It has been a long time coming, but hyperconverged storage pioneer Nutanix is finally letting go of hardware, shifting from being an a server-storage hybrid appliance maker to a company that sells software that provides hyperconverged functionality on whatever hardware large enterprises typically buy.

The move away from selling appliances was something that The Next Platform has been encouraging Nutanix to do to broaden its market appeal, but until the company reached a certain level of demand from customers, Nutanix had to restrict its hardware support matrix so it could affordably put a server-storage stack in the field and not lose its shirt supporting it. Some would argue, given the staggering cumulative losses that Nutanix has incurred over its history breaking this new type of operating system into the datacenters of the world that even this simplification is not enough. This is the price that innovators have to pay some time to change the world.

The question we have as we examine the prospects of hyperconverged storage is whether this entire category, which Nutanix has been the standard bearer since it uncloaked from stealth mode in August 2011 with the Scale Out Converged Storage, or SOCS, the which provided virtual storage in the form of block and file structures on servers equipped with disk and flash and running a hypervisor atop the cluster. This hyperconvergence has been a hot idea since then, with many players jumping into the fold and shifting many companies away from traditional SANs whiel making it easier and cheaper to buy compute and storage and to manage it. The only problem with have with this hyperconverged approach is that it is, in fact, precisely and exactly not what Google and Amazon and Facebook and Microsoft do on their hyperscale infrastructure. Yes, Nutanix has created an impressive cloud operating system that can rival anything that Microsoft, Red Hat, or VMware can put into the field, but what the real clouds and hyperscalers are building is disaggregated storage and compute that is encapsulated in datacenter-spanning networks with 100,000 nodes, in mixed proportion of storage and compute as needed. They are not running storage and virtualization, or even bare metal servers, on the same nodes. In fact, because they are not hyperconverged, they can run compute or storage in bare metal mode.

This, we think, could prove to be a problem as large enterprises grow their workloads. And it will particularly be a problem for many companies considering the hefty premium that Nutanix and its peers are charging for hyperconverged functionality. In many cases, the vast majority of the value of a hyperconverged node – call it $80,000 or $90,000 or so out of a $100,000 to $110,000 node cost – comes from the software stack. Given the lower margins on hardware, you can understand why Nutanix has always wanted to get rid of hardware appliances and shift solely to selling software, and thereby boost its margins. The company, which is in the midst of this transition now, will take a short term revenue hit, but its gross margins should improve given the fact that server makers who don’t have their own hyperconverged solutions – Dell has vSAN and ScaleIO by virtue of its VMware and EMC acquisitions, Hewlett Packard Enterprise has SimpliVity by virtue of that deal, and Cisco Systems has Springpath thanks to its own acquisition – will want to sell Enterprise Cloud Platform, particularly to those enterprise and midrange customers who don’t want to – or need to – create what the hyperscalers and cloud builders have made for their vast applications. For many companies, ease of use trumps sophistication, and VMware and now Nutanix have brilliantly played to this hand. There are far more companies that need something that is easy to use than something that is best of breed in all components and has to be assembled and maintained by fleets of PhDs on the payroll.

The trouble with Nutanix is that it is still not making money, and while the shift away from hardware will help in this regard, Nutanix is still, even after an investment of enormous amounts of money to grow revenues, in the red. Nutanix has grown a bit faster in fiscal 2017, which ended in July, than we had expected, but its losses are also bigger than we expected, although the gap has been closing through the 2017 year and now into the first quarter of the fiscal 2018 year, which ended in October.

Before we get into these numbers, let us just say this: We have never, in all of our years of doing financial reporting, seen a company be so open about the nature of its business as Nutanix. The company’s financial presentations since it went public are thorough, clear, and interesting. (Take a look at the latest one for the first quarter of fiscal 2018 here.) If all companies behaved as Nutanix did, we would all have a better sense of what Wall Street was investing our life savings in. So we commend Nutanix for doing it right. We want and need for IT innovators to succeed economically and financially as well as technically because in doing so this is how the state of the art for IT advances. In the final analysis, someone has to pay for this innovation and people need to make livings.

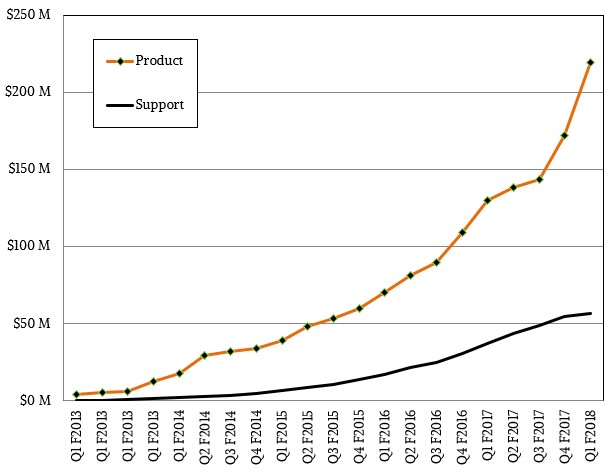

If you look at Nutanix since the beginning of its fiscal 2013, the company’s revenue and services curves certainly have been the kind we like to see, with curves sloping up and to the right as any new technology that is being increasingly embraced tends to show. We have some data reaching back into fiscal 2013, which Nutanix does not put in its current charts, which is why we drew out own curves here:

The services revenues are flattening out a bit, but product sales have accelerated in recent quarters, as you can see.

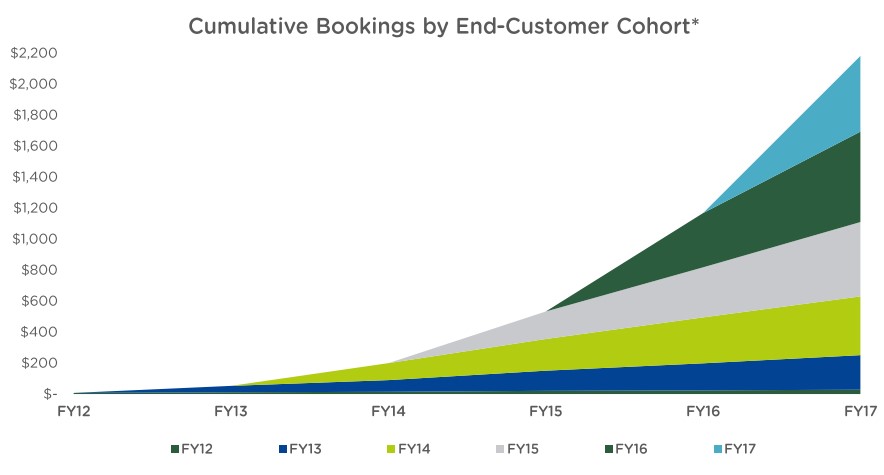

Here is another interesting chart that shows how each successive wave of customers that are new to the Nutanix stack contributes to that exponential revenue curve, capturing in a few slices the kind of data we wish we could see for other companies that attack the enterprise and rely on satisfied customers to provide an ever-heightening foundation on which to build more business. This is how it is done, right here:

When you have wave after wave of customers with steady linear growth stacking up atop each other, you get an exponential curve. Pretty, isn’t it?

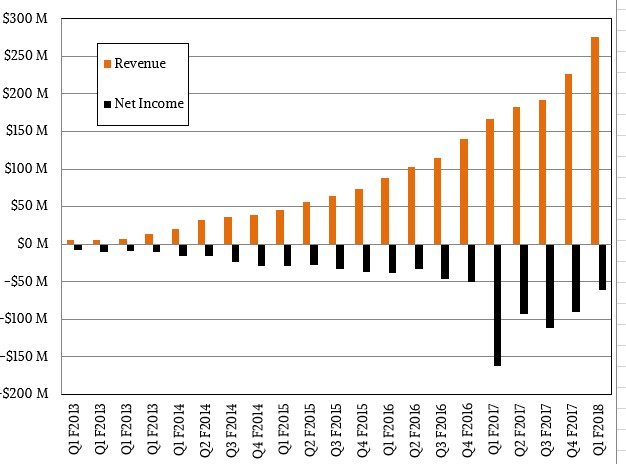

This one is not so pretty, which shows quarterly revenue and net losses over the past five and change years:

It is a very rare tech company that doesn’t have losses for many years as it builds out its product and builds up its customer base and its mindshare in the market. Nutanix certainly got a lot of mindshare in the early days of the hyperconvergence wave, and that is one of the reasons why the company has 7,813 customers and 3,009 employees, which drove $275.6 million in revenues, up 46 percent, and $315.3 million in bookings, up 32 percent compared to the prior year’s fiscal first quarter. Nutanix is now at a run rate above $1 billion a year, and if it can hold costs down and push sales a bit further, it might be at break even by the middle of next year. The company has funded a lot of development in the past several years, including a complete revamp of its storage system with the homegrown Acropolis KVM hypervisor so it could ween itself off dependence on VMware’s ESXi hypervisor (which itself is at the heart of a very pricey software stack that limits the adoption of Enterprise Computing Platform), and now it has added object storage to its virtual block and file storage. That Amazon Web Services and Microsoft Azure are giving bare metal access to VMware so its Software Defined Data Center (remember SDDC?) can run on public cloud iron is giving hope to Nutanix that it can do the same thing and thereby expand its market even more.

The other reason why Nutanix has been able to fuel this growth and hopefully get to profitability in the coming months is that it raised $393.7 million in nine rounds of venture funding and debt financing between 2009 and 2016, and then it went public in September 2016 and raised another $237.9 million through its initial public offering. In the past five years plus one quarter, as Nutanix sold $1.5 billion in hardware and software and another $392 million in support and services, it has booked cumulative losses of $936 million. This is a large amount of dough, but not unusual for a startup taking on the entire datacenter. What is unusual is that we can see it.

We think that Nutanix will continue to grow is base, have repeat customers who come back again and again and again, and eventually get to profitability. This is one reason why Wall Street has placed a value of $5.8 billion on Nutanix as we go to press. But we think that the company will likely have to do more than just give up peddling hardware to get to profitability as it tries to become the software-only company that we always thought it would be.

Down the road, we think a much bigger transition is coming, one where Enterprise Computing Platform itself has a bare metal flavor for those who don’t want anything running in virtual machines, who think of containers, not hypervisors, as the smallest unit of compute. And we think the future wants a system where compute and storage are not locked into the same scale within a node or across clusters of nodes, but rather scale independently from each other as need be. This is what Google does, and you always have to watch very carefully what Google does. For all we know, Nutanix is already on the case here, and we sure hope so.

The Balancing Act Of Training Generative AI

We learn a lot of lessons from the hyperscalers and HPC centers of the world, and one of them is that those who control their own software control their own fates. And that is precisely why all of the big hyperscalers, who want to sell AI services or embed them …

VMware Widens Its Road To The Cloud With Google Partnership

Google and VMware have announced a new element to their partnership that the two companies said will simplify cloud migrations, provide more flexibility, and help companies modernize their enterprise applications with a minimum amount of pain. An expanded partnership between VMware and Google Cloud means AWS and Dell are being …

A Tale Of Three Cloud Builders, All Seeking Dominance

While Amazon Web Services has first mover advantage when it comes to building a compute and storage cloud, it would be a mistake to believe that the division of the world’s largest online retailer can rest on its laurels. AWS has to work hard every day to make its cloud …

“And we think the future wants a system where compute and storage are not locked into the same scale within a node or across clusters of nodes, but rather scale independently from each other as need be.”

This is exactly what Datrium does with their “open-converged” infrastructure. Datrium disaggregates compute and storage performance, from resilient durable storage capacity, allowing for simple VM or Container administration and granular, low-cost, scaling of resources.

Yes, I know.

https://www.nextplatform.com/2017/08/17/stateless-compute-clustered-storage-like-hyperscaler/

In other words.. NetApp HCI also addresses this need. NetApp HCI delivers cloud-like infrastructure (consumption of compute, storage, and networking resources) in an agile, scalable, easy-to-manage four-node building block. It is designed around the foundation of SolidFire all-flash storage to deliver guaranteed application performance with mature integrated replication, efficiency, data protection, and high availability services. You can confidently deploy NetApp HCI for the edge to the core of your datacenter. Compute and Storage are decoupled.