Imagine, if you will, that AMD could make as many Epyc CPUs and Instinct GPU accelerators as it wanted at a reasonable yield and cost. How much larger would its datacenter business already be, setting aside the $49 billion acquisition of FPGA maker Xilinx, completed earlier this year, and the just-announced $1.9 billion acquisition of DPU maker Pensando – both of which add other even more potential datacenter revenues and profits.

It is a very interesting thought experiment, a bit like removing the friction from the table of a simulated billiards table. Eventually, all of the balls go in after one break, if you wait long enough.

But there is friction out there in the semiconductor market. A lot of it, having to do with getting the substrates necessary to etch chips and with getting the wafers on which to do the etching and the place in line at the foundry – in this case Taiwan Semiconductor Manufacturing Co, which is the most popular advanced chip maker on the planet – to do the etching. While AMD has done a great deal to be able to increase its supply of “Milan” Epyc 7003 processors in the past year and is no doubt being more aggressive in its planning for the future 96-core “Genoa” Epyc 7004s coming later this year and the 128-core “Bergamo” variants of the Zen 4 designs due in the first half of 2023 aimed at hyperscalers and cloud builders, we think that given the relatively weak position that Intel has with its current “Ice Lake” and future “Sapphire Rapids” Xeon SPs, AMD could do a lot better than even the very impressive showing it has had in the datacenter.

Considering where AMD was at when it made the commitment to re-enter the datacenter back in 2015 – basically no revenue and no product roadmap – the transformation of AMD back into a player in the datacenter is nothing short of amazing. It is also a testament to the value and desire for competition, and there were many organizations that gave AMD encouragement and the prospect of revenues if it came back into the business it all but abandoned in 2009, setting Intel on a decade-long path of hegemony in datacenter compute.

Those days are long over, thanks in part to AMD’s rearchitecting of its business and its compute engines, but also in part thanks to both manufacturing process and server processor design issues (which are unavoidably intertwined, of course) at Intel, which is still seeing very good sales in the datacenter because AMD never planned for Intel to have so much trouble with its 10 nanometer and 7 nanometer process nodes. And by the time AMD might have felt more comfortable making a bigger bet on itself, the coronavirus pandemic struck and tightened up semiconductor manufacturing at the same time demand exploded.

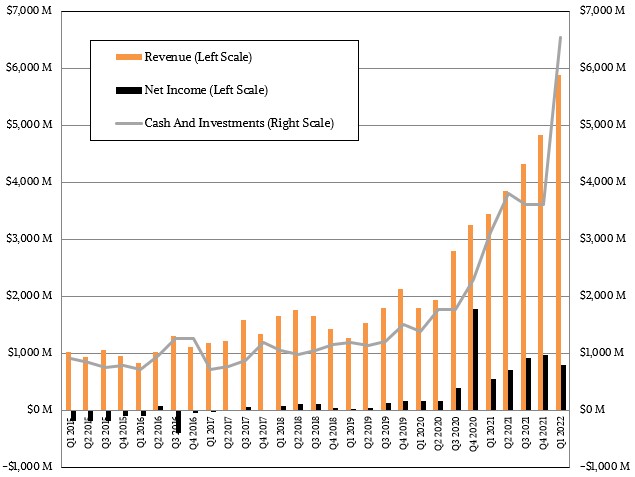

Still, what a ride AMD is on. In the first quarter of 2022, when the Xilinx deal closed, AMD’s revenues absent Xilinx, rose by 54.7 percent to $5.33 billion, and including six weeks of Xilinx revenues, overall sales at AMD rose by 70.9 percent to $5.89 billion. Net income for the quarter was up only 41.6 percent to $786 million as the company absorbed some of the costs if the Xilinx acquisition and boosted sales, research, and development costs.

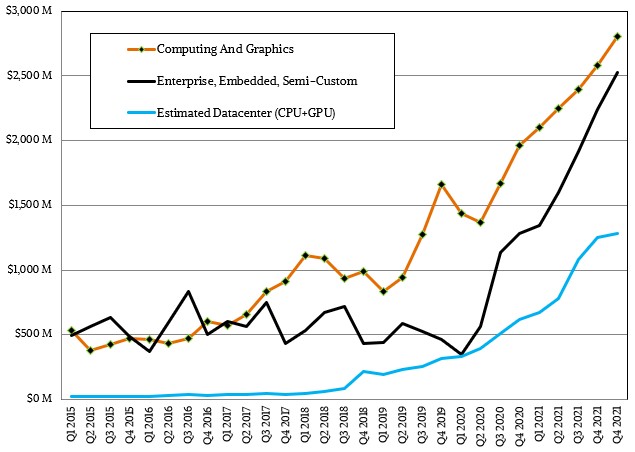

Importantly, AMD’s datacenter revenues have doubled, give or take a few percentage points, for the seventh quarter in a row. According to our model, datacenter revenues – meaning Epyc CPUs and Instinct GPUs but not including any contributions from Xilinx – rose by 92.2 percent to $1.29 billion, which represents a 2.4 percent sequential growth rate from a very good Q4 2021. Epyc CPU sales were up by 102 percent to $1.22 billion and Instinct GPU sales were up 5 percent at $70 million. We reckon that six weeks of Xilinx datacenter revenues – about $52 million – in the March quarter were added onto AMD’s books post deal close, and that makes AMD’s overall datacenter revenues $1.34 billion, or 22.7 percent of total revenues for the company.

It is usually a good sign when a first quarter is up sequentially from the prior fourth quarter for any IT supplier, because there is almost always a Q1 sequential dip.

But the obvious question is: Can this datacenter business at AMD keep doubling? Even in the short term this is a good question, and it is an even better question as Intel is still trying to get its CPU act together and get its first discrete GPU for compute in the field and as Nvidia has just announced its next generation GPU (shipping in the third quarter) and is revving up its first server CPU (due next year). Oh, and Microsoft, Tencent, Baidu, Alibaba, Oracle and (probably soon) Google are deploying Arm server chips from Ampere Computing in their server fleets and Amazon Web Services is ramping up usage of its homegrown Graviton Arm server chips.

“I think the datacenter business, particularly the server CPU business, continues to be very strong for us,” Lisa Su, AMD’s president and chief executive officer, said on the call with Wall Street. “I am not going to proclaim for certain it will double every quarter. I can say that we expect to grow very strongly over the next few quarters, and we are continuing to bring on additional supply to do that. The demand is there and it really is about continuing to work with our customers on that. But I think our confidence level in datacenter growth is very high.”

One reason why AMD is feeling so confident is that its growth with the Epyc server chips is not just among the hyperscalers and cloud builders, but now enterprise customers, who largely buy through OEMs, are buying at the same increasing pace. But like other upstart IT suppliers, AMD is very tightly coupled with its biggest customers and has a planning horizon that extends through all of 2022 and now into 2023. This is the upside of the semiconductor supply chain being tight. Hyperscalers and cloud builders no longer keep suppliers like AMD in the dark. They can’t if they hope to get the components that they need to build out their infrastructure.

This is why AMD is now guiding its core business to grow around 35 percent in 2022, up from a 31 percent estimate a quarter ago, and that with Xilinx in the mix and soon Pensando, the guidance for all of 2022 is now to have 60 percent revenue growth. That will put AMD at around $26.3 billion in sales for the year, quite a contrast to the $4 billion in sales the company posted in 2015 when it decided to come back into the datacenter racket.

And just to give you a sense of how much that datacenter business has grown, AMD had about $100 million in datacenter CPU and GPU sales back in 2015, and did $3.78 billion in 2021 and, even at only 60 percent growth, it will break through $6 billion and at slightly less than doubling (which is more likely given how Genoa will stack up against Sapphire Rapids) it will probably post something on the order of $7.2 billion in core datacenter revenues, and then add maybe $400 million to $500 million from Xilinx for its FPGA datacenter business on top of that.

AMD’s success is due to a combination of consistently delivering reasonably competitive CPU / GPU while riding the TSMC process train and an unbelievable number of Intel technology and business failures that led a vast number of customers to actually deploy AMD products instead of using AMD as an arbitrage vehicle. Props go to their CEO for bringing strong organizational discipline and business savvy; she is one of the best in the industry. As for AMD’s data center strategy, props go to their CEO who finally got their technology / business leads (hubris isn’t unique to Intel) to realize that their more to the data center than just CPU / GPU which should have been done years earlier, and IMO, only came about as they saw Nvidia accelerate its acquisition and organic technology efforts enabling them to take market and margin share from competitors and partners alike. Hopefully, they don’t rest on their laurels and will continue to expand their portfolio while adhering to open standards where appropriate as no intelligent customer will ever interlock their future / supply chains with any single vendor again.

Excellent analysis which nicely rounds out the article!

Wow, only $70 million for Instinct GPU sales? I didn’t realize how small that segment was… I would have expected it to be quite a bit more since their supercomputer deals are using the MI250… Maybe that’s a typo?

Here’s the trend I have in my model, and I think the cost of at least some of the Aldebaran GPUs is in here. Starting with Q4 2020, you see:

Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022

$72 M $67 M $80 M $164 M $148 M $70 M

I think they have to wait for acceptance to book all of the revenue.