IBM made no bones about it. After divesting itself of its System x server business, which it sold off to Lenovo Group, and its Microelectronics chip making division, which Big Blue paid Globalfoundries to take, the company said that 2015 would be a year of transition on many fronts. There is no question about that, and Big Blue’s latest financial results bear this out.

While IBM expends a lot of corporate oxygen talking about social, mobile, analytics, and cloud, deep down inside, even after all of the changes, the company remains what its full name – International Business Machines – has always proclaimed: a systems company. It is important to remember that as IBM goes through the changes and tries to adapt, once again, to a radically altered data processing market.

Before the divestiture of the System x business, IBM probably had somewhere between 400,000 and 500,000 enterprise customers – on the same order of magnitude as software and systems rival Oracle and partner and sometimes rival VMware. And while AWS boasts that it has over 1 million users on its public cloud, we all know that a lot of these are independent developers, not corporations, and the comparison is not exactly fair. The SoftLayer cloud has in the range of 25,000 companies using its server fleet, which should be at just under 200,000 machines by the end of the year by our estimates.

It is ironic that IBM is talking up a cloud that is based on X86 servers while trying to convince the world that Power-based systems are better than X86 iron for lots of workloads; IBM doesn’t have to push the System z mainframe so much as keep it on a Moore’s Law curve of its own and keep the price/performance improving to keep those customers in the mainframe fold. We hesitate to say to keep those customers happy, considering how expensive mainframes and their software is relative to other platforms. But the fact remains that with well over $1 trillion in software investments on mainframes, the 6,000 or so enterprises that use IBM mainframes are the die-hards who will not move off The Next Platform because of the cost and disruption this would cause to their businesses. IBM can count on a certain level of money from the System z line that it just cannot with the Power Systems line.

Over time, as Power-based systems get commoditized by IBM’s partners in the OpenPower Foundation and more of the Linux stack moves over to Power-based iron, we can expect for IBM to eventually deploy lots of Power server nodes in its SoftLayer cloud. The idea is to make Power machines look as much like X86 iron as possible, as Rackspace Hosting is doing with its Power8-based “Barreleye” server and as Google is examining doing with its own search and advertising workloads. IBM wants to sell raw capacity for customers to run their own applications and also has a set of its own applications – including Watson cognitive computing services – that it wants to deploy on its cloud, allowing it to carve out a profitable niche against Amazon Web Services, Microsoft Azure, and Google Cloud Platform. But it is important to remember that IBM is still a systems company, one that sells top-to-bottom platforms that enterprises, government agencies, and other organizations rely on to run themselves.

It will take some time to get there, and IBM has already spent a lot of time figuring out what to do and then implementing its transition plan; the second quarter marks the 13th straight quarter of revenue declines for Big Blue, and Wall Street is not patient about such things even if Warren Buffett, perhaps IBM’s largest shareholder, apparently is.

In the quarter ended in June, IBM’s revenues decreased by 13.7 percent to $20.81 billion. In a conference call with Wall Street analysts, Martin Schroeter, IBM’s chief financial officer, said that the strengthening of the US dollar against other currencies in the world (particularly the euro) shaved 9 points off of the company’s revenue growth and the divestiture of the System x and Microelectronics units were nearly another 4 points, so absent the currency pressure IBM’s revenues were actually only down a point or so.

On the strategic imperatives front, IBM is being very generous with itself in terms of categorizations. Schroeter said that these key areas, which represented about 20 percent of IBM’s revenues in 2014, grew at more than 30 percent in the second quarter, a similar rate to the first quarter. Schroeter reiterated IBM’s plan was to grow these businesses – again, that is mobile, social, analytics, and cloud – such that by 2018 they would represent 40 percent of revenues at the company. On the analytics front, IBM said that it bad $17 billion in revenues in 2014, and that this business grew at more than 20 percent in the second quarter, which Schroeter said was well above market rates. He added that the growth was due to sales of services from its Global Services behemoth and from sales of shiny new System z13 and Power8 iron that was bought by customers to specifically run analytics workloads.

On the cloud front, Schroeter said that IBM’s sales were up 70 percent in the first half of the year and now had an annual run rate of $8.7 billion; that is $1 billion higher than the run rate as the first quarter closed in March. Within this cloud revenue stream, $4.5 billion of it comes from applications that IBM is running on its SoftLayer cloud and other infrastructure on behalf of customers. (It would be nice to see an actual breakdown between true cloud infrastructure and application sales and traditional outsourcing. IBM does not provide such details.) Sales of IBM hardware and software to drive social applications rose by more than 40 percent, and wares for mobile applications were up by a factor of four, year on year, in the second quarter.

But with all of this growth, it was still not enough to keep IBM’s top and bottom line from sinking. IBM’s so-called growth markets are flat and the BRIC countries that help it grow so much in the past decade – as they did for many IT suppliers – have been crunched in recent quarters for their own reasons. The market in China declined 25 percent for IBM in Q2, in large part because Chinese companies and government agencies want to buy indigenous technology more and more. India had modest growth, but Brazil declined 16 percent.

People seem to be a bit perplexed that IBM’s Software Group, which provides a large portion of the company’s profits, is in decline, but we are not. The shift from licensed software to cloud subscriptions is putting all enterprise software suppliers under pressure, and moreover, IBM no longer has its System x business to drag along sales of operating systems, middleware, databases, and other software. (We are not saying that Lenovo is somehow boycotting IBM software, but rather there is not a single company trying to push a single stack on System x as there was last year.) Including internal sales to other IBM groups and external sales to customers, IBM’s Software Group had $6.6 billion in sales, down 10.1 percent, and posted a pre-tax income of $2.27 billion, down 15.3 percent. Some of that profit hit is due to investments in the Bluemix variant of the Cloud Foundry platform cloud and Watson analytics applications, which is now deployed in 30 countries and 20 different industries.

IBM’s Systems Hardware business – again including external sales to channel partners and customers as well as internal sales to other groups within IBM – generated $2.16 billion in revenues, down 32.4 percent as reported but up 5 percent if you take out the effect of the System x divestiture and currency translation into US dollars for IBM’s books. IBM’s System z mainframe business had a 15 percent bump if you look at it through those rose-colored glasses, and the Power Systems business, thanks to sales of scale-out Power8 machines as well as midrange and high-end scale-up Power8 systems that are newer to the market, had a 5 percent increase in the second quarter. IBM’s storage business, which includes disk array, flash array, and tape array and library sales, declined by 4 percent. FlashSystem all-flash arrays had “strong growth,” according to Schroeter, but the high-end disk array business had “continued weakness.”

As we have pointed out before, IBM carved up its financial reporting back in the dot-com era to reflect the fact that it was trying to position itself as a provider of software and services that were not necessarily tied to its own systems. We think that IBM should talk about its own systems business as a whole and then talk about its cloud as a unique thing and also separate out its software and services that are deployed on other systems. Our point is that, even after the divestiture of the System x division to Lenovo, IBM has a quite large and quite profitable systems business.

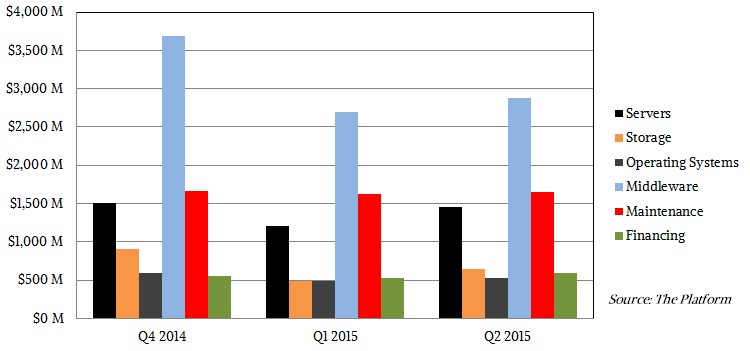

To help get a sense of that systems business, we have diced and sliced IBM’s financials since the divestitures to try to understand how large it is and what it is comprised of. Take a look:

IBM provides quarterly statistics that allow us to figure out how much revenue it is getting for servers, storage, and operating systems, which are the key components of its systems.

Trying to figure out how much of IBM’s middleware runs on its own systems is a bit tricky. As a pessimistic estimate, we think that the Other Middleware in its financial presentations is almost exclusively sold on mainframe and Power Systems machines and that 40 percent of its other Key Branded Middleware, as IBM calls it, is deployed on Power and z iron. (Another 30 percent ends up on System x iron perhaps, and the remaining 30 percent on other systems, we would guess.) In the chart above, we are attributing all of IBM’s maintenance revenues to its own iron, and half of the financing it does (which is a very lucrative business with gross margins approaching 50 percent).

Add it all up, and that real IBM systems business weighed in at $7.75 billion in the second quarter, accounting for more than 37 percent of its total sales and we would guess well above 50 percent of its profits.

Why IBM doesn’t talk about itself this way is a mystery to us.

Big Blue Can Still Catch The AI Wave If It Hurries

It has been two and a half decades since we have seen a rapidly expanding universe of a new kind of compute that rivals the current generative AI boom. Back then, with the Dot Com Boom, companies wrapped a layer of Internet networking and Web protocols around their prettified applications …

IBM Leverages Cloud To Push The Encryption Envelope

The rapid adoption by enterprises of hybrid cloud and multicloud environments along with the rise of the Internet of Things, a much more remote workforce and other trends that have contributed to the increasingly distributed nature of modern IT has put the vast amounts of data that is being generated …

The Horizontal And Vertical Platforms Of Big Blue

At its heart, and until the day it dies, if a corporation ever really dies, International Business Machines will be a platform company, no matter how much it tries to bamboozle itself or Wall Street or Main Street otherwise. And sometimes, when we examine Big Blue’s quarterly financial results, it …

Be the first to comment