While there is no question that Amazon Web Services is the largest and most profitable public cloud on planet earth, and that it provides the best subsidy imaginable for a cut-throat online retail business that is its parent company, AWS has not taken over the entire IT world any more than Amazon has become the sole place to buy stuff.

It may feel like that sometimes, but the data doesn’t support that.

As we mused way back in 2015 when The Next Platform was founded, it is hard to imagine how in hell any public cloud provider will catch AWS. Some providers – notably Google and Microsoft – have been growing faster than AWS, but it doesn’t feel like they are really gaining on it. It is helpful to remember that AWS is getting only about a third of public cloud spending, and that the public cloud probably only represents about one-eighth to one-tenth of the worldwide spending on datacenter systems and enterprise software together. (Around $614 billion in total for 2019 is the latest projection we have seen from the prognosticators at Gartner.) The share that AWS has of the whole pie depends on the assumptions in the larger models.

No business can grow forever at triple digits or even double digits, and we pointed this out three years ago as it relates to AWS. The trick is to grow fast for as long as possible, and AWS has been brilliant at moving up the stack from infrastructure to platform to software as services, using one to build the foundation for the next one in a manner that is consistent with the way the world thinks about information technology. This layering gave it different waves of triple and then double digit growth, which prolonged the overall growth cycle and which has kept AWS growing faster than the public cloud market at large and many multiples faster than overall IT spending or global gross domestic product.

Given the frequent price cuts, enormous and lumpy infrastructure investment cycles, and varying nature of the workloads and customers that use AWS, it can be tricky to predict what the company will do looking ahead. The dozen years of estimated and actual financial results for AWS are handy, to be sure. But past performance is no guarantee of future performance, as they say on Wall Street.

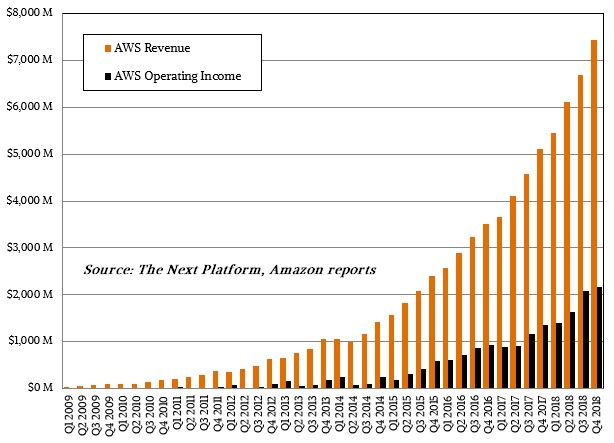

In the fourth quarter, which Amazon reported its figures for this week, sales at AWS rose by 45.3 percent to $7.43 billion, and as has been the case for the prior four quarters, operating income on the Amazon public cloud unit rose faster than revenues did, in this case for the final quarter of 2018 rising by 60.8 percent to $2.18 billion. AWS is getting better a wringing more money from its investments, and we think that has as much to do with adding platform and software services atop its raw compute, network, and storage infrastructure as it does arguing about pricing with suppliers and driving up utilization across its vast server fleets.

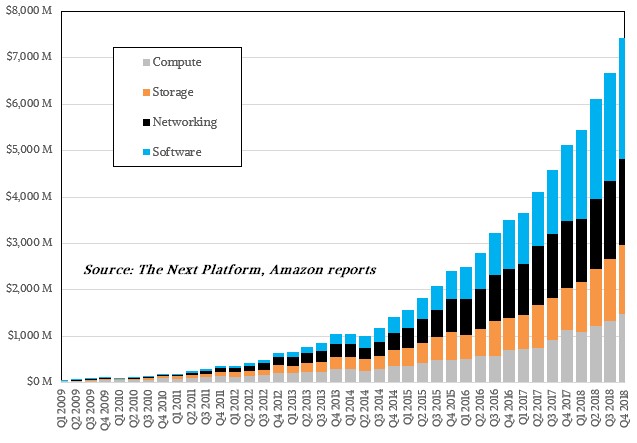

For the full 2018 year, AWS had sales of $25.66 billion, up 47 percent, and operating income of $7.3 billion, up 68.5 percent. The revenue and profit growth accelerated in 2018 compared to the growth from 2016 to 2017, so you can’t think that a gradual and consistent downward trend is inevitable. New services behave accordingly, exploding in usage and cash, old ones are like printing presses, cranking out the steady streams of money. AWS is a mix of hundreds of services of various vintages and tens of thousands of possible SKUs – and with hourly utility pricing and an off switch, too. If we had to guess – and we do because Amazon doesn’t provide any detail on what services generate any particular revenue or growth – we suspect that in 2018, compute in its various forms drove 20 percent of AWS revenues, storage another 20 percent, networking 25 percent, and the remaining 35 percent came from higher level platform and software services such as databases and data analytics stacks. Our model, which admittedly is based on wild guesses about the distribution of compute, storage, networking, and software revenues at AWS, looks like this:

Compute has grown by a factor of 42X in the past decade in this model, but storage has grown by 183X, networking by 228X, and software by 959X. We think they were all more or less at the same level around 2014 or so, and software has really taken off since then. At some point in the future, and it is hard to say when, AWS revenues will reflect the distribution of compute, storage, networking, and software in the broader IT market, but with compute being a bit cheaper and networking being a bit more expensive and therefore we have to adjust the relative revenues a bit. Moving data around AWS and out of AWS is a relatively expensive proposition, and an intentional one that is designed to get people gathering it in the cloud, chewing on it in the cloud, and rarely moving it off the cloud. Real datacenter gear and systems software that companies buy for on-premises installations does not have this bias. It’s all expensive to acquire. (Smile.)

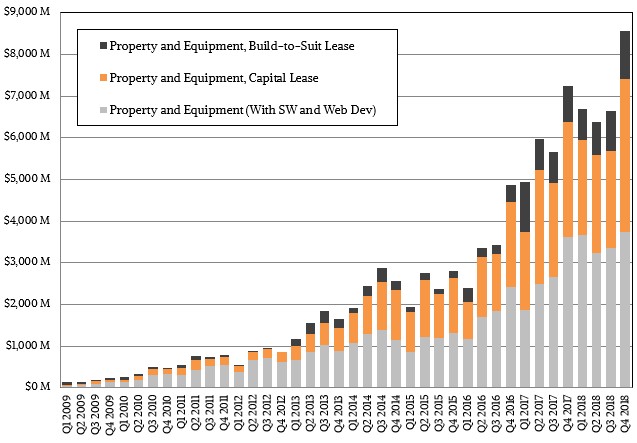

It may not seem like it, with the server market booming like crazy in 2018, but in terms of growth rates, the investment in AWS in infrastructure – either bought or leased – Amazon actually took its foot off the gas in 2018 a little, particularly compared to infrastructure investment growth in 2016 and 2017. Take a gander at this:

“On capital, especially infrastructure capital, if you use the capital lease slide as maybe an indicator for what we have invested into our AWS business to support infrastructure and global expansion, that number grew 10 percent last year, when it had grown 69 percent in 2017,” explained Dave Fildes, director of investor relations, in the call going over the numbers with Wall Street. “So, in a lot of ways, 2018 was about banking the efficiencies of investments in people, warehouses, and infrastructure that we had put in place in 2016 and 2017. While we will continue to concurrently drive growth and customer offering and Prime benefits, we certainly do take costs seriously and we will continue to work on operational efficiencies. I would expect these investments to increase relative to 2018.”

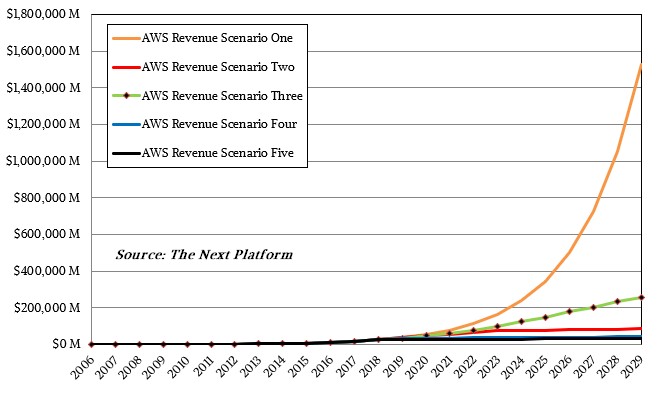

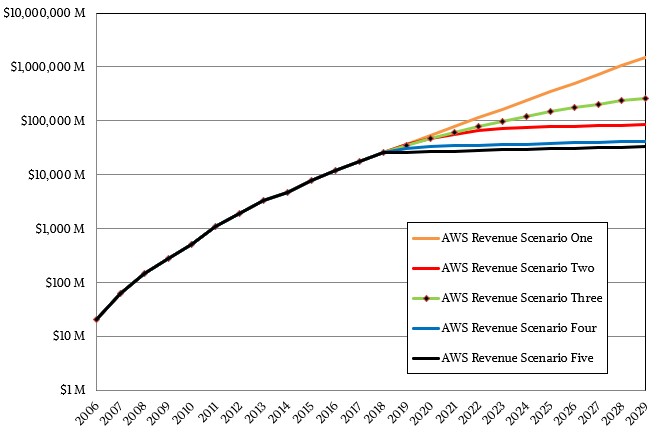

We though it was a pretty good time to also update out revenue growth model for AWS, which we put out in early 2015 as a thought experiment, and to illustrate why the high growth rates that AWS enjoyed between 2006 and 2012 could not hold.

Here’s what it currently looks like on a linear scale for the Y axis of revenue and the X axis of time:

This model shows the estimated and actual AWS revenue figures since 2006, when the cloud unit was founded, and then uses different projections of revenue growth moving forward.

In Scenario One, revenue just keeps on a-growing at 45 percent annually between now and 2029, a decade from now, and by the end of it AWS is a $1.5 trillion company and has essentially eaten all of the IT sector and killed off whole portions of it that are no longer needed. This is not a very probably scenario. In Scenario Two, growth tapers off a little bit each year until around 2024, when it grows at the rate of GDP – a pessimistic or perhaps realistic, depending on your mood, 2.5 percent each year. In Scenario Three, the growth rates take a bit longer to come down but step down nonetheless, and with Scenario Four they step down fast over two years and then hit that GDP level. Scenario Five is the bad one –AWS just grows at 2.5 percent starting this year, and this is also very much unlikely. Scenarios One and Five are the ceilings and the floors, and we think reality will be somewhere around where Scenarios Two and Three are in the chart. This one plots our forecast on a log scale for revenue, which makes it a little easier to read:

So AWS could break $85 billion in sales in 2029 by Scenario Two or $260 billion in Scenario Three. We are pretty sure that Amazon founder Jeff Bezos would love to break $100 billion in sales, and there is every prospect – and room in the market – for that to happen well ahead of 2029, especially if AWS keeps innovating the way it has been doing for the past dozen years. It will be the 20th anniversary of AWS in 2026, and that will be about when we expect AWS to cross that line. Heaven only knows what Amazon’s market capitalization will be by then. . . .

You are predicting 10 years into the future in a volatile market.

Please…

>Some providers – notably Google and Microsoft – have been growing faster than AWS, but it doesn’t feel like they are really gaining on it.

Have you really checked the latest Microsoft financial report?