It is hard to take on either Intel or Nvidia in their respectively dominant CPU and GPU markets, and credit is due to AMD for taking on both companies at the same time to try to carve itself a larger slice of the datacenter pie.

AMD has been steadily growing its datacenter business for the past two years, and the fourth quarter of 2019 saw yet more progress on this front, both with Epyc processors and Radeon Instinct GPU accelerators, as far as we can intimate from the few statements that AMD makes about its datacenter business. That said, it has a long way to go before it has taken a lot of share away from either Intel or Nvidia, and it may just turn out that AMD gets a smaller piece of a much larger pie – and the same amount of pie it would have gotten if the market for server CPUs and GPUs was not growing as much as it is. Either way, AMD will be a healthy and credible second source for these components, and in certain sectors – starting, of course, with HPC simulation and modeling – it may even get dominant share among the upper echelon exascale machines being installed in the coming years.

We shall see.

What we do know is that president and chief executive officer Lisa Su has righted the AMD ship and reminded Wall Street analysts that the company on track for double-digit server CPU shipment share as it exits 2020, and thanks in no small part to the expected launch of the third generation “Milan” Epyc processors in the second half of this year. That should mean that AMD can double its server CPU revenue run rate, year on year. The question is can it double it again in 2021 and get what would be its rightful share of datacenter CPU capacity, which should be somewhere around 20 percent of the pie, given the way markets seem to work on planet Earth. We think that given the desire for competitive pricing in the datacenter and the issues that Intel has had in getting its 10 nanometer “Ice Lake” processors in the field, there is a very good chance for AMD to have that 20 percent share in 2021.

Whether AMD can hold onto it, heaven only knows. We saw AMD stumble and a resurgent Intel absolutely vanquish AMD from the datacenter back in 2009 and 2010, and one good recession – or more precisely, a bad one – hitting when there is a stumble by either player puts the market share in play bigtime. Intel won the Great Recession round, and sooner or later a recession will come around on the guitar again and when it does, there will be more tectonic shifts in datacenter compute. The odds favor a more rapid adoption of cloud and intense pricing competition on those fronts should this scenario go down, and that gives AMD a pretty good shot at maintaining its market share if it can stay on the roadmap from “Naples” to “Rome” to “Milan” to “Genoa” and beyond.

What we can say for sure is that AMD is in a lot better shape now than it was five years ago, both in the PC and in the datacenter, and good engineering of Ryzen processors as well as Intel’s inability to keep up with demand for Core PC chips have combined to give AMD quite a bump in PCs, which feeds back into its server business since they rely on related technologies and traction in PCs gives AMD credibility and the benefit of the doubt in the datacenter. (Just as it has for three decades for Intel, and used to for the suppliers of RISC/Unix workstations in the mid-1980s who wanted to get into servers.)

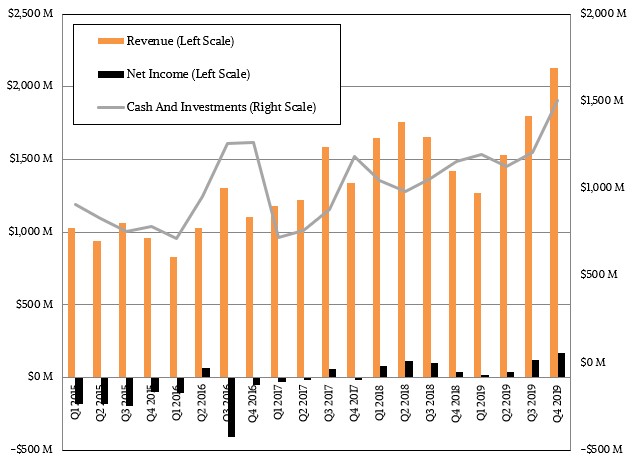

In the quarter ended in December, AMD’s sales were $2.13 billion, up 49.9 percent year on year, and net income rose by a factor of 4.5X to $170 million, or 8 percent of revenues. This revenue bump came despite a big slump in sales of custom processors to Microsoft and Sony for their respective Xbox and PlayStation game consoles, which are slated to be replaced at the end of this year with new models with upgraded AMD CPUs and GPUs. In the meantime, it’s the long and skinny tail of sales of the current custom chips, and the decline is something that sales of Naples and Rome Epyc processors could not make up for. The Enterprise, Embedded, and Semi-Custom business booked $465 million in sales in Q4 2019, up 7.4 percent, and it swung from an operating loss of $6 million in the year ago period to an operating gain of $45 million. Our estimates are that Epyc CPUs accounted for half of that revenue and no doubt the lion’s share of those operating profits.

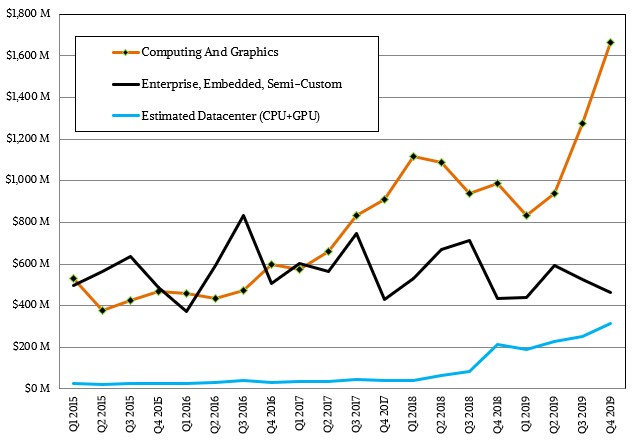

But the Compute and Graphics group was a bigger hero of the quarter, with revenues up 68.6 percent to $1.66 billion and operating income more than tripling to $360 million. Ryzen is a kind of leading indicator for Epyc, and that bodes well.

What everyone wants to know is how AMD’s datacenter business is doing, and Devinder Kumar, AMD”s chief financial officer, said that once again the datacenter share of the company’s sales in Q4 were in the “middle teens” percent range. At which point, everyone gets out their spreadsheets and does some guesstimating. We think AMD did $82 million in sales of Radeon Instinct GPU accelerators (about half from sales to Google for its Stadia gaming platform), up 28.4 percent, and another $232 million in Epyc processor sales, up 55.7 percent and significantly boosted by sales of Rome processors with 48 and 64 cores. Add it up, and AMD’s datacenter sales came to $314 million by our model, up 14.8 percent.

For the full year, we have AMD doing $293 million in Radeon Instinct GPU sales into the datacenter and another $694 million in Epyc CPU sales, for a total of $986 million and representing 14.7 percent of its $6.73 billion in sales. If all goes well in 2020 – and there is no reason to believe that it won’t – AMD will be ramping up volumes and should more than double revenues in the datacenter again, as it did from 2018 to 2019. Now, with game console chips selling again (possibly adding $750 million to $800 million in incremental sales in 2020), PC chip shortages abating somewhat because Intel is cranking up volumes of 14 nanometer and 10 nanometer chips to try to cut AMD off at the Ryzen pass, and datacenter CPUs and GPUs possibly adding an incremental $1.2 billion to $1.4 billion in sales in 2020, AMD should grow revenues by at least $2 billion if it can hold the PC line at the current rates. Call it an incremental $2.5 billion more in sales, just for fun, or $9.2 billion in all of 2020. The datacenter products could account for around a quarter of AMD’s overall revenues.

Should this come to pass, it will be quite an accomplishment for Lisa Su and her team of ex-IBMers and ex-Intelers. And this does not assume a very aggressive ramp on the Radeon Instinct front, which we are sure that AMD is going to start focusing on not only because it has some exascale supercomputer deals that depend upon it, but because the future of hybrid computing – which AMD was a pioneer in, you will remember – depends upon it. Among many other executive changes, AMD last summer quietly hired Brad McCredie, the IBM fellow who launched the OpenPower consortium and who steered the development of several generations of the Power processors, to be the corporate vice president in charge of AMD’s GPU platforms. And only a few weeks ago, AMD hired Dan McNamara, who had been running its Programmable Solutions Group (the formerly independent FPGA maker Altera), to be senior vice president and general manager of its server business.

Now Forrest Norrod, who is general manager of AMD’s Datacenter and Embedded Solutions Business Group, can focus on driving the datacenter roadmap instead of managing day to day operations. As the executive in charge of Dell’s Data Center Solutions custom server business several years ago, Norrod likes to hang out with hardware and software engineers and system architects to plot out the future, and we think this is exactly why Su is giving him space. We think this means a more concerted and focused effort on GPU computing for AMD. And quite possibly tighter integration in some form with one of the FPGA players, or an outright acquisition.

Xilinx, with a market capitalization of around $25 billion, is a little too rich for AMD’s blood, especially considering that AMD has only $1.5 billion in cash. But AMD has a market capitalization of $56 billion, so a merger would be interesting. It is far more likely that AMD would acquire smaller FPGA players Achronix, which is still privately held, or Lattice Semiconductor, which has a market capitalization of $2.8 billion. If we had to bet, we’d bet on Achronix because it would cost less and be more of a datacenter play. But all of this assumes that AMD wants to add FPGAs to its compute engine mix.

It does not help AMD when it’s included in the Enterprise, Embedded, and Semi-Custom accounting unit that all too cyclical Gaming Console APU numbers along with the Epyc(Now at Epyc/Rome) numbers and hidden away AMD’s actual Epyc uptake as well as growth figures.

Server market uptake is notoriously slow to unfold fully over more than a few years. But when financial analysis news articles begin to specifically mention AMD’s EESC accounting unit’s confusing numbers and how that the semi-custom part’s gaming console numbers may be making all things Epyc/Naples to Epyc/Rome look all the more confusing and not appear to be improving as well as expected then maybe AMD is more to blame there that anything else.

Epyc/Rome and its Motherboard ecosystem platform really offers way more value and features per dollar in a much more non market segmented manner compared to Intel’s byzantine levels of Server Processor product segmentation that it’s hard not to see the Epyc/Rome attraction and Epyc/Milan is sampling and scheduled for release this year as well.

AMD’s semi-custom gaming console part of that EESC assounting unit is the dictionary definition of a low margin consumer oriented and very very cyclical oriented sort of business. And currently the current XBOX-X and PS4 pre-Zen(Jaguar CPU) based Gaming Console APUs are at the end of their lifecycle and are experiencing that EOL sales volume slump as AMD makes ready its Zen-2/Navi-RDNA2 based next generation Gaming APUs for both MS’s XBOX(2020) and Sony PS5 next generation gaming consoles.

Also AMD’s current EOL gaming console APUs unit numbers have further been undergoing an Osborne Effect as the news leaks of AMD’s latest Zen-2/Navi-RDNA2 GPU micro-architecture based gaming console APUs become more numerous. How AMD’s management missed that in their advance of 2019/Q4 business guidance is amazing considering AMD’s past history with gaming console APU generational renewal cycles. So cosnumers have now even as far back as before Q4 2019 begun holding off on purchasing old XBOX and PS4 purchases in anticipation of XBOX(2020) and PS5.

AMD/Console and Fab Partners are scheduled to begin the New Gaming Console APU production ramp in Q2 2020 so any of AMD’s reporting quarters before those new gaming console APUs can be legally posted to the earnings reports are going to continue to throw off AMD’s other EESC accounting numbers. And to make things worse Gaming Console APUs are notoriously low margin sales and thereby tend to make the gross margin numbers look worse even while improving the revenue numbers.

AMD production volume and how to purchase by this analyst on EE&C quarterly revenue divided by product category channel inventory value on Average Weighed Price (AWP);

Epyc

q4 2017 = 89,213 units of supply

q1 2018 = 117,211 units of supply

q2 2018 = 357,003

q3 2018 = 445,297

q4 2018 = 178,426

q1 2019 = 148,784

q2 2019 = 766,115

q3 2019 = 137,346

q4 2019 = 310,640

Total Epyc = 2,550,035

Full Run Average Weighed Price $1942.72

Rome 1K AWP = $2184.53

Naples 1K AWP = $1927.31

Procurement strategy;

Low Volume – $1K AWP for proportional core grade’s split of full line production; Rome full line proportional split = $2184.53 per unit

High Volume $1K / 3 * 1.5 = OEM price

Rome by Core Grade AWP

64C = $6240.36 / 3 = $2080.12 * 1.5 = $3120.18

NRE + Margin Allowance is the difference between low and high

48C = $4280.00 . . .

32C = $2425.06 . . .

24C = $1519.11

16C = $903.42

12C = $625.00

_8C = $520.04

Rome ‘high volume’ full line proportional example = $2184.53 / 3 * 1.5 = $1092.26

v Intel Scalable; Rome combined in Ryzen 3xxx and Mobile 4xxx bundle.

v Intel 10 nm at 250 K Epyc units minimum $1K AWP / 3 = price concession.

Rome average supply ramp over 23 weeks = 10.7%

Naples average supply ramp over 117 weeks = 9.1%

Scalable Sky lake over 132 weeks = 10.6%

Scalable Cascade lake over 44 weeks = 9.8%

Naples & Rome combined share v Xeon Lakes on 1.30.20 = 2.4%

Naples & Rome + TR1/2/3 combined share v Xeon Lakes = 4.6%

Epyc by Core Grade to date;

64C = 00.98%

48C = 00.12%

32C = 35.12%

24C = 16.59%

16C = 26.31%

12C = 00.33%

_8C = 20.54%

By generation to date;

Rome = 5.99%

Naples = 94.01%

Rome ‘low volume’ bundle @ 1,000 units and AWP $2184.53

7742 64C = 16 units

7702 64C = 128 units

7702P 64C = 21 units

7642 48C = 7

7552 48C = 13

7542 32C = 14

7502 32C = 68

7502P 32C = 40

7452 32C = 52

7402 24C = 108

7402P 24C = 67

7352 24C = 62

7302 16C = 124

7302P 16C = 52

7282 16C = 20

7272 12C =56

7262 8C = 77

7252 8C = 43

7232P 8C = 33 units

Buy-in = $2,184,530

Upside = $72,330 or 3.31%

Rome ‘high volume’ bundle @ 100,000 units and AWP $1092.26

7742 64C = 1,551 units

7702 64C = 12,773 units

7702P 64C = 2,081 units

7642 48C = 694

7552 48C = 1,347

7542 32C = 1,428

7502 32C = 6,815

7502P 32C = 3,958

7452 32C = 5,223

7402 24C = 10,773

7402P 24C = 6,693

7352 24C = 6,162

7302 16C = 12,426

7302P 16C = 5,223

7282 16C = 2,040

7272 12C = 5,591

7262 8C = 7,672

7252 8C = 4,285

7232P 8C = 3,265

Buy-in = $109,226,500

Upside = $116,459,584 or 107%

I don’t know at what product volume levels AMD increases its discount . . . but everyone gets the idea; buy more and the overall upside increases a lot. There will be 8C loss leaders in this package that loss is made up through brokerage.

Data Center GPU it’s anyone’s guess. This analyst calculates 61,378 in q3 2018 and 66,025 in q4 2019 @ AWP $1495. I’m not sure if it’s a continuous volume. Might be deploy and later upgrade.

Thread ripper

q4 2017 = 582,508 units of supply

q1 2018 = 1,641,799

q2 2018 = 1,799,430

q3 2018 = 1,514,181

q4 2018 = 742,215

q1 2019 = 402,679

q2 2019 = 1,209,618

q3 2019 = 2,720,104

q4 2019 = 19,017

Total Thread ripper = 10,628,551

Full Run Average Weighed Price $1128.24

AMD owns commercial workstation market. This week share of all TR 1/2/3 v Xeon W 21/22/32 is 66%.

By Core Grade to date

64C = 0%

48C = 0%

32C = 24.00%

24C = 12.22%

16C = 36.80%

12C = 16.70%

_8C = 10.29%

By generation to date

TR 3 = 00.22%

TR 2 = 54.97%

TR 1 = 44.82%

Procurement strategy is the same.

See AMD 152 week full product line report here:

https://seekingalpha.com/instablog/5030701-mike-bruzzone/5400844-amd-q4-2019-channel-inventory-report

Mike Bruzone, Camp Marketing