Everyone in the IT industry likes drama, and we here at The Next Platform are no different. But it is also important as the industry in undergoing gut-wrenching transformations, as it has been for five decades now and will probably do so for a decade or two more, to keep some perspective. While the public cloud is certainly an exciting part of the IT market, it hasn’t taken over the world even if it has become the dominant metaphor that all kinds of IT – public, private, and hybrid – aspired to mimic.

That’s something, and it is important. But that is not the same thing as saying that public cloud spending dominates the collective IT budgets of the world. It most certainly does not do that, and it will very likely be a long time before it does, too, if the latest figures out of Gartner are any guide.

We got to thinking about this because Gartner put out two different sets of data during the same week. One was its estimates of infrastructure as a service, or IaaS in the cloud lingo, revenues on public clouds in 2015 and 2016. The IaaS revenue stream is for raw virtual and physical hardware – server and storage capacity and the necessary interconnection – sold on public clouds like Amazon Web Services, Microsoft Azure, Google Cloud Platform, Alibaba Cloud, IBM Bluemix (formerly SoftLayer), and across myriad service providers in the telco and cable space, such as Comcast, Verizon, AT&T, BT, Deutsche Telekom, NTT, and so forth. The platform services, or PaaS, abstract some of the hardware (virtual or physical) away and present frameworks and runtimes for applications, and the software services, or SaaS, go up one level of abstraction further and just let people use applications completely remotely. The public cloud space has other aspects to it, including the sale of advertising, which funds a lot of hyperscale activities and, in fact, underwrites the massive infrastructure the top eight hyperscalers – Google, Amazon, Microsoft, Facebook, Alibaba, Tencent, Baidu, and China Mobile – invest in each year to host services for their billions of end users, who use these services personally and for business. (That line is getting fuzzier and fuzzier all the time, isn’t it?)

Anyway, we have been tracking this IaaS spending for some time, and Gartner was gracious enough to give us the forecast going forward across the various public cloud segments, and it looks like this:

It is ironic that spending on cloud advertising globally is approaching spending on datacenter hardware outside by 2021 or so, and if you back out the hyperscalers that support their IT infrastructure with ads, it will probably hit parity sometime in 2020. That is not a dependency, just a vector.

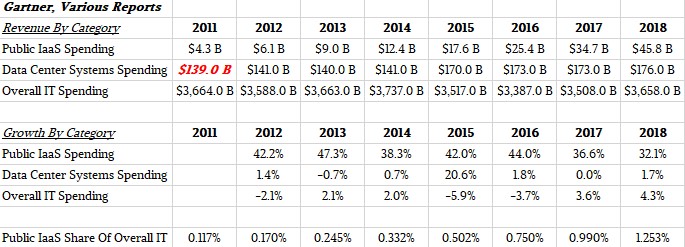

The other bit of data that Gartner put out was its projections for IT spending across various categories for 2017 and 2018. We look at this data for the current and future year as Gartner tweaks it several times each year as conditions change and the quarters actually have real numbers, and it is always intriguing. There is not as much hardware in the overall IT budget as we tend to think about it; there is a lot more application software and IT services in the budget, and the telecom hardware budget, comprising specialized switching and routing and other appliances, is absolutely huge, as is the telecom services that businesses clock up each year on various telecom and cable networks.

Gartner’s current projections are for the IT organizations the world over to consume $3.51 trillion in hardware, software and services in 2017, up 3.3 percent from the year ago period and if that doesn’t sound like a lot of growth, it is hard to move an aircraft carrier like this quickly. Of this, datacenter systems – meaning servers, storage in various forms, and the switching and routing to link it all together and to the users inside and outside of the firewall – accounted for $173 billion in aggregate revenues, up a mere 1.7 percent. This is the slow growth rate we have seen for a decade, and it would no doubt be in decline were it not for the hyperscalers and cloud builders, who buy somewhere on the order of a quarter to a third of the hardware capacity sold worldwide. (One could also reasonably argue that if it had not been for clouds and hyperscale services, enterprises would be spending more on hardware themselves.) Enterprise software in its myriad forms generates more than twice as much revenues, and in 2017 Gartner expects for this category of spending to account for a total of $354 billion worldwide, up 8.5 percent from 2016’s levels. Devices – meaning desktops, laptops, tablets, and smartphones – will bring in $664 billion in revenues this year, according to Gartner, up 5.3 percent, and IT services is an even larger segment at $913 billion, up 4 percent. The biggest chunk of dough is communications services (largely voice, data, and video) that the organizations of the world use, which Gartner says will rack up a gigantic $1.39 trillion bill. Gartner expects for the growth rates in these segments to wiggle a bit here and there, and for overall IT spending to grow by 4.3 percent to $3.66 trillion in 2018. These will probably be a tad bit optimistic, which is human nature.

Just for fun, we mapped these two sets of data against each other, using the historical data as well as the trends going out to 2018, to see how spending on public cloud infrastructure services matched up against spending on datacenter hardware and overall IT spending. Here is what it looks like:

The datacenter systems spending for 2011 is an estimate we made, not Gartner, because the company only started dicing and slicing IT spending in this fashion in 2013 and backcast it only to 2012. Obviously those providing the public cloud services at the top of this table are spending their dough to build their infrastructure in the datacenter systems spending row underneath it. If you assume that about half the spending on public cloud IaaS by customers is reinvested in hardware, and then back that out of the datacenter spending, the datacenter systems hardware business grew a little bit from 2011 through 2014 and did a big jump in 2015 and will be flat to down in 2017 and 2018. It is also hard to separate the capacity that a hyperscaler that is also a cloud operator uses for consumer apps like search engines and ad serving from capacity that is actually used for IaaS. It would be neat to see how each company breaks out in this regard. We suspect that Amazon is heavily IaaS with a smattering of PaaS and SaaS, Facebook has no cloud services as such unless you count Instagram, Google is still dominated by search and ads, and Microsoft is probably one third IaaS, one third PaaS, and one third SaaS.

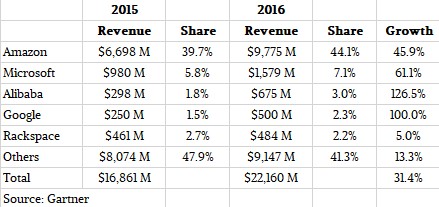

As part of the public cloud spending forecast, Gartner released its guesses for how each of the cloud providers did in 2015 and 2016, and it looks like this for the big five worldwide:

Obviously, Amazon Web Services is utterly dominating the IaaS sector that it has been setting the pace in since 2006, and Gartner thinks it is gaining revenue share in IaaS, not losing it, between 2015 and 2016. And that is despite the continual price decreases and increasingly fine granularity in pricing that the company and its peers are offering for compute and storage capacity. (As best we can figure, networking costs are going up, not down.) Microsoft, thanks to its very large base of tens of millions of Windows Server users and its embrace of Linux as a workload on its Azure cloud, is outgrowing AWS in the IaaS segment, but it is hard to see a day when Microsoft can catch AWS. Alibaba is growing faster than Google in infrastructure cloud, and is now larger, too, as reckoned by revenues. Rackspace Hosting is plugging along.

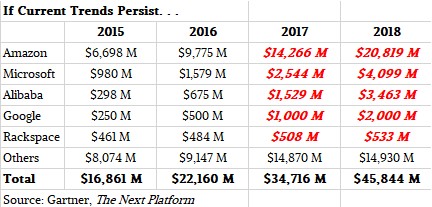

Just for fun, we took this data from Gartner and plotted out what the market might look like if current trends persisted, meaning that the big five vendors keep growing at their current paces and the IaaS sector grows as Gartner projects.

If that happens – and neither we nor Gartner are saying it will – then Amazon Web Services will take a share dip in 2017 but rebound in 2018. It took AWS the better part of ten years to push its IaaS business to $10 billion in sales, and it may only take two years to add the next $10 billion and one year to add the next $10 billion after that. When you say it like that, it brings back a thought we had several years ago: How in the hell will any cloud ever catch AWS?

What we do know is this. AWS cannot grow forever at even this pace because to do so it would be larger than all IT spending worldwide. AWS would, in effect, be IT hardware. This is what Amazon craves, of course. The current vendors – all of them – cannot keep growing at these rates and stay within the Gartner forecast, and the tightening starts in 2018 and gets worse through 2021, even if the market is four times as large. That said, there is plenty of tens of billions to go around; 88.7 tens of billions of dollars by 2021 if Gartner’s forecast pans out, in fact. But there would need to be another $50 billion in IaaS sales for these growth rates to continue, and that would basically obliterate datacenter system hardware spending by enterprises.

It could happen, but it seems unlikely.

Thank you for this refreshing view! Gives me hope that what i love to do (infrastructure architecture) will not go the way of the dinosaur.