The central banks of the world, led by the European Central Bank and the US Federal Reserve, want to curb inflation and they are willing to cause a small recession or at least get very close to one to shock us all into controlling the acquisitive habits we developed during the lockdowns of the early years of the coronavirus pandemic.

As we have previously reported, IT spending forecasts are consequently coming down for 2023 even as inflation is eating into the collective IT budgets for the world and making spending look bigger than what it really is. And now, the jitters are showing up in the current and future numbers from IT hardware suppliers and OEM juggernauts Dell and Hewlett Packard Enterprise.

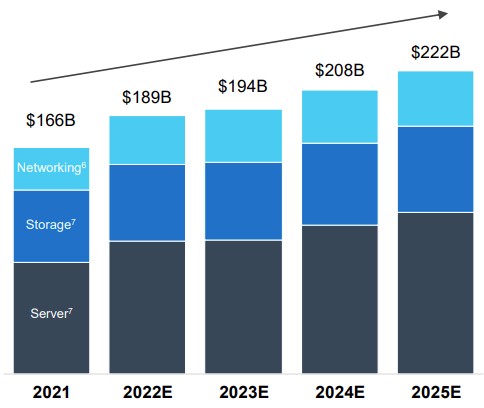

To set the stage for these numbers and the ones we will do as 2023 progresses and goes into 2024, let us take a look at the forecasts for server, storage, and networking spending that Dell talked about in its most recent financial report. Take a look:

The networking spending forecasts were done in the third quarter of last year from Dell’Oro and the server and storage spending forecasts are from IDC also done in the third quarter of 2022. So they are a little stale, but not too bad. As you can see, the prognosis for growth for servers and storage was not very good, and even networking growth is projected to be more subdued in 2023 than it was in the jump from 2021 to 2022. This is going to be a tough year for all of the OEMs, and particularly with Lenovo growing fast and getting its share of server and storage sales into some of the hyperscalers and cloud builders in China and Supermicro doing likewise in the United States. Both take on Dell and HPE daily and have to also contend with Inspur throughout Asia and Cisco Systems in North America and Europe.

This is a tough business, whether you are an OEM that is trying to build many SKUs for a wide variety of customers who have modest to high volumes or you are an ODM that is building to order custom machinery from the world’s largest hyperscalers and cloud builders. We need around 15 million servers this year, give or take, and someone has to build them. All we can tell you for sure is that no one but the CPU makers, the flash makers, the memory makers, and the network interface makers are going to be getting much in the way from profits from the whole effort. The OEMs and ODMs sure as hell don’t bring much to the bottom line compared to, say, Cisco Systems or Arista Networks in datacenter switching. This server and storage infrastructure is absolutely vital to the global economy and the functioning of modern society, but you just can’t make a lot of money doing it.

Having said all of that, let’s dive first into Dell’s latest financial results because it has a bigger business in the datacenter and it is also jumpier about its forecasts for 2023 compared to HPE (at least so far).

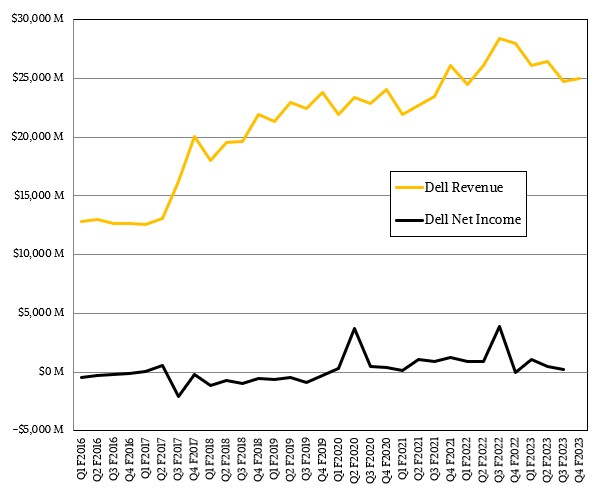

In the fourth quarter of its fiscal 2023 ended on February 3, Dell reported revenues of $25.04 billion, down 10.5 percent, with a net income of $606 million. That net income was a heck of a lot better than the $1 million – that is not a typo – it reported in the year ago quarter, and if Dell’s profitability was predictable at all, we would compare against the average and it would be meaningful. But honestly, the level of net income to revenue is all over the place. What we can say is that at 2.4 percent of revenue, that net income reported in Q4 F2023 is a lot higher than the 0.6 percent average over the past 32 quarters in its most recent financial reporting segments that we track. But seriously, if you think you can predict Dell’s profitability from the outside, we wish you luck.

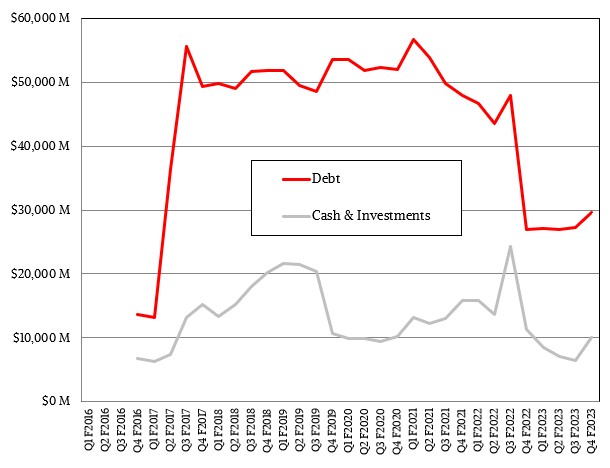

Because of the huge debts that Dell ran up to do its acquisitions of EMC and VMware, we have tracked Dell’s cash and debts separately from its revenue and income. (We usually put it all on one chart.)

Now that it has spun off VMware to wall street, the Dell has cut its debt levels in half, but in the past year it has also spent to $14.11 billion of its cash to pay down debts, shell out $3.8 billion in share repurchases and dividends, and invest in the company. It has a much more sane $29.59 billion in debt against $10.13 billion in cash. (We track cash because it shows a degree of maneuvering room in the IT market to invest in strategies and make acquisitions.)

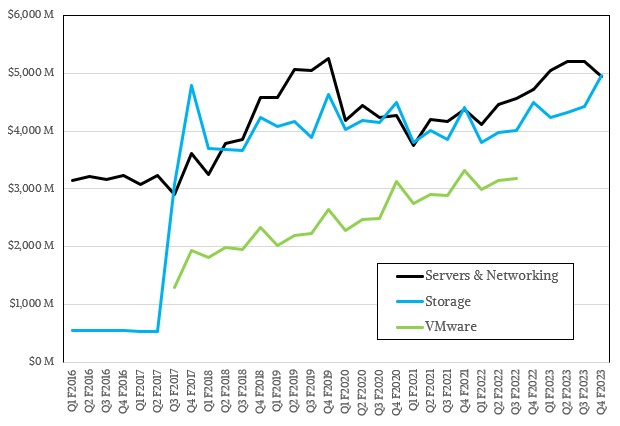

In the February quarter, Dell did pretty well in peddling servers, storage, and networking, with $9.91 billion in sales in its Infrastructure Services Group, up 7.4 percent, and an operating income of $1.54 billion, up 40 percent. In fact, this is the best quarter in IT infrastructure that Dell has ever posted both for revenues and operating income (excluding VMware when it owned it).

Within ISG, servers and networking comprised $4.94 billion in sales, up 4.7 percent, and storage comprised $4.97 billion, up 10.4 percent. Chuck Whitten, co-chief operating officer at Dell, said on the call with Wall Street analysts that Dell has gained 9 points of market share in servers in the past decade (17.4 percent in Q3 2022) and in the wake of the EMC acquisition is by far the largest supplier of external storage (28 percent share, and larger than the next three players added together).

Whitten did say that it was a “challenging server demand environment” in the quarter, but Dell optimized its server shipments with strong attach rates for accelerators and other features and also pushed up the ASPs to maximize revenues (presumably with higher-end CPU SKUs, fatter memory and flash, accelerators, and fast network cards).

Because the nuance is important, we are quoting Whitten in full about the current IT spending environment.

“The broad caution in the IT spending environment that we started calling out in Q2 persists as customers continue to scrutinize every dollar in the current macro environment,” Whitten explained. “Exiting fiscal year 2023, we saw select growth in verticals like financial services, transportation, and construction and real estate. However, we have continued to see demand softness across most other verticals, customer types and regions. Underlying demand in PCs and servers remains weak, and we are seeing signs of changing customer behavior and storage. Though Q4 was a very good storage demand quarter. We saw lengthening sales cycles and more cautious storage spending with strength in very large customers, offset by declines in medium and small business. Given that backdrop, we expect at least the early part of FY ’24 to remain challenging. That said, our fundamental belief in both the long-term health of our markets and the advantage of our business model haven’t changed. Data continues to increase exponentially in both quantity and value and customers continue to see us as trusted partners, helping them navigate the complexities of hybrid work, multi-cloud and the edge. Unlike in prior cycles, customers are not outright stopping digital investments. They continue to plan projects even as they scrutinize spend. This gives us confidence that we will see a rebound in spending and a return to sequential growth later this year.”

Server demand started weakening in fiscal Q2, and that weakness accelerated in Q3 and deteriorated in Q4, said Whitten, adding that the slowdown is most pronounced among the largest customers. This is precisely what always happens when people are actually worried about a recession. Companies keep machines in the field longer and tighten their IT budgets when it looks like a bump is coming in the economic road. And so Dell is guiding for a “mid-teens” decline in datacenter and client spending in fiscal 2024.

Tom Sweet, Dell’s chief financial officer, said on the call that in the Dot Com Bust in 2000 and the Great Recession in 2008 had four to six quarters of decline, and based on what Dell has seen so far – and assuming past performance of the economy is indicative of future performance (always a dicey assumption), then maybe Dell is then at the tail end of that cycle and therefore Dell is optimistic that the situation will get better as we go through fiscal 2024. In general, Dell expects for storage to hold up better than servers.

The chatter among the chip makers is that the second half of calendar 2023 will be better than the first half in terms of growth.

Now, let’s turn to HPE.

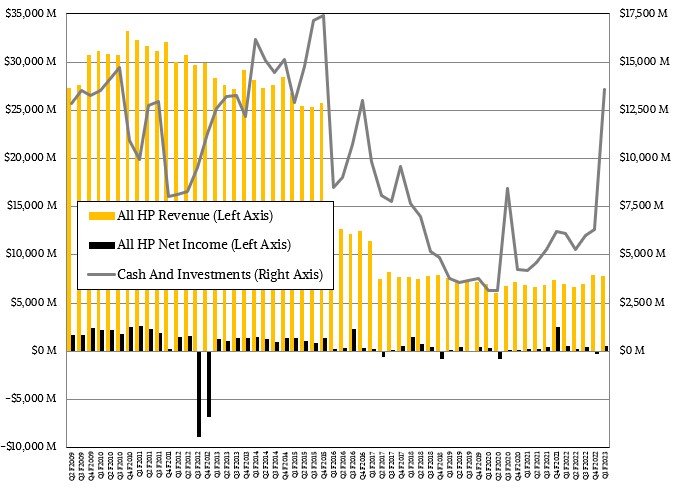

HPE sold off half of itself – specifically its PC and printer business spun out into HP Inc and it also sold off its IT services business that used to be EDS – many years ago, and that is why that long-term revenue and income chart is so hard to see. Those big net losses are the write off of the Autonomy software debacle.

All are well behind us now, and the new HPE is tightly focused on the datacenter, and like Dell, is trying to wring whatever profits it can from servers, storage, switching, and tech support services for its gear.

In the quarter ended on January 31, which was the first quarter of fiscal 2023 for HPE, revenues were up 12.2 percent to $7.81 billion, one of the best quarters in recent years, and net income, while down 2.3 percent year on year, was at 6.4 percent of revenues, one of the best we have seen in a spell.

You have to remember that HPE’s Q1 has two months – November and December – of the calendar Q4 in it, so it is not generally the company’s weakest quarter, but its second strongest one after its fiscal Q4 that ends in October.

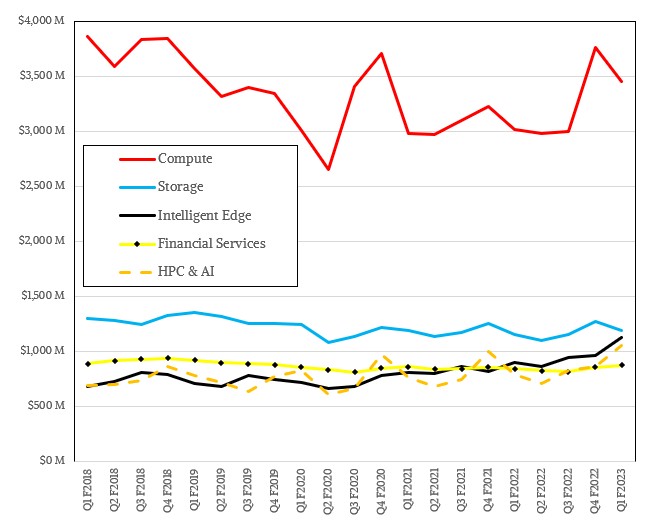

In the January quarter, HPE’s Compute division, which sells servers and switching, had sales of $3.46 billion, up 14.6 percent, and operating income was up 46.4 percent to $609 million, which is a testament to HPE also optimizing its server shipments for higher average selling prices.

Thanks to the revenue recognition of a chunk of the “Frontier” supercomputer at Oak Ridge National Laboratories, sales in its HPC & AI division rose by 33.7 percent to $1.06 billion, but as we have pointed out many times, it is very, very tough to make money in HPC and all that extra Frontier money did not result in more profit, but actually whacked profits and the HPC & AI division only posted a $1 million – no, that is not a typo – earnings before taxes. HPE had earnings of $28 million and $30 million in the two prior sequential quarters on considerably lower sales of $830 million in Q3 F2022 and $862 million in Q4 F2022.

Send HPE and Dell “Thank You” notes, flowers, and chocolates. Better still, send them some business.

HPE’s Storage division was up 2.7 percent to $1.19 billion, up 1.7 percent, and earnings before taxes for this division was down 15.5 percent to $142 million.

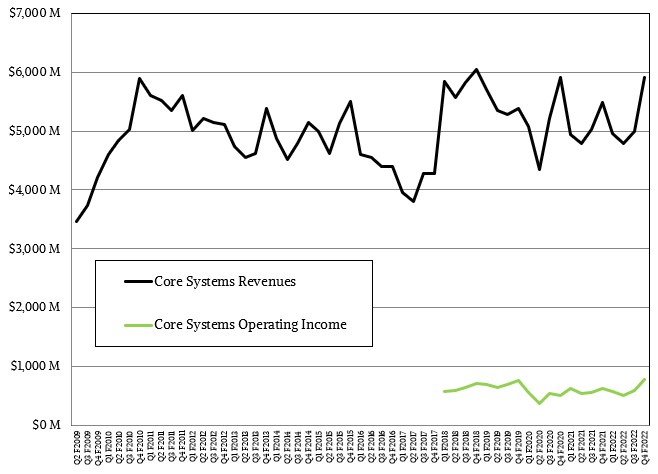

Because HPE was a conglomerate for so long, we have been reckoning what its core systems business has looked like through the decades, including elements from many of its divisions and groups. If you do the spreadsheet witchcraft and add it all up, we think HPE’s core systems business was $5.7 billion, up 14.9 percent, and that earnings before taxes for this core systems business was $752 million, up 30.3 percent.

HPE is more sanguine than Dell looking ahead to the rest of calendar 2023, but is also being cautious.

“We have experienced above-trend demand through much of the past two years, as attested by our growing order book over the fiscal year 2022 period,” Antonio Neri, HPE’s chief financial officer, said on a call with Wall Street analysts going over the figures for Q1 F2023. “And now market demand has shifted from being steady across our portfolio to being uneven over the course of Q1 2023. More specifically, deal velocity for Compute has slowed as customers digest the investments of the past two years, though demand for our storage and HCI solutions is holding and demand for our edge solutions remains healthy.”

Looking ahead, HPE says that in Q2 F2023, revenues will be $7.3 billion, plus or minus $200 million, up 9 percent at the midpoint, and for the full year, it is targeting somewhere between 5 percent to 7 percent growth, which puts it at somewhere between $29.82 billion and $30.49 billion.

The best way to predict the future is not a large language model, but to live it. So let’s get on with it.

Be the first to comment