Red Hat is coming onto IBM’s books at just the right time, and to be honest, it might have been better for Big Blue if the deal to acquire the world’s largest supplier of support and packaging services for open source software had closed maybe one or two quarters ago.

IBM was at the tail end of one mainframe cycle and at the beginning of a new one during the third quarter of 2019, and was up against a very tough compare in its Power Systems business as well. And as a consequence, despite some pretty healthy growth in its services and consulting businesses and a partial quarter of revenues and profits from its Red Hat division, IBM nonetheless had sales contract by 3.9 percent to just a tad over $18 billion in the quarter ended in September, and more surprisingly, net income was down by 37.9 percent to $1.67 billion as costs across all fronts – sales, administrative, research, development – all rose by 17 percent to $6.58 billion at the same time that intellectual property revenues (which are almost pure profit) fell by 39.6 percent to $166 million.

To its credit, IBM is investing in its future and is gung-ho about its transaction processing systems based on Power and System z processors as well as its prospects in the coming years with HPC and AI systems based on Power processors and any number of different kinds of accelerators. This, despite not winning either of the two CORAL-2 exascale system awards with the US Department of Energy at Oak Ridge National Laboratory and Lawrence Livermore National Laboratory, where IBM’s GPU-accelerated Power9 systems – “Summit” at Oak Ridge and “Sierra” and Lawrence Livermore – are the pre-exascale incumbents. The Summit and Sierra deals were contracted at $325 million, which is a big chunk of change for any vendor, and the two exascale systems that replace them – “Frontier” at Oak Ridge and “El Capitan” at Lawrence Livermore – are together accounting for around $1 billion in system acquisitions and another $200 million or so in non-recurring engineering (NRE) costs. Those deals did not impact IBM’s books her in 2019, but the fact that IBM did not win either deal will absolutely have a downdraft effect on its revenues in 2022 and 2023, when these two machines are expected to be accepted by their respective labs and therefore generating revenues.

Jim Cavanaugh, IBM’s chief financial officer, reminded the Wall Street analysts on a call to go over the Q3 2019 figures that a year ago was when the bulk of the revenue came in for the Summit and Sierra machines, and moreover that it was also when Big Blue was starting to ship its midrange and high-end Power9 NUMA systems aimed at enterprise customers, who were champing at the bit for faster iron after more than a three-year wait since similar machines based on the Power8 processor were launched. So it was really no surprise that Power Systems revenues were off 27 percent in the quarter just ended.

That decline ended seven straight quarters of growth for the Power Systems line, which has been gradually rising after falling from a pretty high height over the past decade – as happened with all makers of RISC/Unix iron. Hewlett Packard Enterprise just gave up on its HP-UX systems business (thanks in no small part to the dead-end Itanium processor it helped create with Intel) and is selling high-end Windows Server and Linux machines based on fat Xeon SP processors these days along with its own HPE and SGI chipsets. Sun Microsystems was eaten by Oracle a decade ago, and Oracle has quietly stopped developing Sparc/Solaris machines even if it is very much interested in trying to revive a traditional HPC simulation and modeling business. (Sun had mixed luck in HPC, at best.) IBM won the RISC/Unix Wars, but has been unable to expand its Power Systems business with Linux to the levels that were normal a decade ago.

While the fall has been dramatic, the thing to consider is that IBM has been able to grow its Power Systems business and through the OpenPower Foundation and partners such as Supermicro and Inspur as well as a few others, has been able to increase the overall Power-based systems business. It is still utterly dwarfed by the X86 systems business, mind you. But growing despite the efforts of Intel and AMD – as well as the encroachments by the Arm collective in the HPC space in particular – is absolutely an accomplishment.

IBM’s top line in the Power Systems business is hurt by not winning the CORAL-2 procurements, to be sure and which have gone to Cray, but its profitability and longevity will not be. It is not clear that any of these pre-exascale or exascale deals are going to be profitable when all is said and done, and we would argue that they are break-even by design because they are really research, development, and preproduction for systems that any vendor that wins a capability-class supercomputer deal does to create a product that it can sell at much higher prices to large enterprises and government, academic, and research institutions.

That’s the theory, anyway.

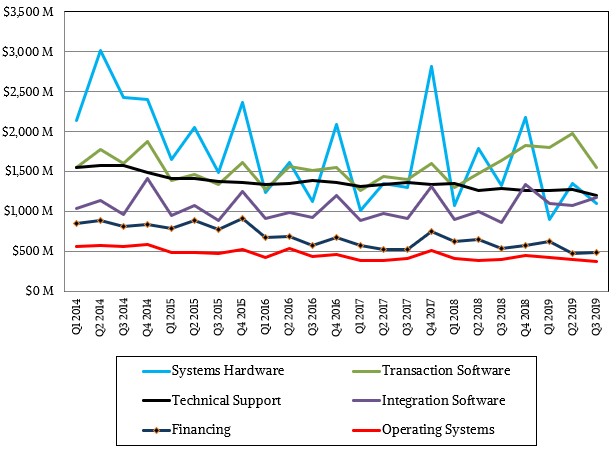

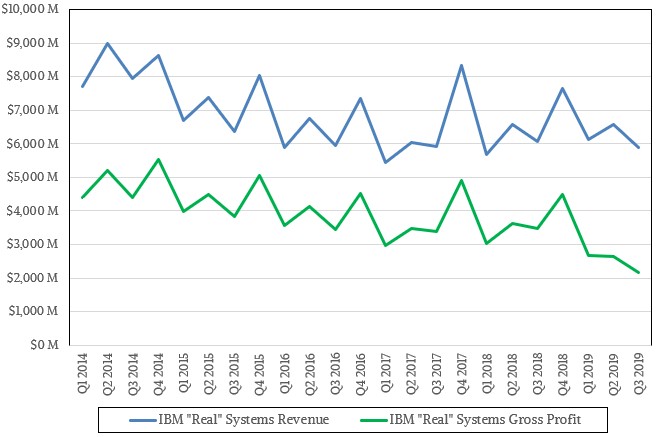

Let’s go through the numbers. In the quarter ended in September, IBM’s indigenous systems business – which does not include Red Hat Enterprise Linux or any of the OpenStack or OpenShift Kubernetes extensions to it – had $1.48 billion in sales to customers and channel partners, down 14.7 percent. The Systems group sold another $195 million in gear to other IBM groups, which actually rose 7.7 percent. So Systems group revenue, as reported, was down 12.6 percent to $1.68 billion. System hardware sales were off 17.2 percent to $1.1 billion and operating system revenues were off 17.7 percent. IBM had gross profits of $785 million on this core systems business, but only $39 million of that dropped down as pre-tax income. This is lower than normal, but a lot better when IBM takes a $186 million, $203 million, or $202 million pre-tax loss, which happened in Q1 2017, Q1 2018, and Q1 2019. This is when the investments in the future are running high but sales slump after the typical big bang in the fourth quarter.

Last month, IBM launched its System z15 mainframe, which we covered over here, and it only had a week’s worth of sales for this new iron in the third quarter. In the coming quarters, there should be a nice spike in sales, which should counterbalance the lengthening tail of Power9 sales, which started shipping in earnest throughout 2018 and which will be replaced by Power10 systems in 2021. It is going to be a long second half of 2019 and full 2020 for the Power Systems division, with an uptick for Linux shops that will be able to get their hands on the forthcoming Power9’ “bandwidth beast” system that we told you about two weeks ago.

IBM does not report specific sales figures for its System z, Power Systems, or storage array sales within the Systems group, but Cavanaugh did say that System z sales declined 21 percent ahead of the z15 launch and that Power Systems sales were off a gut-wrenching 27 percent. Storage array sales were off 6 percent, which is a lot better than what has been happening. Operating system sales – meaning MVS, VSE, VM, and Linux on mainframes as well as AIX, IBM i, and Linux on Power but not any of the Red Hat revenue that was brought onto the books and put into the Cognitive and Cloud Software division – fell by 8 percent, and we think they accounted for $380 million in sales. Red Hat accounted for $371 million in the portion of the quarter that IBM could put on its books, and grew 20 percent year on year. It won’t be long – only about a year or so – before the Red Hat software business will be generating the kinds of revenues that the Power Systems business did a decade ago.

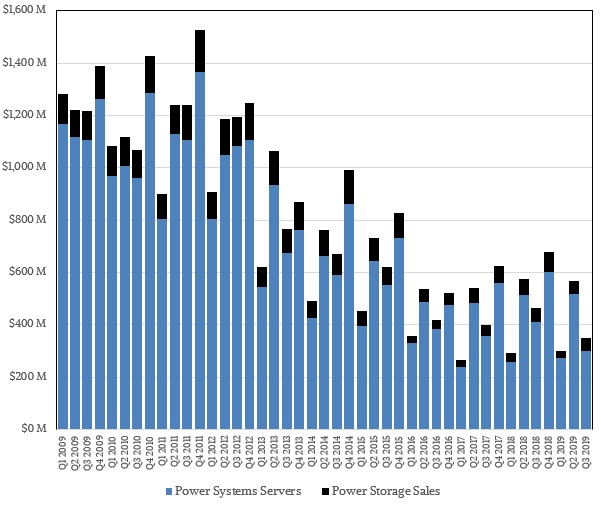

Because we are interested in how the Power Systems platform is doing, we built a model of revenues going back to the beginning of 2009, which is at the darkest hours of the Great Recession when everything – alright, a lot of things – changed in technology and in the economies of the world. Back then, IBM was still generating on the order of $1.2 billion in Power Systems sales each quarter (a combination of internal and external revenues) as well as around $120 million each quarter in Power-based high-end SAN array sales that are not counted as Power Systems sales but are still really Power iron underneath those DS8700 and DS8800 and now DS8900 labels.

Here is the quarterly trend of Power Systems sales, based on our own model, with raw systems and revenues from sales to the storage division added on top:

The overall trend, if you average it out over a year, is up modestly. Obviously, the Summit and Sierra deals helped a lot in 2018 once the revenue for these machines was recognized. But the underlying Power Systems business is still big enough – and strong enough – for IBM to commit to Power10 and Power11 2021 and 2024 and do its best to commercialize the HPC and AI systems it has more broadly while maintaining the substantial and steady transaction processing business on AIX and IBM i and expanding into SAP HANA on Linux to take on HPE head on.

The thing to remember is that the Power Systems business is more than just iron, and it is more than just what IBM breaks out in its financial reports. Our best guess is that Power-based servers and storage plus operating systems and sales to the Global Technology Services unit for outsourcing customers drove around $2.7 billion in 2018. The number will be lower in 2019, but probably only by between 5 percent and 10 percent once all of the pieces of the Power platform are counted.

And looking further down the road, there is still no indication what IBM will do to make the entire Red Hat stack run best and cheapest on Power-based systems. There is an opportunity for Big Blue here, and it will be interesting to see what it will do. If done properly, this opportunity is larger than a pair of $500 million exascale machines sold to the Department of Energy, and probably a lot more profitable, too. By definition, as it turns out.

Are we still trusting supermicro even after backdooring motherboards for the Chinese government? Seriously though, the best thing that can happen with IBM is they suffer a quick death and dissolve their remaining assets to better firms. They don’t innovate and their death spiral, while slow, is inevitable. Marketing will only keep them around so long, and hopefully they won’t take many more good companies down with the. I’d hate to see redhat assets sold to the incompetent boobs at HCL.