If there has been a time when the IT industry was not being roiled by multiple transitions, we can’t remember it. More than two decades ago for sure.

Getting a handle on how these transitions are playing out in the market is tricky because the big players in the IT sector are constantly moving from legacy products to new-fangled ones and dealing with competitive pressures as well as reorganizations aimed at better capturing opportunities.

But, once a quarter, all of the big public companies get their grades from Wall Street and now that it is no longer affiliated with a PC and printer business, Hewlett-Packard Enterprise is a pretty good proxy for what is going on out there in the datacenters of the world. That is why The Next Platform watches HPE so carefully, as well as IBM, Cisco Systems, Supermicro, Cray, SGI, Microsoft, VMware, and a number of other publicly traded vendors. Dell is also a bellwether and will be even moreso once it completes its $67 billion acquisition of storage and virtualization giant EMC later this year, but unfortunately for us, Dell is now private and we have very little idea of how the company is doing aside from the guesses that market researchers like IDC and Gartner make each quarter for segments of the IT market.

In the financial analysis that we do, we think it is relevant to track the ups and downs of companies since the recovery from the Great Recession started back in 2009. The world is different since then, as it always is in the IT sector after a recession. Long before HPE was spun out as an enterprise-focused company, we have been tracking the elements that make up the enterprise portion of this business, and to its credit, HP and now HPE have always provided detailed revenue and operating profit figures for key parts of its business that allows such a thorough and consistent analysis. The one big change now that HPE is an independent company is that it has consolidated its Industry Standard Servers group, which peddles entry and midrange X86 iron, and its Business Critical Systems group, which sells Itanium machines running HP-UX or OpenVMS as well as high-end Xeon machines bearing the Superdome X label, into a single Servers category. The Business Critical Systems part of HPE has been in decline for years, although it was seeing some uplift in recent quarters thanks to the Superdome X iron.

Because of the increasing dependence on sales out of the United States and the rising US dollar in the face of economic uncertainty in China, Russia, and other parts of the world, the multinational IT suppliers that are based here often provide some sense of how sales for different products are doing in different regions in constant currency – a practice that IBM started doing two decades ago and that others have followed, particularly after the Great Recession was over. HPE is now doing it, and this practice gives us all a sense of how the underlying business lines are doing without the ups and downs of foreign exchange. That said, the real money for these companies is booked in dollars, and ultimately, everyone wants their IT supplier to be healthy in actual dollars, not just constant currency ones.

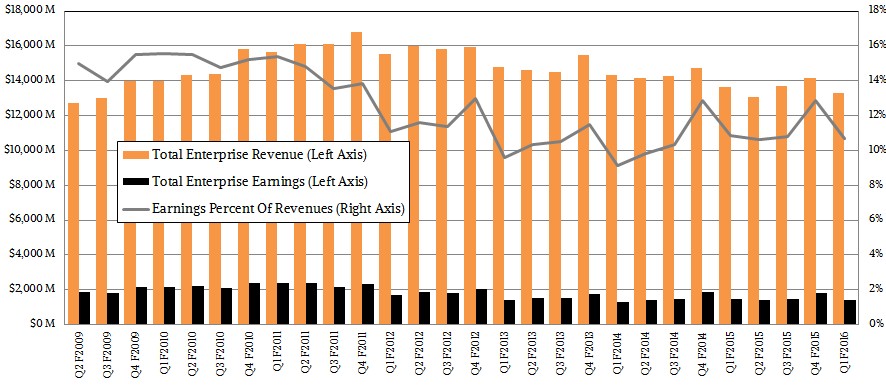

To grow, companies have to eat market share sufficient to mitigate against currency effects. This is a serious challenge, and not just for HPE, which actually turned in better numbers than Wall Street expected, with revenues of $12.72 billion and net income of $267 million in the first quarter of fiscal 2016 ended on January 31. Take a look at the trends:

HPE’s net income was hurt by reorganization and stock-based compensation costs that accompanied the spinoff and by foreign exchange issues, but in the chart above, we are comparing apples-to-apples across time with operating earnings for the enterprise parts of the former HP and the new HPE.

As you can see, the enterprise business has been trending down as a unit since recovering after the Great Recession, and it is due to many different transitions. Legacy server and storage platforms collapsed faster than the company was able to replace them with newer products, and we think HPE is also subject to more intense competition in its core server, storage, and switching markets on top of these transition issues. To its credit, it has made the acquisitions in storage and networking to remain relevant and has continued to be an innovator in servers, so in this regard it is doing better than some of its peers. The company has had issues with its enterprise services business almost from the moment when it bought EDS, and is no different in its struggles that IBM with its Global Services behemoth. The fact of the matter is that the nature of the services business is changing and in such a business, which is highly dependent on people and their skills, it is difficult to turn on a dime and extract profits.

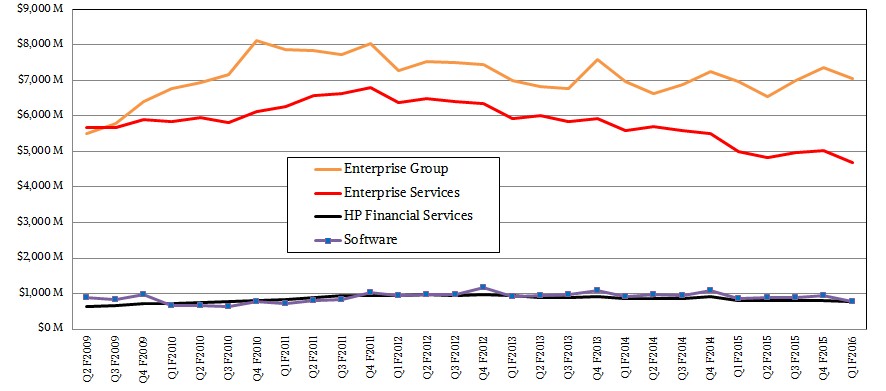

Despite all of the market issues and technology transitions, the four core parts of the HPE business have remained remarkably stable since the recession was over. Enterprise Group, which sells the key server, storage, and switching hardware that most people know the HPE name from, has found a relatively stable revenue level that seems to hold at around $7 billion a quarter. Enterprise Services, which includes tech support, systems integration, outsourcing, and other activities, continues to creep down and it is hard to say where it will end. HPE is committed to this business being profitable. The Software and Financial Services parts of HPE are steady at just under $1 billion per quarter, with a little wiggling here and there.

In the fiscal first quarter, HPE generated just a tad over $7 billion from its Enterprise Group, up 1 percent year-on-year (up 7 percent at constant currency), and had an operating profit of $944 million, down 10.8 percent. Enterprise Services posted sales of $4.69 billion, down 6.1 percent, with an operating profit of $238 million, up 58.7 percent and clearly headed in the right direction. Software revenues fell 10.3 percent to $780 million and Financial Services revenues were down 3.4 percent to $776 million. (HPE sold $572 million worth of stuff between its various units, which is taken out to show the top line revenue.)

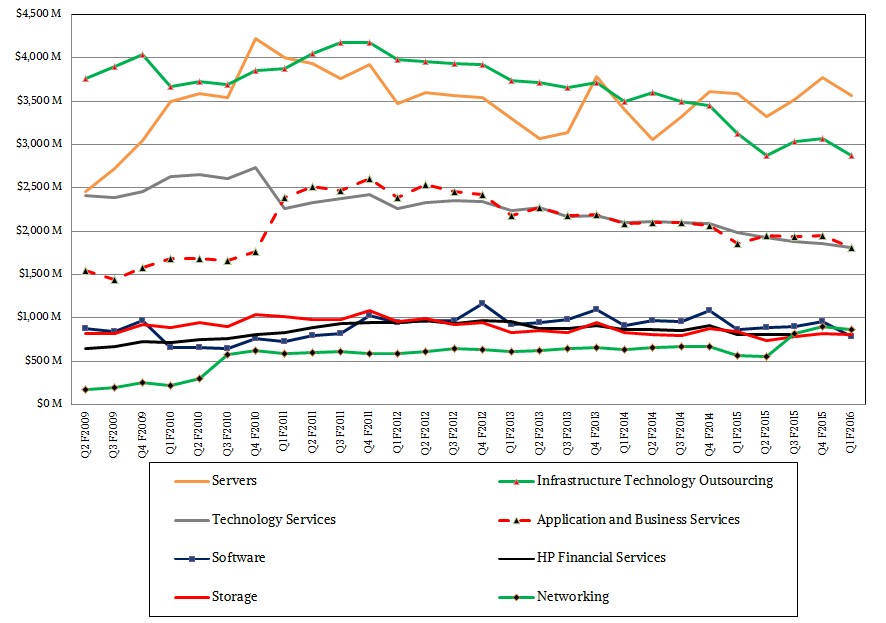

Drilling down into the individual units within Enterprise Group and Enterprise Services gives you these trend lines:

The crucial Servers unit at HP brought in $3.57 billion in revenues, down 1 percent but up 5 percent at constant currency according to Meg Whitman, HPE’s CEO who went over the numbers with Wall Street analysts.

Server sales in the first quarter were driven by the large appetites of HPE’s largest customers and channel partners, and sales in Europe and Asia were strong, according to HPE’s chief financial officer, Tim Stonesifer. Server sales in the America region were under pressure, particularly at the end of the quarter – a slowdown that rival Cisco Systems also experienced.

“We did a great job I think in grabbing share from Lenovo, when those servers moved from IBM,” Whitman said on the call. “And we are all over this Dell-EMC opportunity. So in a flat to declining market, which core servers probably are at least over the next five years, we have to gain share. But there are real pockets of growth in the market as well. And in high performance computing, we are like the last man standing there and we are investing in HPC and it’s a core competency for the company.”

Whitman added that the company’s HPC was now at a $1 billion annualized run rate and that high-end, mission critical Superdome X servers saw double digit growth. HPE’s core networking business was up in the double-digits, too, and adding in its Aruba Networks acquisition revenues rose 54 percent as reported and 62 percent in constant currency.

Storage revenues across flash, disk, and tape products lines came to $810 million, down 3 percent as reported but up 3 percent at constant currency. The company’s so-called “converged storage” lines, by which it means new stuff not legacy NAS and SAN arrays that originated in HP or Compaq way back in the day, had a 17 percent boost in the first quarter (in constant currency) and the 3PAR line had its highest level of sales yet, with triple-digit revenue growth for all-flash variants of the line and what Whitman says was three times the growth rate for the industry at large.

Whitman said that HPE is planning on making two key infrastructure announcements later this month. The first is a refreshed server lineup that will include what she called “persistent memory” that was invented by HPE and that is “a key milestone” on the company’s roadmap towards delivering The Machine. (Which we have written extensively about in the past year.) We suspect that this persistent memory will be coupled with ProLiant servers employing Intel’s forthcoming “Broadwell” Xeon E5 v4 processors, which are expected to launch soon.

The other big announcement is a homegrown hyperconverged server-storage hybrid that Whitman said would be based on its ProLiant server line and would come in at 20 percent cheaper than alternatives Nutanix, which is the revenue leader in the hyperconverged area. HPE has been selling virtual SAN software for a long time, which it got through its acquisition of LeftHand Networks and which it has been peddling as the StoreVirtual VSA; it is likely that this is the storage foundation of this hinted hyperconverged product that Whitman is referring to.

Whatever the case, you know for sure that The Next Platform will be all over it.

European Weather Center Breaks Tradition With Upcoming Supercomputer

Weather forecasting in Europe is going to get a big boost later this year when the European Centre for Medium-Range Weather Forecasts (ECMWF) installs its next-generation supercomputer. This week, the center announced it had signed a four-year deal with Atos worth over €80 million ($89 million) to deploy and support …

Lawrence Livermore’s “El Capitan” To Take AMD’s Instinct APU Mainstream

In March 2020, when Lawrence Livermore National Laboratory announced the exascale “El Capitan” supercomputer contract had been awarded to system builder Hewlett Packard Enterprise, which was also kicking in its “Rosetta” Slingshot 11 interconnect and which was tapping future CPU and GPU compute engines from AMD, the HPC center was …

Enterprise Storage Has To Evolve In A Changing Data Landscape

Enterprises continue to be inundated with data that needs to be collected, stored, moved, processed and analyzed, and the view down the road shows no let up. In 2025, there will be 175 zettabytes of data created, according to IDC – up from 59 zettabytes last year. In addition, the …

Be the first to comment