When this is all said and done, Intel will deserve some kind of award for keeping its 14 nanometer processes moving along enough as it gets its 10 nanometer and 7 nanometer processes knocked together to still, somehow, manage to retain dominant market share in the server space.

Or, maybe Intel just got lucky that AMD’s supply can’t even come close to meeting the potential demand it might otherwise have if there were no limits on the fab capacity at Taiwan Semiconductor Manufacturing Co, which etches the core complexes in its Epyc server chips. (Globalfoundries, the spinout of AMD’s own foundry mashed up with IBM Microelectronics and Chartered Semiconductor, still makes the memory and I/O hub portions of the “Rome” Epyc 7002 and “Milan” Epyc 7003 processors from AMD.)

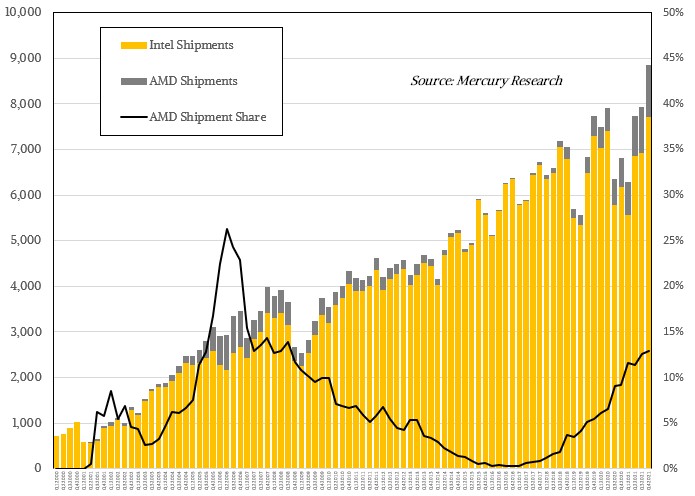

This time last year, when we took a look at how AMD’s share of processor shipments and revenues had grown since its re-entry into the server space back in 2017, the company had just broke through the 10 percent shipment barrier and looked to be on a Opteron-class fast path to 20 percent or maybe event 25 percent. And then the 10 nanometer “Ice Lake” Xeon SPs were launched, and say what you will about how the Rome chips beat them and the Milan chips hammer them, you go to the datacenter with the server chip that you have, paraphrasing former Secretary of State Donald Rumsfeld, who when under fire for the sorry state of the US Army as the Gulf War started quipped with a certain amount of pique that “you go to war with the army that you have.”

If you look at the data from Mercury Research, which does a fabulous job of watching the competition between AMD and Intel, you will see that AMD has a big jump in server CPU shipment share and then it levels off a bit or even declines some and then once it gets its footing, it blasts up a few points to a new level and repeats this entallening sawtooth shape again and again.

And so, as the fourth quarter came to a close, according to Mercury Research, AMD shipped 1.13 million server CPUs, an increase of 82.9 percent over the year ago period, which is great. But the overall market for server CPUs – pushed into the channel, not consumed by the customers on the other side of the channel – rose by 29.9 percent to 8.85 million units. And thus, Intel was still able to grow at almost the same pace of the market at large, rising 24.6 percent to 7.71 million units. And thus, Intel was able to have a record quarter for server CPU shipments, which drove server revenues to new highs as well despite a 5 percent decline in sales to hyperscalers and cloud builders and thanks in large part to a return to spending by enterprises and telco and communications service providers. We suspect that there has been a little channel stuffing on the part of Intel, and a whole lot of component bundling (which is price cutting that doesn’t affect the Data Center Group revenue line but does cut into the revenues and profits of the Data Center Group adjacencies such as switch ASICs, network interface cards, silicon photonics (mostly Ethernet optical transceivers), and Optane storage. Such pricing tactics will all come home to roost – unless server demand keeps on growing and Intel does a good job with the forthcoming 10 nanometer “Sapphire Rapids” Xeon SPs due by the second quarter.

To stick with the war metaphor, Intel’s 14 nanometer infantry with some 10 nanometer tanks was able to hold the line against AMD’s tactical assault teams and sharpshooters. And there are some 10 nanometer gunships on their way as AMD brings a new class of weapons to bear with the “Genoa” Epyc 7004s. If AMD had more capacity, it would be eating more share. There is no question about that. But we think that both Intel and AMD are happy to manage capacity close enough to demand to be able to still have shortages that cause prices to hold or even increase, particularly with high end SKUs in their CPU lines. And they will stretch out product launches to the breaking point, and can always let the hyperscalers and cloud builders have these parts on the sly and charge a premium for that, too.

In other words, server buyers, none of you are in the driver’s seat. TSMC and Intel Foundry Services are, and they are calling the tune on pricing and setting the pace on shipments, and if you need a server, you are going to the datacenter with the CPUs that you have.

Anyway, back to statistics. When you do the math, AMD had 12.9 percent shipment share in the fourth quarter of 2021, according to Mercury Research, and that is barely three-tenths of a point higher than the share it had in Q3 and mimicking the same tepid growth in share it had in the prior year at the same time.

It is hard to say what will happen as Genoa Epyc 7004s hit the market and possibly more revenue is recognized for the “Trento” custom Epyc processors used in the “Frontier” supercomputer at Oak Ridge National Laboratory (we think a lot of this was done in Q2, Q3, and Q4 of 2021, but AMD has not said how this works).

What we will observe is that AMD’s revenue share has been outpacing its shipment share since Q2 2021, which is when that revenue recognition for Frontier might have started. And given that the major supercomputing centers usually pay less than half of list price for CPUs and GPUs, based on estimates we have done, then this revenue recognition would actually have hurt AMD’s revenue share. And so if AMD’s share of the X86 server chip market revenues is higher that means Intel’s average revenue per chip is trending up slow than AMD’s is trending up. (Both are trending up as customers increasingly buy up the stack.) We will be watching this revenue expansion rate carefully. In the fourth quarter, for instance, AMD captured 14.4 percent share of the $7.48 billion in X86 server CPU sales, and it had the same share of the $6.65 billion in X86 server CPU sales in Q3 2021, according to Mercury Research.

It is even harder to say what will happen out towards the end of 2022 and through 2023 and into 2024. By that time, the server market could be consuming somewhere close to 10 million X86 server CPUs a quarter, and maybe even 500,000 or more Arm server CPUs (why not?), with the X86 servers generating somewhere close to $9 billion in revenues per quarter. We have a long way to go to get to that point, but when it is done, if current trends persist, it is not hard to see AMD having somewhere north of 20 percent shipment share and close to 25 percent revenue share of the X86 market, which is going to continue to grow even if at a much slower pace than it is doing now.

This will be fun to watch unfold, quarter by quarter, shot by shot.

Camp Marketing has AMD commercial shipments for the year higher than Mercury Research on channel data on 10-Q/K financial reconciliation.

My commercial estimate includes Epyc and Threadripper. Epyc in quarter volume is not regular but sporadic on what the analyst believes are opportunistic production windows in relation wafer starts and AMD full line production category volume – start’s tradeoff. TSMC appears agile when it comes to production / tooling change.

2021 = range 8,320,645 to 9,620,695 units dependent q2 volume roll over into q3;

Q1 = 1,099,950

Q2 = 4,331,103 which is Rome run end production into inventory

Q3 = 1,189,776 which could be roll over from Q2

Q4 = 2,999,867

30% are Threadripper

2020 = range 4,168,967 to 4,560,973 units dependent q3 volume roll over into q4;

Q1 = 449,332

Q2 = 846,604

Q3 = 2,404,558 where some of this volume may roll over into Q4

Q4 = 1,567,108

15.2% are Threadripper

2019 = 5,714,393 of which 76.1% is Threadripper

Naples run end enters q2 2019

2018 = 6,795,562 of which 83.8% is Threadripper

For channel share AMD Milan commercial in relation Intel Ice Lake commercial, I have AMD at 28.45% for channel market share over the prior two quarters [q3-q4] and production volume share, prior two quarters, on AMD and Intel financials on channel price data at 17.09%

AMD 2021 all up produced 119,108,089 units and holds 29.06% overall x86 market share.

Mike Bruzzone, Camp Marketing

I like ur work, but after a good job pointing to the harsh realities & temporary sellers market Intel faces, u draw benign conclusions re intel’s future.

For now they can achieve selective good numbers via a mix of a lot of old tech w/ a little new tech & disguise the weakening margin hits via bundles for now, but clearly it is intel which is underspending on new tech & TSMC that is way out spending them.

More cores w/decent power & latency will always win in servers. Sub par chips are uneconomic at any price.

w/o a true response to Infinity Fabric for the foreseeable future. “mesh”/”tiles”/”chiplets” … are just buzzwords w/o the ~seamless scalability of Fabric

Intel may be merely waiting for a big bolus of public money, aka the CHIPS Act, to get deposited into it’s bank account. Why spend its own money when it can spend the taxpayers’ instead?

lol@”big bolus” — I’m picturing a big green IV bag full o’ cash, drip drip

I hear you but at some point they can’t wait, they need to move. I don’t know if Congress can move quickly enough right now on the CHIPS Act and I don’t know whether Intel is the primary beneficiary or whether there’s some incentive to spread the money around to others who might build fabs here in the US, there’s always lots of variables. I think they can go into their own pocket for earnest money and to get things rolling, and CHIPS Act, when it shows up, is more fuel for the fire.