Sometimes, you just have to be amazed by a good stroke of luck in the IT sector. Just as its competition in processors was getting the most intense that we have seen in a decade and a half, the demand for compute has risen so high, so fast, that it has not only carried Intel over the rocky shoals, but has raised it to new heights of revenue and profitability.

With its significant woes with its 10 nanometer manufacturing capability, there are still some big rocks ahead as Intel navigates past the “Cascade Lake” and “Cooper Lake” Xeons and tries to reach 10 nanometers in early 2020 with the “Ice Lake” Xeons. But for now, the company’s Data Center Group is awash in revenues and profits – much more than it ever anticipated as 2018 got started, and more than anyone really expected, to be frank.

The goods news is that the steep demand wave for compute is letting all boats rise, which will over the long term create the kind of competition that will very likely put some pressure on revenues and even more on profits. That’s just the way markets work. It is up to the competition – the main ones are AMD with Epyc processors and Radeon Instinct CPU coprocessors, Nvidia with Tesla GPU accelerators, Xilinx with Everest FPGA accelerators, IBM with Power9 processors and their wealth of high speed interconnects, Cavium with ThunderX Arm processors, and Ampere with eMag Arm processors – to catch the same waves and to make some while they are at it.

In the third quarter ended in September, Intel brought in $19.16 billion in revenues, up 18.7 percent from the year ago period; operating income rose by a pretty impressive 43 percent to $7.35 billion, and net income rose nearly in concert by 41.7 percent to $6.4 billion. The PC business has taken an unexpected upturn and Intel is chasing the high end of that line, leaving some of the entry market for AMD to catch, and the demand for PC chips is making it tough for the company to balance out its “Skylake” Xeon SP production. Intel is similarly pumping out high end chips with the highest prices and (presumably) the best margins to capture this wave of demand. It must be quite a stressful juggling act inside of Intel’s fabs right now – but there are worse problems. Like not having 10 nanometer server chips out the door next year when AMD is going to be ramping up its “Rome” kicker to the “Naples” Epyc 7000 that launched last summer beside the Skylake Xeons and that have gotten AMD back into the datacenter conversation again as well as some money.

We called Intel’s Data Center Group unstoppable a few years back, when this competition was just a storm forming on the horizon, and even now, when the storm is overhead, nothing seems to be slowing Intel down in this vital part of its business. And that is mainly because the hyperscalers and cloud builders have such appetites for compute right now that they can’t wait for future Xeon processors from Intel. As they get more comfortable with the alternatives, the hyperscalers and cloud builders could shift more work off of Xeons, but the big public clouds only really have AMD Epyc chips as an alternative to Xeons because the vast majority of customers on the public clouds are doing so with X86 applications running atop Linux or Windows Server. Hyperscalers (and those public clouds that offer hyperscale-style services) can do whatever they want, as Microsoft is doing with an Arm-based version of Windows Server it is using for certain services on the Azure cloud. But the cloud providers can’t.

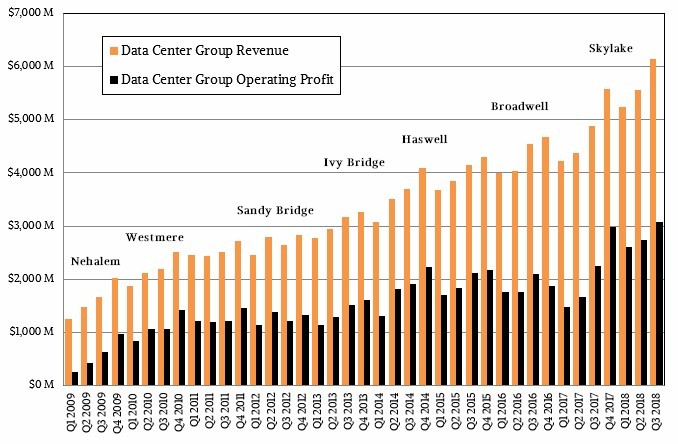

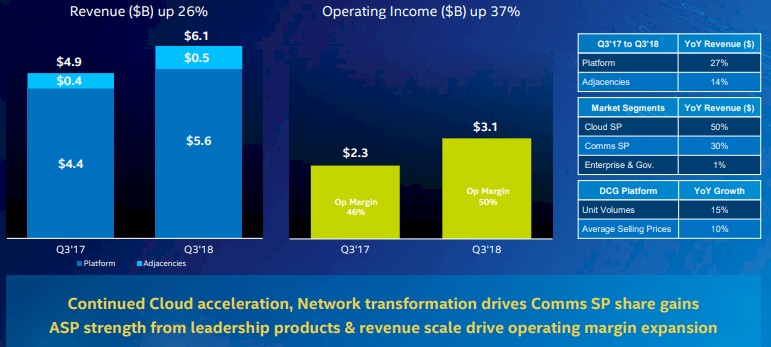

In the third quarter, Data Center Group, which makes Xeon processors (and Xeon Phi coprocessors until they were discontinued) and their chipsets and motherboards as well as adjacent technologies such as the Omni-Path interconnect, sold $5.64 billion in platform products, up 27 percent, and $502 million in adjacencies, up 14.4 percent. So overall sales for Data Center Group jumped to $6.14 billion, up 25.9 percent. Operating income for Data Center Group was $3.08 billion, up 36.7 percent. With that said, Intel’s Client Computing Group, which makes chips for PCs and other client devices, still rakes in more money, with $10.23 billion in sales and $4.53 billion in operating profit.

That PC business is why Intel is so formidable in the server business, and vice versa. It can’t have one without the other because Intel, unlike all of the other players in compute, builds its own factories and they are ginormously expensive. A modern fab is something on the order of $12 billion these days. All of this cash will certainly help Intel revamp its 10 nanometer processes, which we think it is doing despite the protestations otherwise – Intel may have not killed off 10 nanometer like Globalfoundries killed off its close sibling 7 nanometer a few months back, but we are pretty sure that whatever Intel was trying to do did not work and it has gone a long way back to the drawing board to recover. So that cash over the past five quarters of boom time buys Intel the time to go back and fix 10 nanometer while milking 14 nanometer extra hard.

Intel no doubt has hopes that AMD will ship its Rome Epyc CPUs and “Vega20” GPUs, the former due in 2019 and the latter due any day now, later rather than sooner using the 7 nanometer processing techniques from fab rival Taiwan Semiconductor Manufacturing Corp. Hopefully, for the sake of competition, AMD can keep its foot on the TSMC gas and give both Intel and Nvidia a run for the money and help drive some of the high prices in CPUs and GPUs down a bit.

Then again, with all of this demand, what is the point in driving the price down? Perhaps everyone will just compete just enough and wait for a recession to start fighting on price as well as features. You can’t blame them if they do. Pile the hay high while the sun is shining bright. . . . and let the supply and demand curves do as they do. If there is a delay at TSMC – and we are not saying we think there is, but 7 nanometers is tough to do – it is not like Globalfoundries gave up on 7 nanometer and Intel is struggling with 10 nanometer and Samsung is probably working real hard with its 7 nanometer, too.

Hopefully, system makers are getting a piece of the action, but as far as we can tell, most of the profits in Xeon compute are going straight to Santa Clara, do not pass go and definitely do not collect $200. Well, maybe about $200.

As has been the case for many years now, the hyperscalers and cloud builders who are always at the front of the line at the fabs to get chips are buying lots of them. In the quarter, these companies, which Intel calls cloud service providers, pushed an incredible 50 percent revenue growth from this time last year. The smaller communications service providers – telcos, cable companies, and other service providers – as a group delivered 30 percent revenue growth for Intel in the third quarter, which is nothing to complain about. The enterprise and government sector, which is often trending downwards these days, actually had a 1 percent uptick, which is a good sign about how enterprises feel about investing in core IT compute these days. (They aren’t cutting is the point.) These cloud and comms customers account for about two thirds of Intel’s Data Center Group revenue these days.

Intel’s unit volumes across chips, chipsets, and motherboards within Data Center Group rise by 15 percent, boding well for a good fourth quarter for OEMs and ODMs, and average selling prices managed to rise by 10 percent. If volumes are up and ASPs are down, that means there is some price pressure and we think it is at the high end of the Xeon line where Intel is probably struggling to keep up with demand.

Intel chief financial officer and interim chief executive officer, Bob Swan, said on a call with Wall Street analysts that the Skylake Xeons were doing well even as the Cascade Lake Xeon SP chips loom, calling out the hardware-based mitigations for some of the Spectre/Meltdown speculative execution security vulnerabilities that Cascade Lake will include as well as the VNNI machine learning interface instructions that are in the future chips. (We talked about these here.) Swan also said that after pulling back on having so many variants of the Xeons with the Skylake generation, Intel expected to have many more custom SKUs with Cascade Lake – 60 percent higher than with the Skylakes, although we don’t know the number of SKUs that this generation had. Cascade Lake is still on track to ship before the end of the year, which is not tough since it is really just a tweaked Skylake using a tweaked 14 nanometer process that is very mature at this point. Cooper Lake follows in the middle of next year with some more tweaks on the CPU and the process, but we won’t see Ice Lake with 10 nanometer processes, a multichip design akin to that which AMD uses in the Epyc processors, and a new server socket until early 2020.

Swan also said that Intel shipped more than 8 million processors into the compute, storage, and networking segments of the datacenter, against a total addressable market that was estimated at around 30 million units. (There is a lot of Arm gear in the datacenter, it just isn’t in servers.)

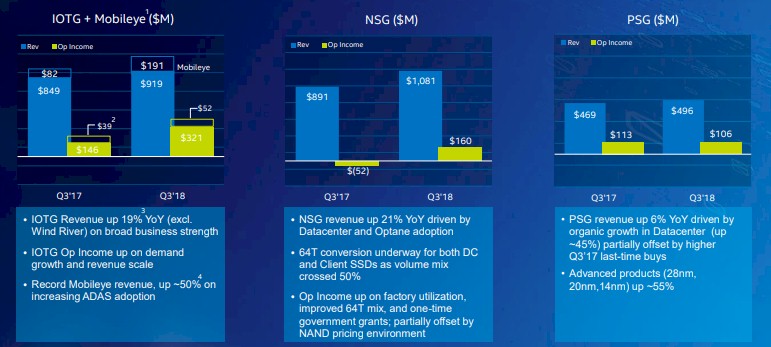

The adjacent IoT Group, Non-volatile Storage Group, and Programmable Solutions Group all have a datacenter component to what they do, although Intel does not lump the revenues and profits or losses them these three groups into the Data Center Group. Here is how the third quarter turned out:

We think it is significant that within Programmable Solutions Group, sales of the more advanced Altera FPGAs – those made using 28 nanometer or 20 nanometer processes from TSMC or 14 nanometer processes from Intel – rose by 55 percent in the quarter, showing that there is demand for the more recent devices. That said, FPGA sales were only up 5.8 percent to $496 million; operating income was actually down 6.2 percent to $106 million.

Sales of flash and 3D Xpoint Optane memory helped Non-volatile Storage Group push its revenues up 21.3 percent to $1.08 billion, and this business is finally making a little money, with operating income of $160 million compared to an operating loss of $52 million in the year ago quarter. Swan said that Intel had shipped the “Apache Pass” Optane DIMMs that were originally supposed to be an integral part of the “Purley” platform using the Skylake Xeons to Google, Microsoft, and Alibaba, three of the Super Eight. With the costs of its separation from Micron Technology on both flash and 3D XPoint memory development and manufacturing, the Non-volatile Storage Group is expected to break even at the operating income level for all of 2018. As part of its contract with Micron, Intel has a predictable and steady supply of flash and 3D XPoint memory through 2020, and is beginning to explore its internal manufacturing options.

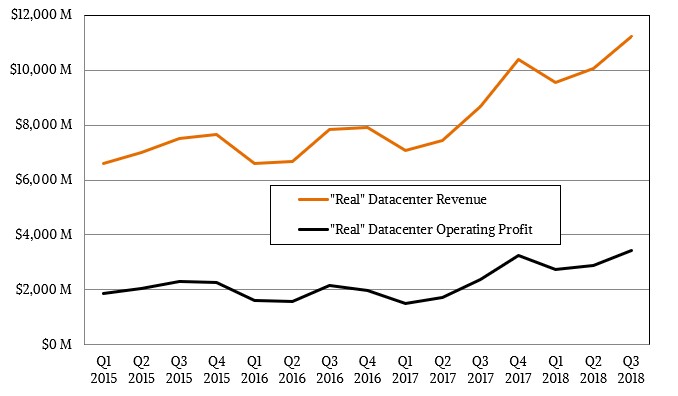

We have once again tried to reckon from Intel’s numbers what its “real” datacenter revenues look like, and they are always much bigger than the reported figures for Data Center Group because some of that IoT stuff and a lot of that FPGA and non-volatile storage ends up in the datacenter, not just in personal computers. It is a rough guess, we realize:

Because of the relatively low operating profits that flash and FPGAs have relative to all of the Xeon CPUs, chipsets, and motherboards, this datacenter business operating profit is a bit lower than what Data Center Group proper reports. So, that’s why Intel does it that way. In any event, we think that this real datacenter business at Intel generated around $7.78 billion in revenues, up 23.1 percent, and had an operating profit of $3.44 billion, up 45 percent. This is the biggest shift in profitability that this datacenter business has ever seen, the highest level of profitability (and close to the highest percentage if revenue, second only to how it did in the final quarter of 2017), and the highest revenue it has ever generated.

Intel has expanded its total addressable market to over $300 billion and has raised its guidance for revenues for all of 2018 by $8.4 billion since the beginning of the year, just to show you how big that new crest of the wave is.

Looking ahead to the final quarter of the year, Swan said that Intel was projecting that it would hit $71.2 billion in sales, up 13 percent against a pretty tough compare, particularly for Data Center Group, and added that the PC business would rise about 9 percent and the data-centric businesses would rise about 20 percent. For the fourth quarter by itself, Intel is looking at bringing in $19 billion flat with some slight downward pressure on margins as it makes investments in 10 nanometer manufacturing and 7 nanometer research and development. Intel did give guidance for Data Center Group, with Swan saying that growth for the datacenter business (as reported) would be “north of 20 percent” for the year and that during the fourth quarter all indications were for “really solid demand” with sales to come in around $6.3 billion.

We don’t know where this talk of a slowdown in server spending is coming from, but whatever the source, Intel is not seeing it.

Be the first to comment