When Taiwan Semiconductor Manufacturing speaks, the datacenter sector of the IT industry listens because, with few exceptions, this foundry etches the compute, networking, and storage engines that power the datacenter. And the rest of the entire IT industry also listens, particularly the smartphone industry and a good portion of the PC industry (the part not controlled by Intel), because TSMC is also for the most part their foundry.

So TSMC is perhaps the best indicator of how the semiconductor industry is doing, and what it will be doing based on the capital expense and revenue guidance that TSMC gives.

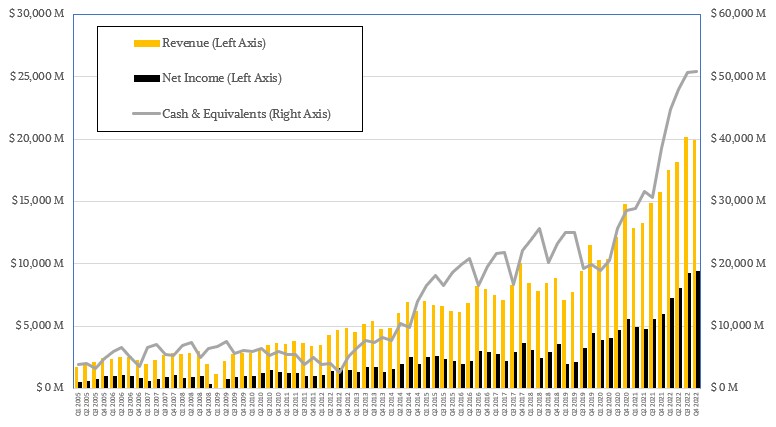

In the fourth quarter ended in December, TSMC’s revenues rose by 26.7 percent to $19.93 billion, and the company brought an incredible 47.3 percent of revenue – that is $9.43 billion – down to the bottom line. If this were any other business, we would be telling you that within a few years, TSMC would have competition crawling all over it with such high profits.

But the foundry business is different. The chip factory in Arizona that TSMC is building to etch 3 nanometer chips in 2026 costs on the order of $28 billion, more than twice the $12 billion the company earmarked for the 4 nanometer foundry in the same location. This is a crazy capital intensive space, and it takes a hoard of engineers with all the intellectual property in the world to make it all work properly.

Small wonder Intel wants to be in the foundry business and not just make chips for itself.

Running a fab, when it is done properly like TSMC is doing it, is far more profitable than the hyperscalers and cloud builders who, ironically, depend heavily on chips manufactured by TSMC. In the first nine months of 2022, Google brought 30.4 percent of its revenues to the bottom line and Meta Platforms did 22 percent; Apple did 25.3 percent in its fiscal year ended in September 2022 and Microsoft did 32.2 percent of revenue in its fiscal 2022 ended in July 2022. For the full 2022 year, TSMC, by comparison, brought 44.8 percent of its revenues to the bottom line, which was just a tad over $34 billion. Enough to cover that fab in Arizona with some cost overruns to spare, but a crazy profitability. One might even be tempted to call TSMC a monopoly in high end chip manufacturing, and its ability to command such high prices for its services, yielding such high levels of profitability, pretty much means it is a monopoly. TSMC’s share of the relevant market for high-end chippery is nearly 100 percent aside from the chips that Intel makes for itself excepting some GPUs and CPUs made by Samsung in recent years.

So, oddly enough, the industry needs for Intel to be a second foundry, not just a self-serving chip manufacturer, and for Samsung to continue to expand out to CPUs, GPUs, and other circuits to help drive down the cost of chip manufacturing even as Moore’s Law declines and chip packaging challenges try to drive it up.

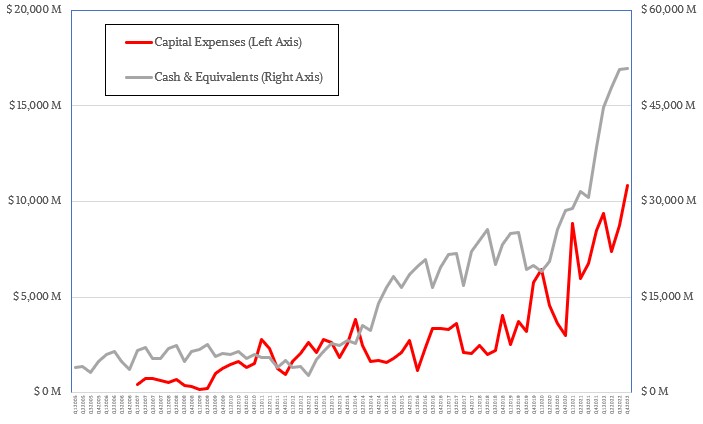

In Q4, TSMC spent $10.82 billion in capital expenses, up 27.9 percent year on year, and ended the quarter with $50.84 billion in cash, up 32.1 percent. The ratio of capital expenses to cash and equivalents is lower than the average over the past two years, but not by that much. The company spent a total of $36.35 billion on capital equipment and other expenses in 2022, an increase of 21 percent compared to 2021 and driven by investments to build out 5 nanometer factories and ramp up 4 nanometer and 3 nanometer etching across its factories in the Taiwan, China, and the United States.

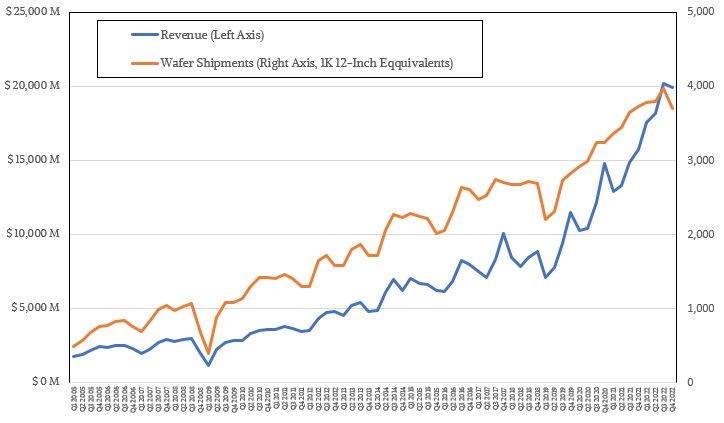

One interesting data point is that wafer starts took a bit of a dip sequentially and wafer starts took an even bigger dip in the fourth quarter as there was a bit of a glut in the semiconductor space. Take a look:

Revenues in Q4 were down 1.5 percent sequentially from Q3, but wafer starts fell by a considerably larger – and potentially more ominous – 6.8 percent to 3.7 million 12-inch wafer equivalents.

Looking ahead to the current first quarter of 2023, Wendell Huang, chief financial officer at TSMC, said on a call with Wall Street analysts that gross margins were at 62.2 percent in the fourth quarter, but because of under-utilization of its fabs this quarter it would see gross margins in Q1 2023 around 54.5 percent. Those margins are lower because of unfavorable currency exchange rates but mostly because of lower demand from PC, smartphone, and datacenter chip customers. This year, gross margins will be impacted by inflation, the fabs in Arizona (which are more expensive than the ones in Taiwan and China), and the 4 nanometer and 3 nanometer ramps.

Huang added that TSMC was expecting for its capital expenses to be somewhere between $32 billion to $36 billion in 2023, which is flat to down 12 percent. Of this, about 10 percent of the capital will be spent on packaging and mask making, 20 percent will be spent on “specialty technologies,” and 70 percent will be spent on advanced process technologies. (The specialty technologies are based on processes with 28, 22, 16, and 12 nanometer geometries, and seem to be largely focused on the foundry being set up in Japan.)

Our guess is that capital plan for 2023 means spending on 4 nanometer and 3 nanometer equipment and fabs will remain the same, and expansion of 5 nanometer facilities will be curtailed to match slowing demand. We strongly suspect that the mature 7 nanometer processes are humming along and making good coin for TSMC and it doesn’t have to do much except take the orders and run the masks. The trouble is that demand for chips using the 6 nanometer and 7 nanometer processes – chips for smartphones and PCs for the most part – is declining.

For the full year, CC Wei, chief executive officer at TSMC, said the company grew 27.9 percent against a semiconductor industry (minus memory, which is its own animal) that grew at around 10 percent according to the latest estimates.

“As customers and the supply chain continue to take action, we forecast a semiconductor supply chain inventory, while reduced sharply through first half 2023, to rebalance to a healthier level,” Wei said on the call. “In the first half of 2023, we expect our revenue to decline mid to high single-digit percent over the same period last year in US dollar terms. Having said that, we also start to observe some initial signs of demand stabilization and we will watch closely for more signals. We forecast the semiconductor cycle to bottom sometimes in first half 2023 and to see a healthy recovery in second half this year. In the second half of 2023, we expect our revenue to increase over the same period last year in U.S. dollar terms. For the full year of 2023, we forecast the semiconductor market, excluding memory, to decline approximately 4 percent, while the foundry industry is forecast to decline 3 percent. For TSMC, supported by our strong technology leadership and differentiation, we will continue to expand our customer product portfolio and increase our addressable market and we expect 2023 to be a slight growth year for TSMC in US dollar terms.”

Wei added that over the long haul, the 6 nanometer and 7 nanometer processes (6N and 7N in the TSMC lingo) would be “a large and long lasting node” and that the downturn is a cyclical rather than a permanent thing. The N3 3 nanometer process that has been ramping in its Taiwanese factories entered volume production late in the fourth quarter – as planned and with good yield, according to Wei. Demand for the 3N process exceeds supply, and 3N is expected to contribute a middle single digit percentage of total wafer starts this year. The N3E enhanced 3 nanometer process aimed at high end chips (what TSMC calls HPC, which is not precisely the same as our HPC) and smartphone chips will go into volume production in the second half of 2023. The combined 3N and 3NE processes have twice the number of tape-outs as the N5 process had in its first two years. So demand is clearly going to be high here. The 2 nanometer N2 process will start volume production in 2025 and is being ramped in foundries in Taiwan.

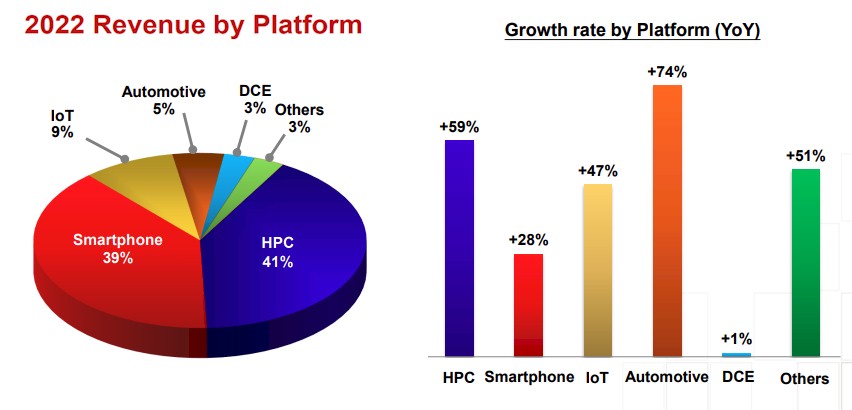

While it is unclear what 2023 holds, it was a stellar 2022 for so-called HPC chips for TSMC. (Again, this is for myriad high end chips such as server CPUs, GPUs, switch ASICs, discrete AI accelerators, FPGAs, and such.) Here is how the year was by product category:

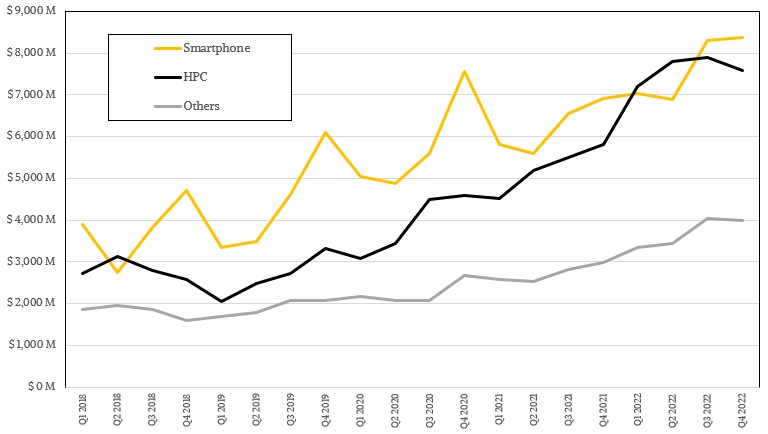

And here is the longer trend that shows HPC and smartphones against the rest of the hodge-podge:

The HPC segment increased by an incredible 59 percent and accounted for $30.47 billion in sales in 2022, or 40.1 percent of total sales. But you can see how the HPC chip segment cooled in Q3 and actually declined in Q4. It will very likely decline in Q1 and Q2 of this year as well, even with myriad CPU and GPU launches. And that is why TSMC is projecting for Q1 2023 sales across all of its segments of between $16.7 billion and $17.5 billion, which is a sequential decline of 14.7 percent at the midpoint between those two revenue projections.

According to TSMC, the 2 nanometer N2 process will start volume production in 2025 in Hsinchu (Baoshan next to TSMC’s HQ) and Taichung (Central Taiwan Science Park) in Taiwan. China was never considered a site for N2.

Dangerous transcription error. The software turned “Hsinchu” into “Chengdu”

Just for your reference, TSMC has also selected a site for the 1NM fab which is going to be located in Longtan Science Park in Taoyuan County, about 40 miles north of TSMC’s Hsinchu HQ . This location has been confirmed by the Deputy Prime Minister Shen (former Economics Minister) and the current Economics Minister Wang. TSMC has an advanced packaging fab (Advanced Backend Fab 3) in the Longtan Science Park. By the way, Apple has a microLED project (substrate-embedded) with TSMC, Epistar (Taiwan’s top LED developer) and AU Optronis in the Longtan Science Park. The micorLED project is located next to TSMC’s packaging fab. The aim is to eventually replace OLED’s that Apple currently buys from Samsung and LG.