All good parties come to an end, and the one that Intel has enjoyed for an unbelievable dozen years, starting with the rollout of the “Nehalem” Xeon E5500 processors back in March 2009, is over. Find the Advil, grab a glass of water, and try not to drop all the pills on the floor.

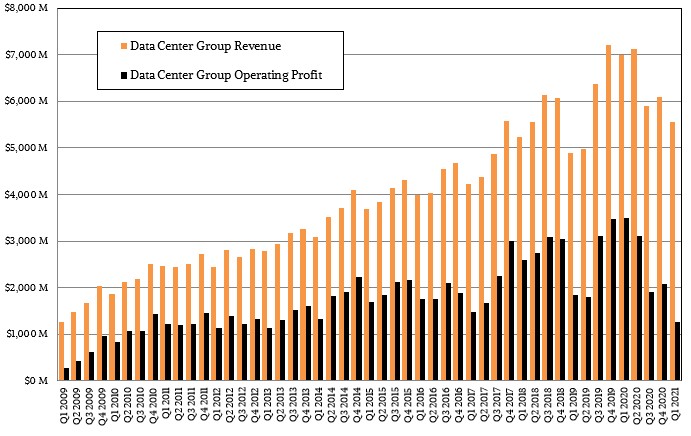

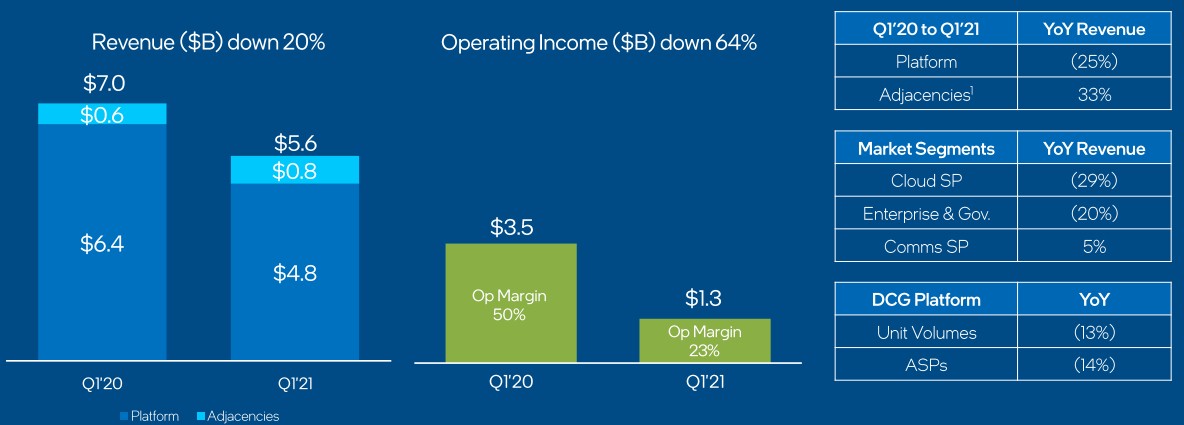

Nothing demonstrates this more than Intel’s financial results for the first quarter of 2021, where its Data Center Group stomached an overall decline of 20.4 percent to $5.56 billion, and the core platform sales – meaning processors and chipsets and motherboards – fell by 23 percent to $4.81 billion. As we have been saying, Intel has been able to mask some of the effects of the competition that AMD has brought to bear by bundling together different components, both inside of Data Center Group and from other Intel groups, to keep the revenue coming in. But the combination of a number of factors has made even this strategy fall flat. We think Intel is supply constrained with its 10 nanometer “Ice Lake” Xeon SP processors, launched earlier this month, and no one is willing to take prior generation “Cascade Lake” CPUs at anything even close to list price, and so, inevitably Intel’s Data Center Group revenues declined and – here is the important bit – its operating profits declined over three times faster, falling a stunning 63.5 percent to $1.27 billion.

Wile E Coyote finally looked down. . . . as we always knew would happen. And the reason is simple. No business that is throwing off 50 percent operating margins will remain free of competition. No market will allow that. Many will enter the field, a few will succeed, and then there is a price war followed by a sustained technology campaign.

In fact, if the competition had been stronger, or if Intel had been only a CPU player, Data Center Group margins would have taken this hit a lot earlier. As it is, operating profits are back to absolute dollar levels that Intel was stuck at between 2011 and 2013. And before this year is out, even if revenues stabilize, Data Center Group could see profits hit even harder as competition heats up and costs for 7 nanometer development go up.

It is a pity that Intel didn’t do something more useful with all that excess Data Center Group profit for the past decade – more useful than blowing tens of billions of dollars on share buybacks, at least. Perhaps it would have already built two foundries and already established its Intel Foundry Services business. Who can say?

But don’t get the wrong idea, because it is easier to take things too far. Just like AMD’s rise in the datacenter has taken longer than expected – certainly longer than the Opteron ramp back in the 2000s – and is more muted than expected, Intel’s decline is a temporary setback. The company is regrouping, and it will, thanks to a shortage of fab capacity in the world, become a merchant foundry, and for the reasons we said a few weeks ago: It has no choice. The only way to run a foundry is to milk older processes for everything they are worth. Intel can no longer afford to throw away fabs because the old ones can pay for the new ones and not every chip – indeed most chips – do not need the most advanced processes that a CPU, a GPU, or an FPGA requires to run datacenter workloads. Just ask Taiwan Semiconductor Manufacturing Corp.

This is not a protracted fight for the CPU in the datacenter, and the gloves are off and Intel has to fight to stay in the ring now. And AMD has earned its way back into the ring to fight like hell, and will. The Arm collective is holding a metal chair and is climbing through the ropes. . . .

Back to Intel’s numbers. While Intel said that its Data Center Group numbers were above its expectations, they still are pretty awful and set a new baseline, we think. This isn’t just about the hyperscalers and cloud builders having “inventory digestion,” as George Davis, Intel’s chief financial officer put it. This is about Intel having heartburn. Operating income for Data Center Group was impacted by the 10 nanometer ramp and investments in the Xeon SP server processor roadmap – meaning costs for the future 10 nanometer “Sapphire Rapids” chips that will sample at the end of this year and ramp through the first half of 2022 and the 7 nanometer “Granite Rapids” chips that are supposed to follow a year later. But some of that hit to revenue and profit is just plain competition, and more than Intel wants to admit to Wall Street. In fact, all Davis would admit to is that the 14 percent decline in Data Center Group average selling prices was due to product mix and factory startup costs for 10 nanometer production and 7 nanometer preproduction.

Here is how Pat Gelsinger, Intel’s prodigal chief executive officer, sees the situation. “It’s about building leadership products. Ice Lake is a great product and we are seeing a strong ramp for it. As the products get better, ASPs will get better – and then we are going to be very aggressive in terms of market share in this area. So we feel like we are now very much on the front foot again in this business and we are starting to see the market respond that way. And with some of the things that we have talked about with Ice Lake in particular and our Sapphire Rapids program following up, we are on a good competitive dynamic and we are leaning into this area of our business and we are seeing great response from our customers.” Gelsinger added that Intel is going to “fight for every socket in the market.”

There are going to be some bruised eye sockets, for sure. And maybe some bruised egos, too, as the hyperscalers and cloud builders just decide to build more and more of their own CPUs (as AWS is doing and as Microsoft is expected to be doing), or as Ampere Computing, Fujitsu, and now Nvidia get some traction with their Arm server CPUs. Gelsinger said that the volumes of homegrown CPUs at the hyperscalers and cloud builders “are fairly modest overall” and even if more of them do it, Intel Foundry Services can pick up some revenue etching these chips, too. This is inherently lower margin, we think, but maybe not terribly so.

Whatever is happening, Davis said that all three segments where Intel plays will see growth – enterprise and government, cloud, and communications service providers – in the second quarter of this year, but that cloud buys (what we call hyperscalers and cloud builders) would be “the standout grower” in Q2. It will be interesting to see if any of the hyperscalers and cloud builders take Intel Foundry Services up on the offer of building custom X86 server processors for their datacenters, something that Gelsinger reiterated was on the table.

In the meantime, the Ice Lake Xeon SP and its relatively short-lived “Whitley” platform will have its short ride, and all eyes are now turning to Sapphire Rapids and its “Eagle Stream” platform, which will also support the “Granite Rapids” Xeon SPs, thus cutting server OEMs and ODMs a break on having to redesign their motherboards and systems. Those who can wait for Sapphire Rapids and Eagle Stream, which will sport DDR5 memory, PCI-Express 5.0 peripherals and the CXL overlay, and fourth generation “Donahue Pass” Optane PMEM.

One last thing. Gelsinger also said there was an installed base of over 100 million servers in the world, which seems a bit high. We are going to have a think on that.

” no one is willing to take prior generation “Cascade Lake” CPUs”

FB is reportedly taking Cooper Lake CPUs for the bfloat16.

The new Ice Lake is slower than previous Cascade Lake. Intel is going backward.

“Intel can no longer afford to throw away fabs …”

Do you think Intel buys all new DUV equipment when moving from 14nm to 10nm?