The hyperscalers and cloud builders can be split into two camps, but a third one might be emerging.

There are those who do not buy routers or switches from Cisco Systems, one of the early innovators in routing in the late 1980s – when a router was a funky kind of server – that expanded through many acquisitions into switching in the datacenter and on the campus. There are those who do buy such gear. And there are those who are reconsidering buying Cisco Silicon or even complete gear in the wake of the Silicon One router and switch chip launches in December 2019 and October 2020, respectively.

Cisco was the safe bet in networking in the dot-com boom, much as Oracle databases and Sun Microsystems servers for running those databases as well as web and application servers were the safe bet for serving in that time. No safe bet stays that way forever, and at exactly the same time just ahead of the Great Recession in 2008 that Cisco was preparing to move into converged server-switching platforms with its “California” Unified Computing System (UCS) platform, Broadcom ramped up its “Trident” merchant silicon for whitebox switching and bought Dune Networks for its “Jericho” line of deep buffer, extensible, switch/router hybrid chips that was the foundation for whitebox routing. Cisco made big gains in serving but lost share in switching and routing – and among the largest IT buyers in the world. Which hurts.

The success of Trident and Jericho, and Trident’s offshoot for hyperscalers and cloud builders, the “Tomahawk” switch chips which have a smaller feature set and a cheaper price, backed Cisco into a corner. At first, Cisco adopted switch ASICs from Broadcom, Innovium, and Barefoot Networks (now part of Intel) as well as developing its own “Monticello” switch ASICs as well as custom router chips like this one. The point was these all could run Cisco’s legacy Internetworking Operating System (IOS) or its more recent NX-OS for its Nexus gear. The fun bit now is that not only will Silicon One switch and router ASICs support IOS or NX-OS as necessary, but it looks like they will soon support the DNOS router stack from DriveNets and very likely (we are guessing) the ArcOS switching and routing stack from Arrcus. Others may follow – IP Fusion, which is commercializing the Vyatta-DANOS stack forged by AT&T, comes to mind. So, in theory, companies might be running IOS or NX-OS on various merchant silicon or running merchant NOSes on Cisco Silicon One chippery.

This has been a hard-won battle for choice, and the fight is not yet over. But the tide of the war against the last bastion of proprietary control (notice we did not say anything about proprietary software or open source, which is not the point) in the datacenter.

That ability to choose is a decade and a half in the making and it is only about customer choice, not vendor choice, and it is why we all should love intense competition in any market – but particularly with datacenter networking where vendors have built citadels with high walls and deep moats against competitors. Open source is a weapon here, but it is not the only one, and it may not be the best one. Economics trumps code, and we have the hyperscalers and cloud builders to thank for prying the covers off network gear and opening them up to competition at many levels, even if they closely guard their network stacks – Microsoft and Facebook somewhat excepted with their respective SONiC/SAI and FBOSS efforts. This multi-layered competition is what transformed the server business from proprietary stacks wrapped up as appliances with very high costs to cheap layers of CPUs, systems, and operating systems that allow for choice within a lot of these layers. And this competitive force will transform the networking business as surely as today is March 354th, 2020.

It is with all of this in mind that we ponder the financial results just turned in by Cisco and await the numbers out of its arch-rival in datacenter switching, Arista Networks, later this week and think about the preliminary results from routing arch-rival Juniper Networks, which were revealed a few weeks ago. (We will cover these separately.)

Sometimes, you can only see something – truly see something – when you haven’t looked at it for a while, and we will be honest and say it has been a while since we dove into Cisco’s financials. Despite all of the churn and disruption in datacenter and campus networking, despite the change in chief executive officer from John Chambers to Chuck Robbins, and despite the sometimes not helpful tendencies of companies that have near monopolies in their markets – think IBM, Microsoft, and Intel in their turn – Cisco has been amazingly stable.

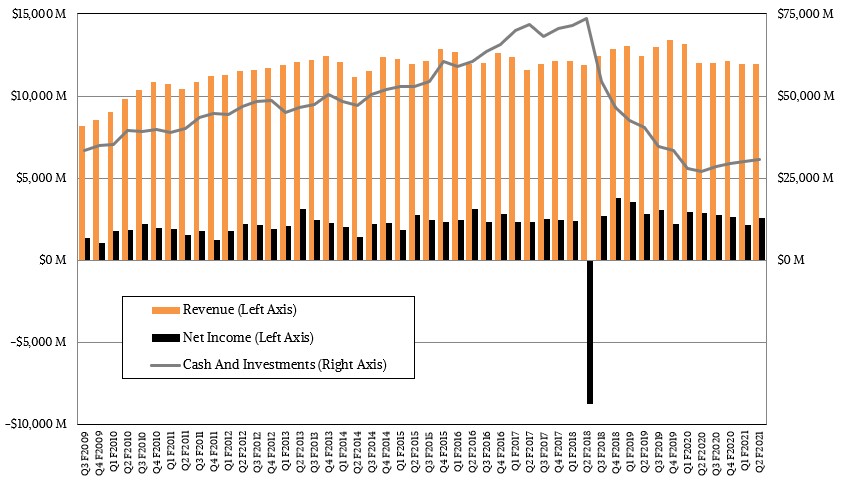

It is funny that the upstarts of days gone by are the steady freddies of today, but this has certainly happened to Cisco. And therefore it was no surprise to us that Cisco repatriated and paid taxes on its huge overseas cash hoard in fiscal 2018 – that is that big loss you see in fiscal Q2 in the chart above when it had close to $75 billion in the bank – and then bought a tremendous amount of shares back from Wall Street. Since the Great Recession, the share buyback tab has been pretty heavy at a net $76.1 billion (Cisco also distributes shares from time to time), but from the summer of 2017, after Chuck Robbins had been at the helm of the networking giant for two years, until the beginning of the Great Infection this time last year, the spending was much deeper – a net $42.1 billion over nearly three years.

Share buybacks are what companies do when they can’t think of anything else better to do. No new technologies that require huge investments, no big acquisitions that make sense at the prevailing (and usually high) prices that Wall Street or the private equity offices of the world set for things. So you buy up your own shares with the electricity that is net income and store it in the capacitor that is market capitalization – and make yourself and your investors rich. And if you do it right – as Cisco has done, by this logic – you do it before your competition and/or the next recession hammers you. And if you need to buy something, you can always use stock, as Nvidia is demonstrating with its attempted $40 billion acquisition of Arm Holdings from Softbank.

And now, after having blown all of that cash, Cisco has been steadily generating more cash and has $30.6 billion in the bank and its market capitalization is driving towards $200 billion again. (A far cry from the $500 billion market capitalization Cisco had during the go-go dot-com days, mind you. But that is what happens when you go from a unicorn to a draft horse. (There is something to be said for draft horses, and we prefer the Belgian sort instead of the flashy Clydesdales.)

In the second quarter of fiscal 2021 ended in January, Cisco’s revenues dropped by four-tenths of a percent to $11.96 billion, and net income fell by 11.6 percent to $2.55 billion. Compared to the average quarter for Cisco, which as you can see from the chart above does not vary as much as is the case with many established IT suppliers, this was not outside of the ordinary.

In the most recent period, product sales were off 1.1 percent to $8.57 billion and services sales rose by 1.6 percent to $3.39 billion, a testament to the fact that people want to keep their networking hardware and software on maintenance, even in a recession. As you can see, product sales took a hit in calendar 2020, but nothing out of the realm of ordinary and certainly did not fall as far as happened (in absolute dollars at least) as happened during the Great Recession back in 2008 and 2009.

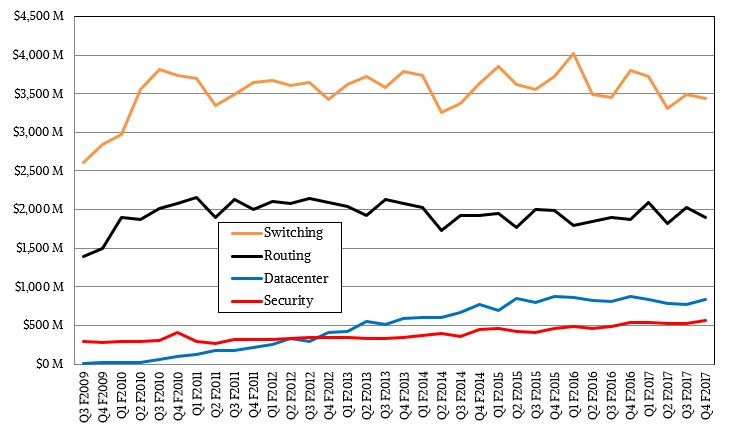

A year after Robbins took over from Chambers as CEO, Cisco reclassified its financials in such a way as to obscure its revenues from its distinct switching, routing, and server businesses, which is a shame really. But just as a foundation, let’s give you the data that we do have running from the Great Recession forward to the summer of 2017, which was the fourth quarter of fiscal 2017. Take a look:

It would be hard to find a tech business – or any business in any sector of the economy – more steady than this. That UCS converged server platform took off in the mouth of that Great Recession, upsetting all of the server OEMs and making them buy their way into networking and rearchitect their systems for network convergence, causing a huge amount of disruption – to both Cisco’s advantage and its disadvantage. It is hard to say if it has been a net gain for Cisco, but we think the company knew the boom was coming from merchant silicon in both switching and routing and it wanted to change the terms of engagement in the datacenter, particularly among enterprise and commercial customers where the server OEMs were not innovating enough. Cisco’s security business kept growing, ever so slowly, but datacenter, switching, and routing had at least through the end of fiscal 2017 ended in October of that calendar year stabilized.

Here is how Cisco talks about itself now, which is not nearly as useful:

We were able to backcast this data to Q1 F2017 when it was first released in Q1 F2018 because there are percent changes for the initial data.

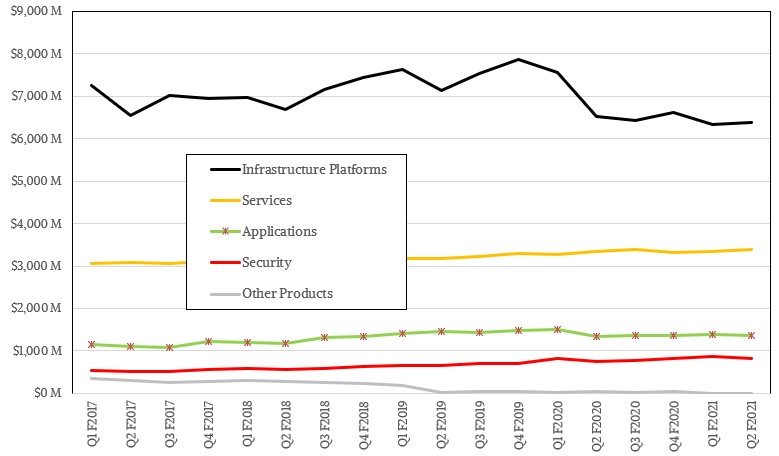

Infrastructure platforms includes switches, routers, servers, and other kinds of gear, including that for edge and IoT applications that are not, strictly speaking, datacenter products. This aggregate business has tended to hover at around $7 billion, give or take, and clearly in the past year during the Great Infection it has done some giving, which is not at all surprising. The services category is the same data, and now applications, which are being sold separately as perpetual and SaaS licensed products, has been pulled out. The security revenue stream is essentially the same.

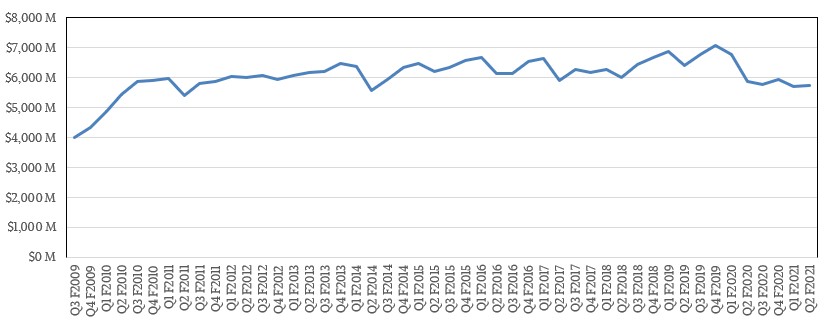

We like to see longer trends, and so we took the old characterization and the new characterization of Cisco’s business and tried to create a unified server, switch, router revenue stream from both sets of data, culling out some of the infrastructure sales in the new categorization that are not related to the datacenter. Here is our best shot of how this business looks:

It is a remarkably steady business in the aggregate, and the pandemic has hit Cisco only a little harder than competition did three years ago. When we get a bit more time, and talk to some of our friends on Wall Street, we will try to pull switching and routing and datacenter back out of the recent Cisco financials.

In the meantime, let’s drill down in Q2 of fiscal 2021 ended in January. Infrastructure platform sales were off 2.1 percent to $6.39 billion, and Scott Herren, Cisco’s new chief financial officer, said on a call with Wall Street analysts that the infrastructure contraction was “driven primarily by servers,” as we all know well, enterprise customers know how to stretch their capacity in a recessional pinch, so no surprises there. Cisco does not sell servers to hyperscalers and cloud builders, who have their own disaggregated platforms and would not use a converged platform that tightly couples one vendor’s networking to one vendor’s serving in any event.

Herren added that while Cisco’s switching revenues were flat overall, Cisco “saw solid growth in datacenter switching with strong growth of the Nexus 9000.” The Nexus 9000 series are fixed port and modular switches based on the company’s Cloud Scale ASICs as well as Broadcom’s Jericho2 ASICs, depending on the models and needed features.

Former CEO Chambers said many years ago that Cisco had a plan to get back into what it calls the “web-scale” customers, which is a much broader term than the ones we use – hyperscalers and cloud builders – and includes communications service providers and telcos as well. On the call, Robbins said that getting back into the good graces of these customers was a marathon, not a sprint, with an effort that started more than five years ago but which, Robbins added, has been paying off in the last five quarters since the Silicon One launch. The growth rates for “webscaler” adoption have been all over the map in terms of lumpiness, but all up and to the right, ranging from 17 percent to 74 percent growth in the prior four quarters. But in the quarter ended in January 2021, sales to the webscalers, which is a subset of the service provider business segment at Cisco, had “triple digit growth” year on year. The Cisco 8000 series routers, based on the Silicon One chips, were singled out as doing well and the 400 Gb/sec Ethernet they implement is being well received. Sometimes Cisco is selling chips, sometimes whole routers. And putting some more numbers on it, Robbins added that webscaler sales accounted for an average of 21 percent of total service provider sales in the prior four quarters, and hit 25 percent in the January 2021 quarter.

“Again, this business – much like the service provider business that we’ve talked about over the years –will be big deal driven, big customer driven. So it will have a tendency to be lumpy,” Robbins explained.

Like a lot of revenue streams we watch here at The Next Platform.

Enterprises Fill In The Hyperscaler Gap For Intel’s Datacenter Business

There is a new tick–tock at work at chip maker Intel, and one that overlays the normal metronome cadence of manufacturing process shrinks and architecture advancement. This one is the tick of shipping products to hyperscalers, cloud builders, and a select few HPC centers and the other is the tock …

Server And Storage Spending Growth Looks Rosy Out To 2027

For a market that is so integral to the global economy, it sure is hard to get a complete dataset on quarterly and annual spending on information technology. We try to gather up all of the information we can find and flesh it out where we can so you can …

Is AWS Making The Switch To Homegrown Network ASICs?

Amazon Web Services, the juggernaut of cloud computing, may be forging its own path with Arm-based CPUs and associated DPUs thanks to its 2015 acquisition of Annapurna Labs for $350 million. But for the foreseeable future, it will have to offer X86 processors, probably from both Intel and AMD, because …

Be the first to comment