Excepting some potholes here and there and a few times when the hyperscalers and cloud builders tapped the brakes, it has been one hell of a run in the last decade for servers. But thanks to the coronavirus outbreak and some structural issues with sections of the global economy – let’s stop pretending economies are national things anymore, because they clearly are not – this could be peak server for at least a few quarters. Maybe a few years.

We started The Next Platform in 2015, but our experience in the systems market goes back to the aftermath of the 1987 stock market crash that eventually caused a recession in the late 1980s and early 1990s that really didn’t get resolved until the dot-com boom came along and injected a whole lot of hope and cash into the tech sector and then into every other sector that needed to become an “e-business.” When we think about transition points in IT, we think that the Great Recession was the point in time when a lot of different industries pivoted. And thus our financial analysis usually goes back to the Great Recession (when we are able to get numbers back that far) because we want to see how what is going on now compares to the difficult time we were going through then.

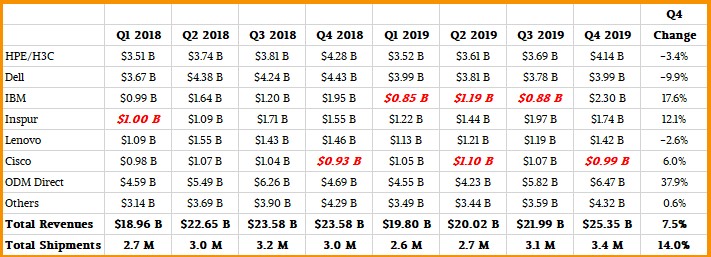

According to market researcher IDC, in the fourth quarter of 2019, which is technically a dozen years since the last recession started, server shipments were up 14 percent to 3.4 million units and revenues rose by 7.5 percent to $25.35 billion.

The big reason for that revenue increase was that the hyperscalers and cloud builders invested heavily in machinery in the quarter, with 1.05 million machines being sold by the ODMs who supply iron to these companies, up a stunning 53 percent and driving revenues up 37.9 percent to $6.47 billion. Clearly, with the hyperscalers and cloud builders buying mostly X86 servers and with increasing competition between Intel and AMD, the hyperscalers are getting great deals on processors with AMD leading the price/performance drive and Intel huffing and puffing to try to keep up without wrecking its profit margins. Don’t feel bad for Intel – the chip giant is driving historic revenues and very high operating profits in its Data Center Group even with the competitive pressure. IBM’s System z mainframes also perked up in the quarter, driving revenues for Big Blue up 17.6 percent to just a tad under $2.3 billion. Inspur, thanks to a very aggressive X86 and Power server business in China, saw revenues grow by 12.1 percent to $1.74 billion.

The rest of the server makers were either up a few points or down a few points. As we recently discussed in our analysis of the datacenter businesses of Dell and Hewlett Packard Enterprises, these two companies are exemplary of what is happening in the enterprise and among smaller Tier 2 clouds, telcos, and service providers. Dell and HPE have fiscal years that are distinct from calendar years, so IDC reconciles their numbers to the solar cycle for us. In the fourth quarter, IDC reckons that Dell had $3.99 billion in sales, down 9.9 percent, against 549,488 servers shipped out of its factories to the channel or to customers, down 5.4 percent. HPE, including its H3C partnership in China, actually saw shipment growth of 4.7 percent to 507,228 units and raked in $4.14 billion in revenues against that, down 3.4 percent but giving HPE the mantel of top server shaker money maker in the quarter – the first time that has happened in a while. Lenovo had $1.42 billion in server sales, down 2.6 percent, Huawei Technology had $1.28 billion, up 1.8 percent, and we estimated that Cisco had just under $1 billion in sales, up 6 percent.

To be fair, OEMs had a pretty good fourth quarter in 2018, making it a tough compare to this time around, even as the ODMs saw a pretty steep decline, making it an easier compare.

Here’s the table of server revenues, which we have had to estimate in a few points (shown in red bold) for the past two years by source:

And here is the same data extended back to the belly of the Great Recession presented in a chart:

Now, if you do a little math on these numbers from IDC, you will see that if you take out the effect of the ODMs, who together comprised 25.5 percent of the sales in Q4 2019, the rest of the server market was flat as a pancake revenue-wise. That was better than the 8 percent revenue decline in Q2 and the 6.6 percent revenue decline in Q3, but the big different is really those incremental System z15 sales from IBM. Take that out, we are back in negative territory for X86 servers in the enterprise, service providers, and telcos once again. (At least as a group. Intel said that its telco and service provider customers from Data Center Group had 14 percent growth in its fourth quarter and enterprises were off 7 percent, which matches this period in server sales being analyzed by IDC.)

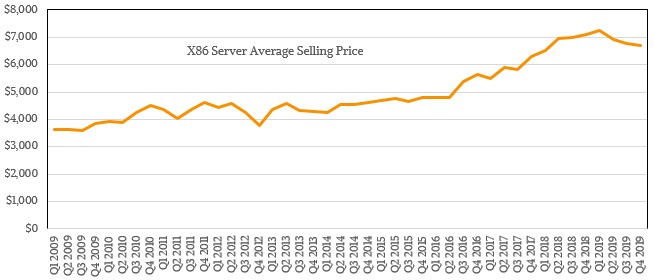

Thanks in large part to competition among Intel and AMD in the server CPU racket and falling DRAM and flash memory prices, the average cost of an X86 server has been trending downwards, as you can see:

The X86 server platform still represents something north of 98 percent of shipments, which grew by 12.9 percent to 3.35 million units (98.5 percent of shipments), with revenues of $22.44 billion (89 percent of revenues). Sales of non-X86 server shipments rose by 17.8 percent to $2.91 billion, and IBM’s System z and Power Systems machines accounted for 78.8 percent of that non-X86 slice of the server pie.

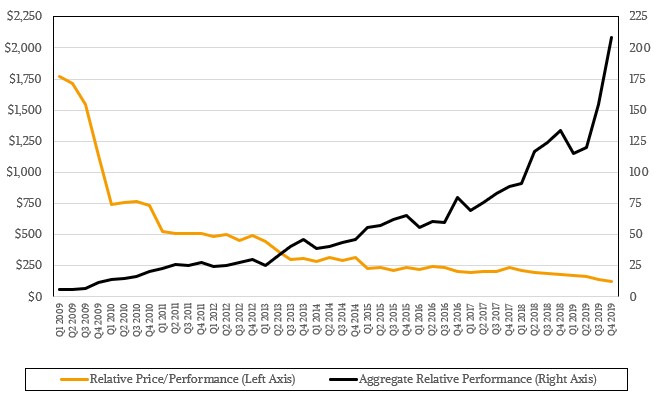

The amount of compute we are consuming is growing a lot faster than the price is dropping these days, as we have calculated since the Great Recession:

The amount of compute acquired in recent years, mostly due to the hyperscalers and cloud builders, is enormous, as you can see. How much steeper can that curve get if there is a recession? We may find out.

There was not a peep out of IDC about the coronavirus outbreak, and that is to be expected because the effects of the interruption to the supply chain for servers as well as the impact on buying patterns for enterprises, governments, service providers of all stripes, hyperscalers, and cloud builders. And the reason why is simple: No one knows. The error bars on any thought experiment, much less simulation, about the global economy right now are too large because some, many, all (take your pick) of the underlying variables that go into trends in the economy are changing.

What we can say honestly is this: If we do go into a recession, there is no question that some aspects of the platforms that we build will change. This has happened time and time again. Platform transitions are not caused by recessions, but they are often accelerated by them, particularly if companies can save money or do things they have always wanted to do or, better still, never even dreamed of doing. Let’s walk through it.

The move to proprietary minicomputers was certainly helped by the recession in the mid-1970s, which lingered for a while and then there was a mild one in 1980 and then again in 1981 and 1982 after the Iranian Revolution in 1979. Again an oil pricing shock jolted the system, although unlike last week, where we were worried that oil prices would be too low, in those two cases we knew they were going to be too high. IBM’s and Hewlett-Packard’s proprietary minicomputers took off then because companies wanted to computerize their back-office and factories, but they could not afford mainframes.

In the late 1980s, another oil price shock combined with “irrational exuberance” on Wall Street shocked the economy and the RISC/Unix transition was there to benefit. The client/server revolution of the late 1980s to early 1990s was not only a reaction to a sluggish economy where central host systems were wildly more expensive than PCs, which were on everyone’s desktops at work and which had to be made more useful for the sake of the IT budget, but it was also a precursor to the Internet age, where hybrid computing across PCs and servers became so normal that we don’t really talk about it much any more.

The dot-com bubble from around 1995 through 2001 coincided with the Unix revolution and then the rise of Intel iron and Linux and Windows Server, and this was an architectural change that was funded by fear of missing out and being stuck in a personal corporate recession as upstarts blew by you and left you in the ditch of economic ruin. We could argue about how much of the spending in the dot-com boom was wasted on hope and ideas, but the fear was running pretty high and companies like Sun Microsystems, EMC, and Oracle benefited mightily from all the hype and hope.

And after the September 11 attacks in the United States, we had another recession and that really put the nail in the coffin of RISC/Unix systems and marked the rise of Intel X86 server chips and within a few years AMD Opterons, and these systems rose until the Great Recession kicked in during 2009, when Intel essentially copied off AMD’s homework and created the “Nehalem” Xeon architecture that we are still using predominantly in the datacenter today. When that last recession hit, VMware was there with a credible, enterprise-grade server virtualization platform that allows companies to get their existing iron to run at a higher utilization by converging the workloads on physical servers onto virtual machines on a physical server, and this helped save the day. AMD had made some architectural compromises and also had some bugs in chips, and server makers were in no mood to be patient. They all fell in behind the Nehalems, and Cisco Systems went so far as to converge compute and networking and set off the whole server industry on a tear for converged platforms at the same time Nutanix was being founded to offer us hyperconvergence, which emerged in 2011.

This time around, if a recession should come to pass – and we surely hope that it does not – then AMD, Ampere Computing, and Marvell might be the big beneficiaries. Not Intel.

Intel’s margins will be taking a hit if the demand for CPUs takes a large enough dive and the bargain seekers will look for the lowest prices as the rule and no exceptions what with a tanked server market unable to quickly amortize any costly server CPU expenditures.

Intel’s supply constraints will be a non issue compared to what new constraints the Cloud/Hyperscalers bean counters will put on expenditures as the economy takes a hit from the pandemic. So there will be a corresponding drop in that buy CPUs at any cost because the mad server market/services growth rates will quickly amortize that cost and then only gravy afterwards market will turn so Scrooge McDuck pinny pinch that even Intel’s large war chest may be insufficient to stop the bleeding.

The layoffs at Intel will come at an ever greater rate as the only way to survive on thin margins and not totally drain the cash reserves is via big middle management/nonessential employee cuts any way possible as Intel can not afford to reduce its worker bees too much in the face of such massive competition. Engineers will once again represent a larger percentage of Intel’s staffing while the rest will be tossed under the nearest bus. So that mostly looks like some MBAs and other such non necessary for product development/production staffing will get the first cuts from that even larger axe about to be swung.

AMD is a very lean operation and is really going to be OK in any downturn and is already above water on a gross margin rate that Intel could never manage. And and AMD’s modular CCD die/wafer production yield able to give AMD so much more pricing latitude that even Intel’s Contra Revenue spigot wide open could not take back much before it’s too late. And Intel has more other competition including Micron’s QuantX XPoint offerings and other competition across all of Intel’s market segments. And speaking of segments Intel’s byzantine array of CPU product segmentation schemes is another thing to go and that’s one that can not logically continue if demand dries up.

Wow a few years back Intel was mothballing fabs and all in on 10nm but even its current market records will not suffice if its 10nm folly and Fab wafer starts shortages issues are solved by market demand drying up. That’s going to become mostly a replacement CPU market and customers in the mood for the best of the bargains that AMD will have no problems providing in addition to all that is other and non x86 in the market as well.

Intel employees will have to be seriously polishing up their CVs as that’s most prudent and find some employer that’s lean and in a growing market position if at all possible in a recessionary environment.