of NEX and the foundry automotive business that was part of Intel Foundry Services have been pulled out of those groups and are now reported in the Others category. If silicon photonics doesn’t belong in either DC&AI or NEX, where does it belong?

Intel DCAI and NEX q1 net on financial = $388 sans tax accrual down to $288 pulling taxes from net. Net is determined from $1K AWP on channel DCG primarily equals $2128.37 delivers gross per unit on financial $728. Q1 gross down 32% from q4 and net down between 27% and 46%. For q1 2023 DCAI and CCG appear to be operating at marginal cost = marginal revenue sufficient to produce every next unit on a cost basis and NEX a looser suspect cleaning house. Zinsner implied first half as a (marginal) cost half and second half up to “100%” the marginal revenue half. I have DCAI production volume in q1 at 9,587,463 to 12,922,052 that is up 18% to 58% over q1 dependent net take range low to high. NEX 3.8 M to 5 M units. Altera within DCAI suspect 400 K to 500 K units of production as a curiosity it’s hard to say. First half 2023 appears to be a heavy Sapphire Rapids sample time any my bet is fully populated boards tied to an Emerald Rapids procurement agreement. Whether DCAI SR sampling or Core goosing the channel with high margin as a market share keeper, or NEX clearance, Intel gave the store away in q1 2023.

Mike Bruzzone, Camp Marketing

I see another article on the google A3 AI supercomputer. Each node with a couple of Intel SPR chips and an Intel designed Mount Evans IPU.

Intel can put HBM in-package on SPR-HBM and on Ponte Vecchio … and no need for TSM. They would have a problem ramping Gaudi 3 if they are still relying on TSM for the packaging, but the point of IFS is that Intel can package up tiles built at TSM … as they are doing with PVC.