A massive buildout of infrastructure is happening within the datacenter walls of at least several of the hyperscalers and large clouds in the world if the financial results of Arista Networks, the upstart switch maker that has been taking on Cisco Systems in the datacenter with machines based on merchant silicon for more than a decade.

We won’t know for sure how much money Microsoft, Meta Platforms, and a few other big customers spent on iron and support and software subscriptions until Arista Networks reports its year-end results in January 2023. This is when the company drills down into its segments and talks about customers who spent big on iron (or didn’t, as the case may be). The big customers for Arista Networks for many years are Microsoft and Meta Platforms, and if there is one big change with 2022, it is that the latter is spending money on 400 Gb/sec Ethernet gear after largely sitting out the 200 Gb/sec generation back in 2020 and 2021.

Let’s do some math and figure out just what a windfall this is, and what it might mean about spending across the “cloud titans” as Arista Networks calls the hyperscalers and cloud builders.

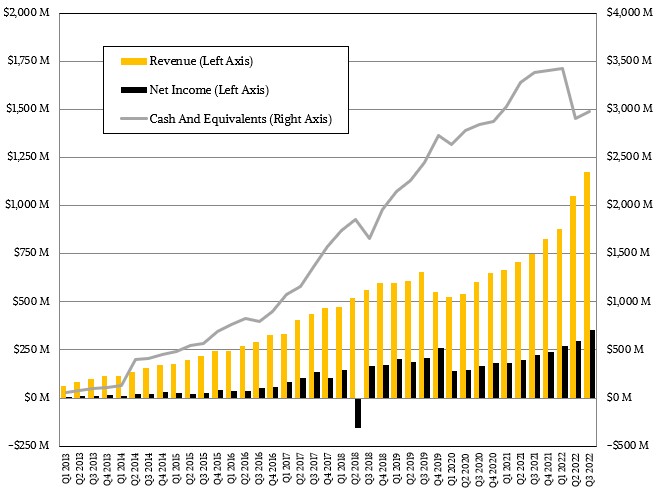

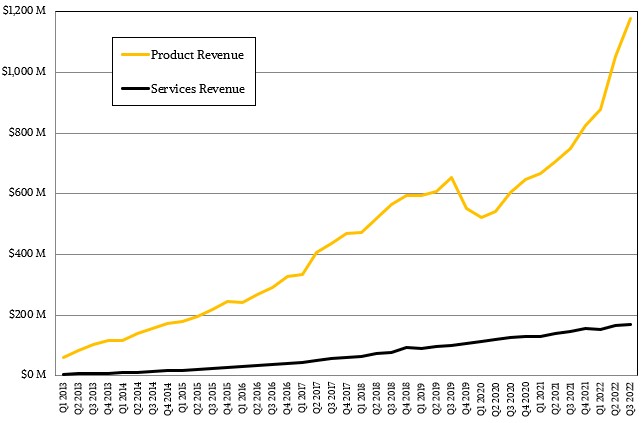

In the quarter ended in September, Arista Networks had $1.01 billion in product sales, up a stunning 67 percent year on year, with services revenues of $168.1 million, up 16.3 percent. If you do the math on what the company said, then $23.7 million of that was for software subscriptions, up 44.3 percent, and the combination of software licenses plus support services for hardware and software together accounted for $191.8 million, up 19.2 percent and driving 16.3 percent of overall revenues.

Those overall revenues rose by 57.2 percent to $1.18 billion, and net income rose almost the same, by 57.8 percent, to $354 million, accounting for 30.1 percent of revenue. This is an impressive level of growth and profitability in the cut-throat datacenter and campus networking spaces.

Like other companies that strike it rich, Arista Networks likes to reward its shareholders with some share buybacks, and that is one of the reasons why its cash hoard is only a tad below $3 billion as the quarter ended. The company has spent $740 million since this time last year on its shares against an authorization of $1 billion. About half of that came out of cash flow and half from its cash hoard.

Ita Brennan, chief financial officer at Arista Networks, said on a call with Wall Street analysts, said that when 2022 began, the company was expecting to grow revenues 30 percent this year, with a balance across the sectors and product lines and “heavily constrained by supply.” That would have been something on the order of $3.83 billion. As it turns out, Arista Networks is now guiding for a 45 percent growth rate across products and services together for 2022, or around $4.26 billion, which implies a 40 percent or so growth rate in the final quarter of the year, to around $1.18 billion.

And we can see who is spending the big bucks. Brennan went on to say that the “cloud titans” will account for 45 percent of overall revenues in 2022, which works out to $1.92 billion. In 2021, the combined spending of the cloud titans was a relatively piddling $884 million, and only grew at around 3 percent by our estimates. In this case, Microsoft was $442 million of that, we know because Arista Networks has to tell us by SEC regulation, and we estimate Meta Platforms was a mere $48 million. That was an 11.3 percent decline in spending at Arista Networks for Microsoft and a 71.1 percent decline for Meta Platforms. So that 200 Gb/sec pause was no fun. The remaining $395 million in cloud titan money from 2022 came from other buyers, but none of them rose to the 10 percent of revenue level that requires reporting by the SEC.

We strongly suspect that Meta Platforms will be a big part of 2022’s cloud titan revenue, as will Microsoft, when the numbers come out next January. And the growth factor of 2.2X for these cloud titans is amazing, but also expected given that 200 Gb/sec was a stepping stone to 400 Gb/sec.

Now here is the neat bit. According to Andy Bechtolsheim, co-founder and chief products officer at Arista Networks, the network represents on the order of 10 percent of the cost of a cluster at the cloud titans. That means Arista Networks is involved in somewhere close to $20 billion in datacenter infrastructure among the cloud titans this year.

“Demand from our enterprise and provider businesses has also been strong, exceeding our original expectations from a demand perspective,” Brennan added on the call. “But with revenue somewhat constrained by supply.” Jayshree Ullal, chief executive officer at the company, added that that it expected to hit its goal of hitting $400 million in campus switch sales in 2022, but given the supply constraints, it was not sure if it will make it.

Ullal, like many other IT suppliers, does not want the company she runs to be treated like a leading indicator for the economy or the overall IT sector, but truth be told, Arista Networks is absolutely a bellwether for certain parts of the IT sector that we care about – like large enterprises, hyperscalers, and cloud builders. And this is what she had to say about that:

“Look, I don’t think Arista is a bellwether for macro. So we will let the pundits and economists speak about that. But I think it is fair to say that datacenter spend has been very strong and we are confident of our near-term strength, both in cloud titans and enterprise and campus. If there is a place that we see some softening at all geographically, I would point to Europe. They have had the effects of the pandemic, the energy crisis, the war, and Brexit – it’s just a whole lot of things going on there. But our numbers are small. And even there, I would say it’s more than enough to execute better. So overall, macro is not yet an issue for us. We will keep a vigilant eye on it, but so far, so good.”

And then she elaborated in an interesting way:

“Unlike server or storage, networking is a very, very strategic spend. There is a long qualification cycle that goes into proof-of-concept labs and is intense testing for scale. we are all struggling with lead times. So switching windows doesn’t give you any particular advantage. And if you are looking for best-of-breed and best operational advantages, our customers would prefer to wait for us. So of course, we don’t want to test their patience. We’re going to do everything we can to execute.”

The ramp of 400 Gb/sec Ethernet, both inside the datacenters and across datacenters and regions at the hyperscalers and cloud builders, is a big driver of business right now, and even though the majority of large enterprises are still using dusty and rusty 10 Gb/sec and 40 Gb/sec switches, Ullal said that Arista Networks is seeing some enterprise customers move to a combination of 100 Gb/sec and 400 Gb/sec in their networks. Back in 2020, Arista Networks had 70 customers, and then quadrupled it to 300 customers in 2021 and will probably double it to more than 600 customers. These are the flagship uses cases, but a lot of revenue is still going to come from 100 Gb/sec and even 200 Gb/sec links. The share of ports sold running at 400 Gb/sec is somewhere around 5 percent of ports for the company in 2022 and maybe 10 percent of ports in 2023, according to Ullal.

These transitions all take time. And sometimes, a lot longer than expected, as happened with the initial run at 100 Gb/sec networking, which was too hot and too expensive, and with 400 Gb/sec, which many were willing to wait for and skip the huge hassle of investment in 200 Gb/sec two years ago.

Be the first to comment