We know, as you do, that artificial intelligence is driving a lot of spending at IT organizations and is probably the fundamental driver of spending by the hyperscalers and cloud builders that have, thus far, benefitted most from the machine learning revolution.

But just how much money are companies sinking into AI, and how will that grow over time?

We have not seen a lot of good data on this, and the market researchers at IDC, as usual, have been the most vocal about how they dice and slice the AI market in their public statements, which dribble out some insight here and there to keep their name out there and to drive deeper engagements with AI startups, their investors, IT suppliers who are chasing this market, and large enterprises that are on the forefront of commercializing AI in their application stacks.

What sent us down this AI spending rathole was some numbers that IDC released on March 7, which talks about worldwide spending on AI-Centric systems, including hardware, software, and services. AI-centric means that without the AI component, an application will not function. So AI augmentation is not enough. But those scenarios where AI helps and application perform better, but the absence of it does not cause the application to stop working, are lumped into an AI Non-Centric category, which has been a bigger part of the overall AI market historically but which is not growing anywhere as fast as the AI-Centric part.

We did some poking around the IDC site and found statistics and forecasts put out in February 2022, July 2022, and September 2022, and we have tried to weave this into a coherent dataset to get a sense of what the AI market really looks like. As usual, we extend and enhance this information where we can and anything shown in bold red italics is data we either derived from a trend (usually projecting backwards to fill in a gap in the data) or from a chart where we count pixels to get a sense of the underlying raw data that IDC has not supplied. Anything in blue was derived either by using the compound annual growth rate to fill in the gaps between the endpoints in a forecast or derived through simple subtraction.

We do not warrant that this is the IDC data except where shown, bur rather give you some back of the envelope estimates from the IDC data so you can see how things might be changing. If you want the complete set of real data, which is no doubt more complex and more complete, call IDC and give them some money.

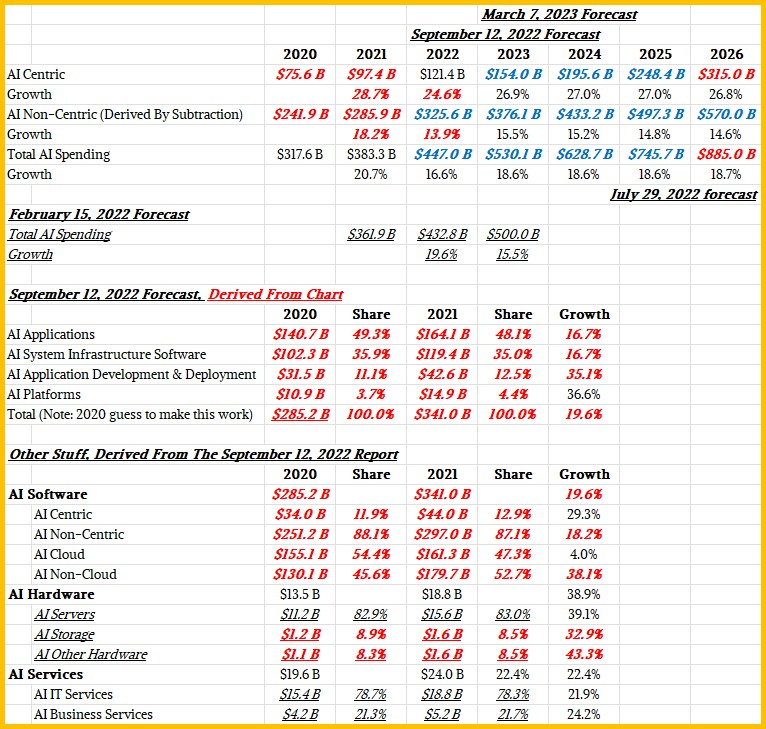

Here is everything from these IDC statements brought together into one table:

In the March 2023 report, IDC said that spending on AI-Centric systems is forecast to reach 154 billion in 2023, up 26.9 percent compared to 2022 and therefore there was $121.4 billion in such spending in 2022. The market is expected to “surpass $300 billion” in 2026 with a CAGR of 27 percent between 2022 and 2026, and these numbers shown in blue bold italics fit that description. To make the CAGR work out, the sales of AI-Centric systems in 2026 has to be $315 billion.

In the July 2022 report, IDC said that the overall AI market for hardware, software, and services would “reach the $900 billion mark” by 2026 and grow at an 18.6 percent CAGR between 2022 and 2026. In the September 2022 forecast, IDC said that total AI spending was $383.3 billion in 2021 and was projecting that it would reach nearly $450 billion in 2022, and to make this all sorta fit, then the overall CAGR for AI spending has to make it hit $885 billion by 2026. (That rounds up to $900 billion.)

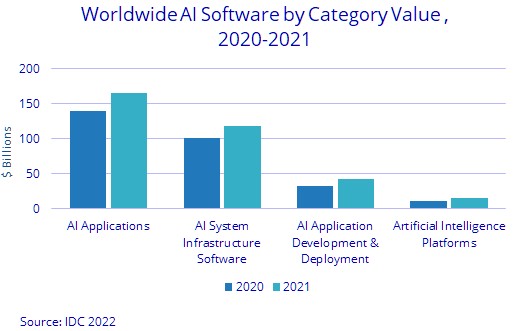

That September 2022 report had this interesting chart in it, which broke down worldwide AI software spending in 2020 and 2021:

The numbers shown at the bottom of the consolidated table above are done using pixel counts converted to dollars. (The error of margin is a few percent, give or take, given the resolution of the imagine, we reckon.)

This is very much a software and services market, and AI hardware is a relatively small, but growing part of the overall global AI hardware market.

“AI hardware was both the smallest ($18.8 billion) and fastest growing (38.9 percent year over year growth) segment of the AI market,” IDC writes. “The hardware growth was driven by efforts to build dedicated AI systems capable of meeting the increased compute and storage demands of AI models and data sets. While both AI servers and AI storage delivered strong growth in 2021 – 39.1 percent and 32.9 percent respectively – server purchases were notably larger at $15.6 billion.

You will note that storage and networking together represent only 17 percent of the costs of AI hardware. This is absolutely consistent with the way petascale and exascale HPC systems are priced. Every penny that can be spent on compute goes into compute.

AI services accounted for $24 billion in 2021, up 22.4 percent from 2020.

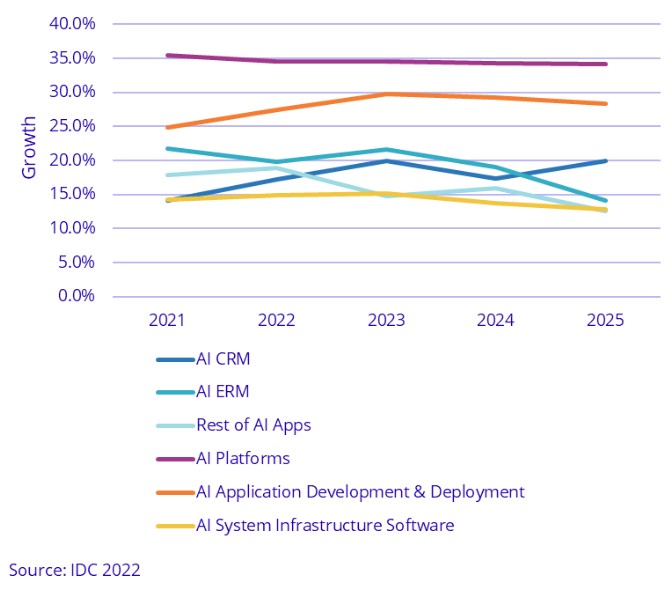

This chart from the February 2022 forecast was interesting in that it showed growth rates for AI software spending by category between 2021 and 2025:

It is too difficult to reverse engineer this and apply it to the 2021 numbers and try to rectify it to the 2022 through 2026 forecast. The important thing is that the growth rates are pretty steady across the categories of AI software and quite high at that.

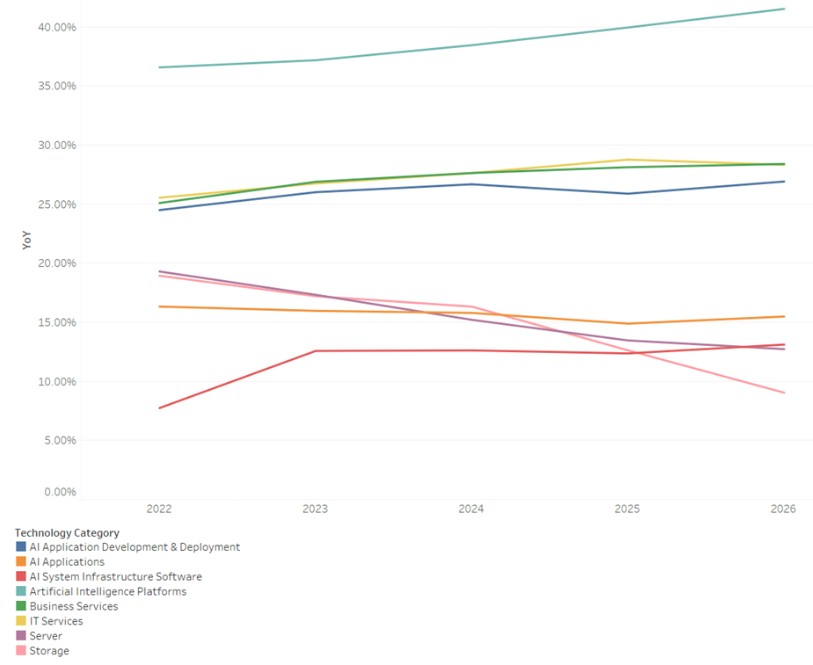

Ditto for the overall spending growth rate forecast chart put out in the July 2022 forecast:

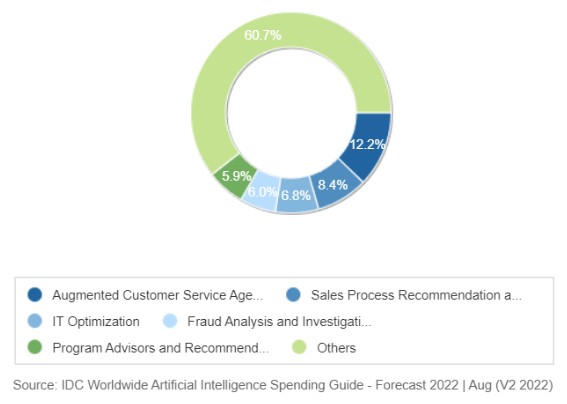

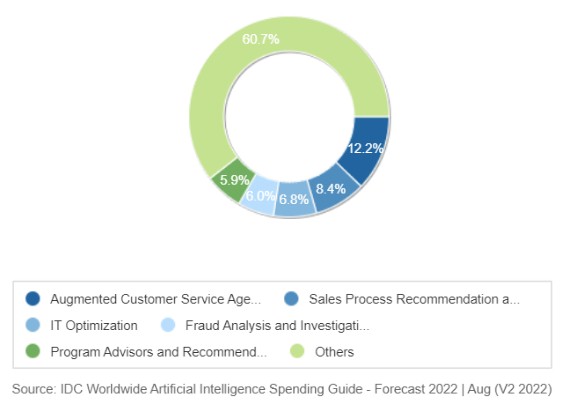

These use case ring pie charts from the September 2022 and March 2023 are interesting. Take a look at this one:

And then this one, which dices and slices the market share of revenue a little differently:

Perhaps the most significant thing is that over the 2022 to 2026 forecast the 26.5 percent CAGR for overall AI-Centric spending is more than four times as high as the growth rate of the IT market overall, which is expected to grow at 6.3 percent CAGR over the same timeframe. Looking at IDC’s latest IT spending forecast, which has about $1.4 trillion in spending for IT of all kinds globally by 2026, then this AI-Centric spending represents a little less than a quarter of all IT spending, and if you add in the AI Non-Centric investments, that number rises to nearly two thirds of spending in 2026.

The rest is really all about maintaining the stack in place.

So, now you know what the IT plan is for the next four years for the entire world. Carry on.

Be the first to comment