It is week one of the new Dell Technologies, the conglomerate glued together with $60 billion from the remaining parts of the old Dell it has not sold off to raise cash to buy storage giant EMC and therefore server virtualization juggernaut VMware, which is owned mostly by EMC but remains a public company in the wake of the deal.

By adding EMC and VMware to itself and shedding its outsourcing services and software business units, Dell is becoming the largest supplier of IT gear in the world, at least by its own reckoning. You could argue that consumer PCs have nothing to do with corporate IT, and that even corporate desktops and laptops have little bearing on datacenter gear except inasmuch as these devices all tickle the datacenter gear for data and apps. But the resulting Dell will be a behemoth by any measure, with $74 billion in sales and 140,000 employees, of whom 30,000 are dedicated to customer service and support. Dell wants to take a bigger bite out of the $2 trillion core IT market, and thinks that its 118 service centers, 25 manufacturing locations, more than 40 configuration centers, reach into 180 countries worldwide, portfolio of over 20,000 patents and applications, and vast supply chain will give it the leverage to be the dominant supplier of IT gear on Earth.

To help fuel the $60 billion acquisition (it is $7 billion lower than expected) and give it focus, Dell sold off its services unit to NTT Data earlier this year, ahead of the EMC acquisition, for $3.1 billion, and shed its software division in June for around $2 billion, selling it to Francisco Partners and Elliott Management. That leaves the old Dell stripped down to PCs, servers, storage, and networking – basically back to where it was before it got IBM envy a decade ago and started acquiring software and services companies to round out its products and be more like Big Blue.

IBM shed its PC business a decade ago to Lenovo for $1.25 billion and followed suit in October 2014 when it sold off its X86 server business to the same company for $2.1 billion, and is hunkering down with Power Systems, mainframes, a collection of software, the SoftLayer cloud, and an amorphous “cognitive computing” business that seems to have every kind of database and tool in it that Big Blue sells. HPE has nothing to do with PCs any more, and in May 2016 sold off its own IT consulting and outsourcing services arm to CSC for $4 billion (with a stake worth an estimated $4.5 billion) and is in the process of selling off its software unit to Micro Focus for $8.8 billion.

Both IBM and HPE are willing to shrink their supply chains in exchange for focus and the prospect of higher profits in the datacenter. Dell, for its part, is still clinging to clients and wants to have leverage in the supply chain (particularly with processor, memory, and storage suppliers) that it believes it will not have if it exits the PC business. We will be able to tell who is right with this. If HPE starts losing share to the new Dell Technologies in servers and storage, and is able to extract more profits, too, then Dell is right. Time will tell.

What we know is that this is an expensive set of experiments that Michael Dell and his rich friends are running. (This is what money is for, of course.) To complete the EMC deal and thus take control of VMware, too, Dell Technologies and its principal backer, Silver Lake Partners, had to raise $47 billion in debt, which included $20 billion in investment-grade bonds, $3.25 billion in high yield bonds, and $14.5 in term loans; there is another $10 billion in there somewhere. This is a lot of money, by any measure. It would be interesting to know how Dell will pay it all back, including the money that was used to do the $24.9 billion leveraged buyout that took Dell private three years ago. Thus far, Dell has paid back over $5 billion in its debt from the LBO, but it will have a long way to go to pay it all back.

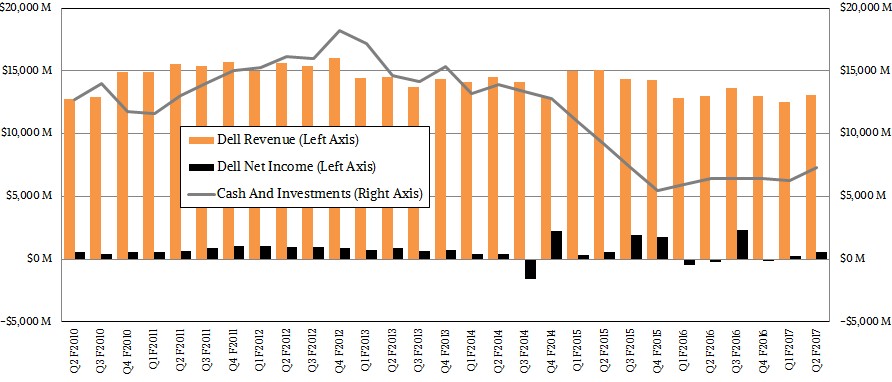

With Dell being private, but buying a public company, we got a glimpse into the financials of the company ahead of the closing of the EMC deal. We spent some time digging around through old Dell financials and the reports that Dell Technologies, the name of the new entity that combines Dell, EMC, and VMware, has been filing with the US Securities and Exchange Commission. It gives us a sense how the various Dells have fared since the Great Recession and since the LBO in October 2013. There are plenty of holes in the data, which we filled in with estimates and with the help of some Wall Street analysts who are also curious about the trends.

The short answer is that Dell peaked in the wake of the Great Recession, cresting above the $60 billion in revenue target that Michael Dell had set for the company that bears his name in the wake of the dot-com boom. Being a peddler of iron, Dell never brought a lot of cash to the bottom line – it is the nature of the game – and the advent of large public clouds and hyperscalers that Dell caters to with its servers has not helped margins at times, either. But when you are in the volume business, you cannot walk away from volumes unless the margins are extremely negative. (Sometimes, as with former custom server customer Facebook, there is nothing you can do to save the deal. Facebook wanted open source servers, and a larger ecosystem of users.)

Since disappearing behind the veil of privacy, Dell has had swings of black and red ink, with plenty of black. But speaking generally, over fiscal years 2011 through 2016 inclusive, Dell has raked in $347.2 billion and brought 5 percent of that, or about $17.5 billion, to the bottom line. This is better margins than for grocery store chain, but it is not the kind of margins that Google and Amazon Web Services are making. You can see why Dell wants to have the largest supply chain possible, because that allows aggressive pricing on components. But going after some of this business is tricky since it is not inherently profitable.

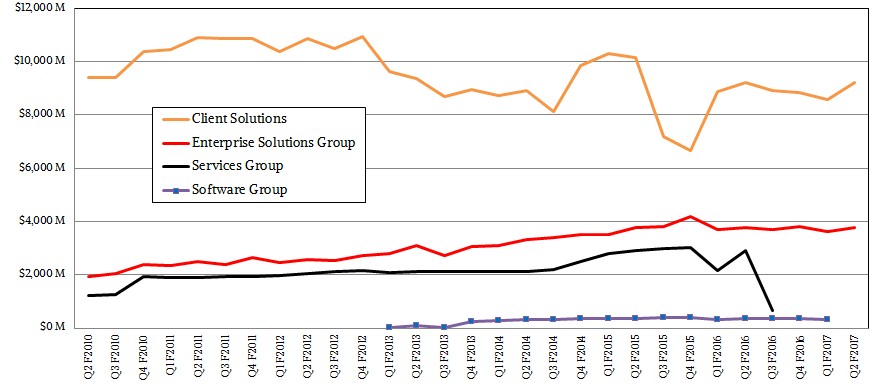

Tom Sweet, chief financial officer at Dell Technologies, said as much in a call with Wall Street analysts going over the financial results the company posted for its second quarter of fiscal 2017 ended July 29. In the quarter, Dells’ Enterprise Solutions Group, which peddles its datacenter gear, had sales of $3.78 billion, flat from the year-ago period. The core PowerEdge commercial server business declined by 6 percent year-on-year, with particular softness in China where Lenovo, Inspur, Sugon, Huawei Technologies, and others are competing hard. The modular, blade, and converged variants of PowerEdge are doing well, particularly the PowerEdge FX modular machines, which had triple digit growth. But some small and medium businesses are moving to the cloud and therefore not buying gear. Sweet said that he expected some customers would ricochet back and end up with hybrid gear in their closets and datacenters and capacity on the public cloud, but this remains to be seen.

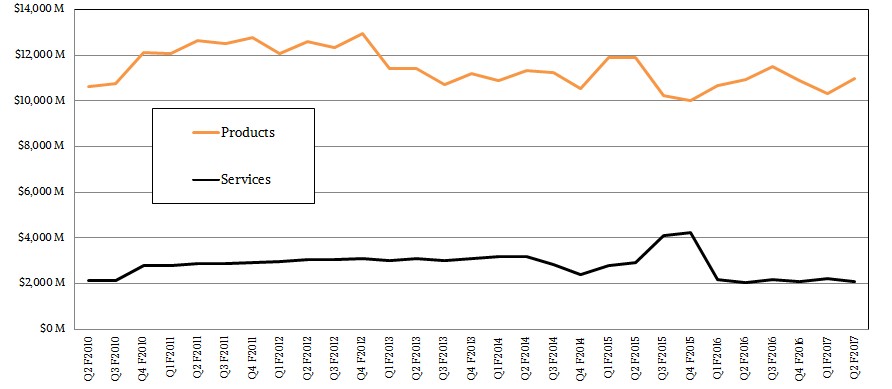

The custom server business, which includes machines sold to hyperscalers, accounted for about 10 percent of revenues in the quarter, and the Data Center Solutions (DCS) unit that sells explicitly to hyperscalers saw growth in the middle 30 percent range and the Datacenter Scalable Solutions unit, which sells to smaller service providers and enterprises that need semi-custom gear, grew in the low 30 percent range. Within Dell’s Enterprise Solutions Group, revenues for servers and networking grew 1 point to $3.24 billion and storage fell by 2.7 percent to $542 million. Dell’s storage business, even after big acquisitions, has not grown, but it does do well in hyperconverged storage. (It is not clear where this gets categorized, as either storage or servers.)

Dell does not give out operating income for its product categories, but Sweet said that generally speaking the hyperscaler sales, which were obviously up in the quarter and driven by some big deals, have lower margins, but not always. In the second quarter in particular, Sweet said that the DCS team was able to keep revenue and costs in line and pricing held up. Margins on storage were also up even as revenues were down. For the entire Enterprise Solutions Group at Dell, operating income was up 7.1 percent to $300 million. This operating income was 8 percent of revenue, compared to the $484 million in operating income from Dell’s Client Solutions Group, which had $9.22 billion in revenues. Revenues were flat for the quarter, and the operating income for the PC business works out to 5.2 percent of revenues.

The baseline Dell is, all things considered, pretty stable from the numbers we could put together, and adding VMware and EMC to its portfolio, once some costs are eliminated, will probably result in more cross selling and more profits. VMware is already expecting to get an incremental $1 billion in revenues from the Dell partnership. (We are not sure if it means annually, but that is the only number that makes sense.) The issue we see is that the effect of a tight partnership between Dell and VMware might mean server competitors look elsewhere for allies, such as Red Hat and Microsoft, possibly Canonical, and any number of upstarts peddling containerized platform clouds. Dell may keep VMware at arm’s length as a public company, but it will still have hold of it, and unlike EMC, until it recently took over VCE, has not been a server provider. The convergence of servers and storage was pushing EMC in that direction, and in contention with Dell and other suppliers. A clash seems inevitable, as was the case when Cisco Systems entered the server space back in 2009 when servers and networking were converging.

Stacking Up The Next Dell Platforms, Plural

In unveiling of the Dell Technologies conglomerate this week by the company’s top brass, it did not provide financials for the combined Dell, EMC, and VMware, above and beyond the statement that it will have $74 billion in annual revenues and be the largest pure-play IT supplier and certainly the largest privately held IT supplier. The combined companies have around $4.5 billion in annual research and development spending, according to Michael Dell, and it is arguable if this is enough for a company with such high aspirations. But there is no question that Dell will have immense reach, with well north of 500,000 customers since VMware has that many by itself, and its supply chain will indeed be large and something that it can leverage. And as Dell, the man, pointed out on the call, Dell’s debt payments for its LBO and the EMC acquisition will be lower than what its competitors shell out for share buybacks.

In launching his embiggened company, Dell said that we are at the cusp of a major shift in IT, and that this new company was better positioned to ride up the tsunamis caused by that shift. (OK, he did not literally say that, but it is nice image, isn’t it?) And, he reminded Wall Street, customers, and competitors that he was thinking long term – something a private company can do.

“We believe that humanity is standing at the very beginning of the next industrial revolution, the next quantum leap in human progress,” Dell said. “Digital transformation is real and it is radical beyond anything we have ever seen. And I am not just talking about digital transformation of business, but the entire physical world. As the marginal cost of making something intelligent approaches zero, the number of objects and devices is growing exponentially. By 2031, the number of connected devices and objects will grow from 8 billion today to 200 billion or more – about 25X the number of people on the planet – and it will create massive new sources of information. Using that information, especially in real-time, provides better insight to build a better world. That is the challenge of our generation.”

Having missed the smartphone and the public cloud, both of which Dell tried to make but could not afford to do, the company is going to try to make it up in other areas. Intel missed the smartphone and do did Microsoft, and both are trying to make it up in other areas; Microsoft, with a lot of help from Dell, has managed to get a solid number two place behind Amazon Web Services in the public cloud and it has a good opportunity to pull even some day thanks to that vast Windows Server installed base.

Dell said that he was thinking about how to pursue opportunities beyond automating industrial processes, which is what a lot of IT does, including augmented reality and deep learning and the new kinds and levels of engagement these will engender.

“Thirty years ago, I was building PCs in my dorm room at the University of Texas,” Dell recalled of his initial startup operation. “Now, I didn’t know where it would all go, but I believed personally that information technology represented a revolutionary advancement in human progress that would change the world for the better. And in the last three decades, we have seen information technology driven into the world deeper than ever before. We have seen information and access to technology democratized – new industries, new business models, and new ideas that bring opportunity to every corner of the globe. And this is just the beginning.”

Before we get to that far-away future where drones and self-driving cars and robots service our every whim (do we really want this?), Dell has some practical platform stacking that it needs to do to help customers create the backend systems that will manage the deluge of data coming off tens to hundreds of billions of devices. (We think 2031 is pretty far away for predicting any future, but Michael Dell is looking at retirement age there. And he is thinking big.)

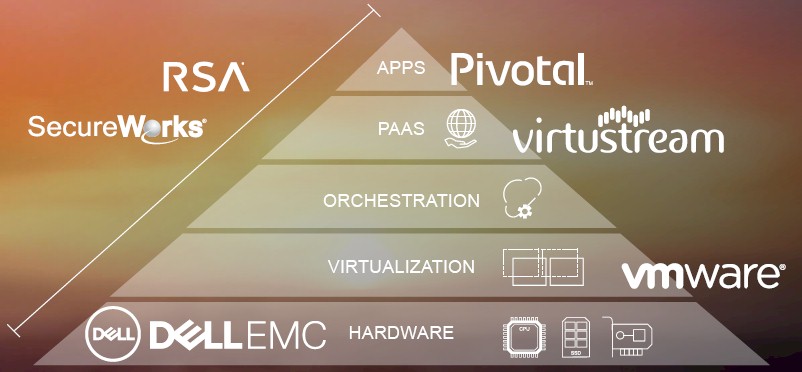

The stack looks something like this at the moment:

We think should be a rectangular block diagram to show the equal importance of each layer, but we digress. The orchestration layer is something that Dell has invested in already, and VMware has aspirations here even if the chart doesn’t say that and Dell’s partners, such as Red Hat and Microsoft, also have goals here, as do the OpenStack, Mesos, and Kubernetes communities. There is a lot of stuff that can hang here.

David Goulden, who will be president of the combined Dell and EMC Infrastructure Solutions Group, didn’t say all that much unexpected during the announcement and certainly did not detail any product line rationalizations that will no doubt be taking place over the long haul of many years. But Goulden did present this image of the Dell Technologies opportunity:

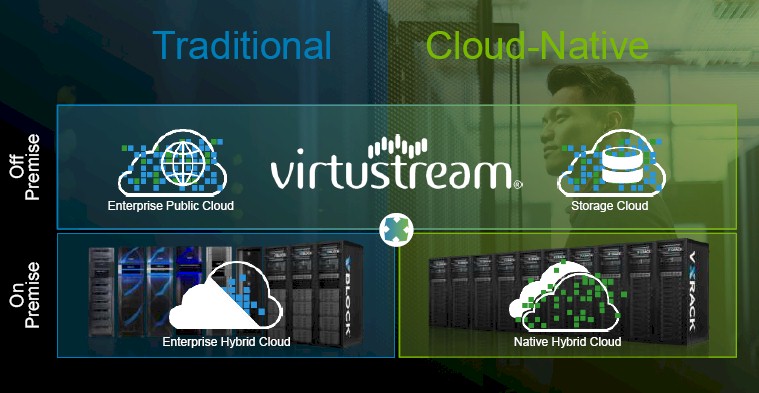

For traditional IT customers, which have scale-up applications that are often these days virtualized, the stack will be servers and storage running the VMware vSphere platform. This is a very general statement, as you know, since vSphere is offered as a substrate running the OpenStack cloud controller as well as an integrated Docker container environment. (We discussed the latest developments with vSphere Integrated OpenStack and vSphere Integrated Containers in the past week.) VMware thinks it can get public clouds to adopt its substrate as well, and certainly its vCloud Air Network partners will do this, but the major public clouds – Amazon Web Services, Microsoft Azure, and Google Cloud Platform – have their own substrates. So it is hard to imagine how this is going to work. The images showed the vBlock infrastructure from EMC, which took control of the VCE partnership a while back, but clearly Dell will have to rationalize is now quite diverse server base.

For so-called cloud native applications, which have a much lighter virtualization substrate and which are a mix of containers running on platform clouds, Dell will be emphasizing its Pivotal Cloud Foundry platform cloud underpinned by its Photon Platform container environment, which is derived from vSphere components but which is very different. The VxRACK converged systems are shown underpinning this native hybrid cloud, and again Dell is making the assumption that the stuff in the corporate datacenter mirrors that in the public cloud. This seems unlikely, and as we have said, it is far more likely that customers will press the public clouds of their choice to give them private versions of their stacks. Dell can get a piece of the Azure Stack action with Microsoft and partner with IBM SoftLayer as it has done, but it is hard to imagine how the company might forge private slices of the Google and Amazon public clouds.

Dell is pitching the Virtustream cloud as a kind of glue to cross connect private and public clouds, and while this is successful to a certain extent right now, that is merely because private versions of AWS, Azure, and Cloud Platform are not available.

There is a lot to chew on with this Dell Technologies behemoth, which is in a way getting back to its infrastructure roots even though some of it is now bits and not metal. Now that the deal is done, we will be stepping through it in some detail. There will be lots of work to figure out what Dell, EMC, and VMware products to push – and what server and storage products not to – and the situation is far more complex than the presentation that Dell, Sweet, and Goulden presented. Pipe up with any thoughts you might have.

Be the first to comment