International Business Machines has gone through so many changes in its eleven decades of existence, and it is important to remember that some days. If IBM’s recent changes are a bit bewildering, as they were in the late 1980s, the middle 1990s, and the early 2010s in particular, they are perhaps nothing compared the changes that were wrought to transform a maker of meat slicers, time clocks, and tabulating equipment derived from looms.

Yeah, and you thought turning GPUs into compute engines was a stretch.

Herman Hollerith, who graduated from Columbia University in 1879 when its engineering school was still focused on mining and laid the computing foundation that leads to the work done in specialized machines there that were created in the 1990s to run quantum chromodynamics and that lead to the BlueGene supers, is arguably the true father of IBM and got the idea of commercialized tabulating equipment going for the 1890 US Census. The United States had grown so much between 1880 and 1890 that we had our first big data explosion and needed to automate the tabulation of the Census, which is required by the Constitution.

It is with this long transition in mind that we examine the latest financial results for Big Blue, which is undergoing yet another wrenching and sometimes exasperating transformation. The most recent incarnation of IBM is slowly dying off, and the business is being pruned by the company’s top brass as soon as the leaves turn a little brown in the hopes of giving more sunshine to the new cognitive, cloud, mobile, social, and security portions of Big Blue that are growing – its so-called strategic initiatives, which in the past twelve months generated $34 billion, or 42 percent of the company’s total revenues. The new IBM is more focused on Watson analytics (a vague collection of stuff), Blockchain, IoT, and other things. But the thing to remember – to always remember – about IBM is that it is, at heart, a platform company.

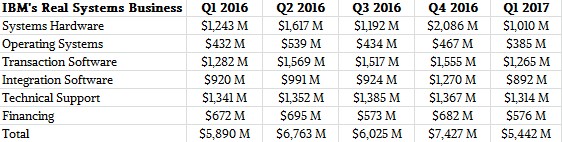

IBM’s remaining transaction processing platforms, the System z mainframe and the Power Systems boxes running Linux, AIX, and IBM i, are used by somewhere around 130,000 customers worldwide, and they generate what we often refer to as IBM’s “real” systems business. As best as we can figure after analyzing its financial results for the first quarter of 2017, this part of Big Blue generated about $5.44 billion in revenues, broken down into these categories:

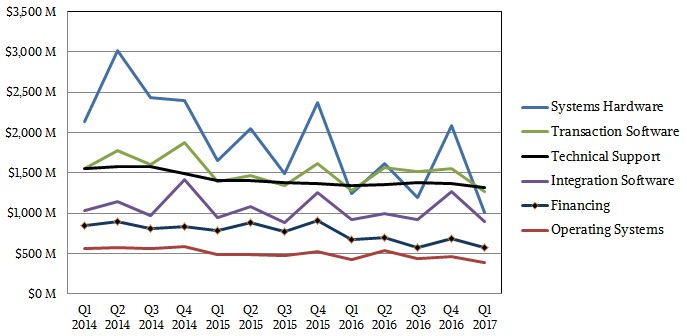

And here is what the elements of the real systems business looks like back through 2014 reflecting the new characterizations of its business that IBM set up in 2015 after selling off the System x server division to Lenovo.

The numbers in Q1 are a little lower than usual because IBM is at the tail end of both its System z13 and Power8 processor families, and everyone knows the company is launching new Power9 iron in the second half of this year and is probably fixing to move to z14 engines in its mainframes, too, although it has not said anything about this publicly. That core platform business at IBM, which includes servers, storage, some networking, operating systems, middleware, and management tools, was off 7.6 percent compared to the year-ago period, falling much faster than IBM overall, which booked $18.16 billion in sales, down 2.8 percent. IBM’s net income fell 13.1 percent to $1.75 billion in the period. (We are keeping databases separate from this core systems business because we honestly don’t know how to break this out.)

The trend lines are all pointing down, and you can easily see the big spikes in sales that happen in the fourth quarter, when budgets have to be spent, and in the second quarter, when there is often new gear available or companies have run out of gas on their systems. IBM’s operating system, database, and integration software on its mainframe and Power machinery is tied to sales but also have an annuity-like flow for mainframes. (IBM was SaaS on mainframes when it was no longer cool in the 1970s and perpetual licenses emerged, and the good news is that it does not have to deal with this jarring transition to rental pricing schemes because it never stopped selling it on a monthly basis.)

In any event, this systems business represented 30 percent of IBM’s overall sales in the first quarter of 2017, almost two points lower than a year ago and almost five points lower than three years ago. But here is the thing. We estimate that the gross profits on the real IBM systems business ranges from 55 per cent to 65 percent a quarter, depending on a lot of factors, but it has tended to stay in this range. And if you add in databases atop of the systems, that makes the numbers look even better.

This is still, despite the white knuckle declines in revenues that IBM is experiencing in its core server lines, a good business. That said, it is no fun at all for IBM to be reporting that its Systems group is under water again, with sales of System z mainframes off 40 percent and Power Systems down 27 percent ahead of the new products coming this year. Storage revenues were up 7 percent, driven by aggressive adoption of flash and despite declines in disk-based storage that has been IBM’s bread and butter since it invented the RAMAC disk drive in 1956 and made Silicon Valley the place of high tech on the West Coast. (Yeah, we know Hewlett Packard Enterprise gets credit for that because of the oscillator it invented for Walt Disney Company by founders David Packard and William Hewlett. But IBM mowed down almond groves in San Jose to build a disk drive factory for electronic tabulating machinery almost a decade before mainframes came to market, and that was high tech back then.)

That aggregate systems business, as IBM reported it, had just under $1.4 billion in external sales and another $167 million in internal sales to other units for a total of $1.56 billion in sales, down 26.1 percent, and pre-tax losses grew from $10 million a year ago to a $160 million loss this quarter. Within that, operating systems accounted for $385 million in revenues, off 11 percent, and hardware accounted for just over $1 billion, down 18.7 percent.

You can see now why IBM talks about Watson and Blockchain and the Weather Company and SaaS and other things so much, and without being terribly specific. It is a hodge-podge of stuff just like IBM was when it was incorporated as the Computing Tabulating & Recording Corporation back in 1911. Maybe the mainframe platform, and its open-ish baby brother, Power Systems, are the exception, not the norm.

Big Blue Should Start Believing In Big Iron Again

There isn’t really a systems business so much as a collection of them, all unique and all facing their own particular challenges. Among all of the current crop of vendors, IBM has been at this the longest as a free-standing, independent organization, but there are some very ancient systems businesses …

Systems Turn In A Good Year for Big Blue

You can’t turn back the hands of time, but if you are lucky enough in business, you can continue to find some modicum of relevance that outlasts your initial success and even adapt to new conditions as they inevitably and often unexpectedly change. Say what you will, but that is …

IBM Starts Walking The Hybrid Cloud And AI Talking

If Big Blue is going to talk the hybrid cloud and AI talk, as it seems to do incessantly, then the company has to walk it. And perhaps the most interesting thing that was said as part of the company’s discussion of its first quarter 2023 financial results was its …

Be the first to comment