It is the nature of the many businesses that Hewlett Packard Enterprise remains in, after spinning off printers, PCs, services, and software, that it still has many ups and downs and there is always one business that can pull down the others. This was true of the larger Hewlett Packard, and there is no escape for this truth about conglomerates and companies with complex and varied product lines, as it was also true of the IBM of days gone by that Hewlett Packard was trying to emulate with all those acquisitions in the 2000s.

Given this, plus the state of the IT supply chain due to shutdowns in China and elsewhere because of the coronavirus pandemic, and just the plain difficulty of being an OEM that does a certain amount of research and engineering on its servers, storage, networking, and systems software in an IT world dominated by the hyperscalers and cloud builders, which have enough margin to fund projects that a company like HPE can’t even dream of, the amazing thing is when a company like HPE turns in a fairly decent quarter.

Which it did. The company was constrained by parts shortages and manufacturing capacity issues that held back its core ProLiant server business, it had a major supercomputing system’s revenue recognition pushed out by a quarter (we are not sure if it was “Frontier” at Oak Ridge National Laboratory in the United States or “Lumi” at CSC in Finland), and the storage mix was not in its favor. But HPE hung in there and built the iron that it could and that millions of enterprises around the world need to do their IT. As we often point out, someone has to build the machines IT depends on for on-premises processing and that HPC centers depend on for supercomputing, and HPE is that someone. Send thank you notes because it would all be a lot more expensive if you had to do your IT in the cloud.

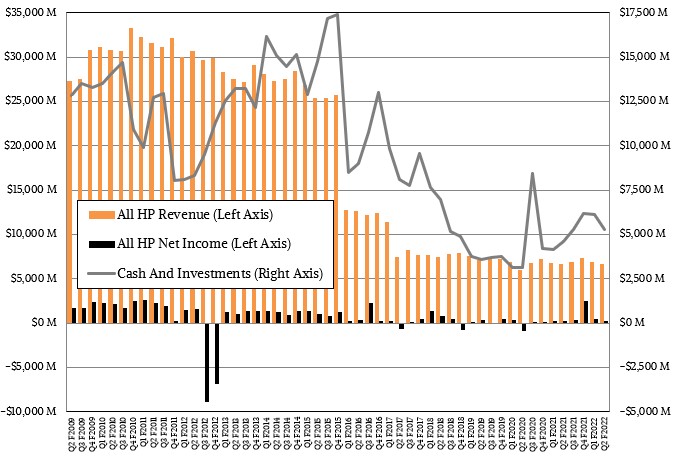

In the second quarter of fiscal 2022 ended in April, HPE’s revenues were up two-tenths of a point to $6.71 billion, and its net income fell by 3.5 percent to $250 million. Cash and investments rose by 14.4 percent to $5.29 billion, and the company has record backlogs in compute, storage, and networking, attesting to high demand in the face of tight supply.

There are worse positions to be in, and the old Hewlett Packard spent plenty of quarters being in them.

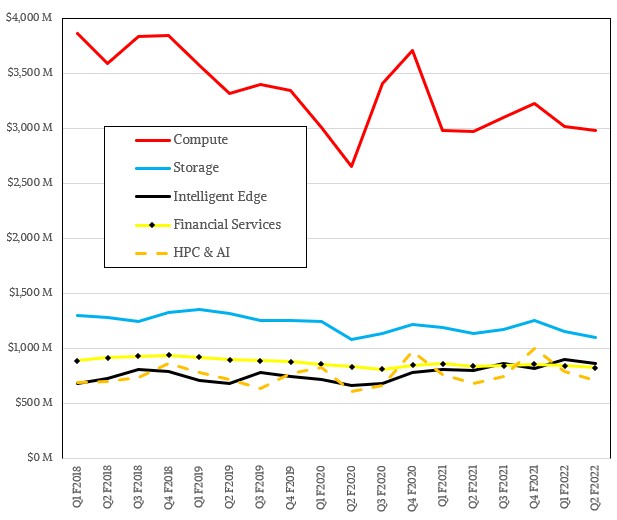

In the quarter, the Compute division, which is mostly ProLiant servers, had sales of $2.99 billion, up three-tenths of a point, but thanks to richer configurations and the effect of price increases for components that are being passed onto customers (after HPE held back for a reasonable time), operating income rose by 23.9 percent to $415 million. Order growth in Compute was more than 20 percent for the fourth straight quarter (up 23 percent to be precise in fiscal Q2), and that is with unit shipments “down mid-teens year on year with supply chain tightening” and average unit prices up more than 20 percent thanks to those price hikes and richer configs.

We defy anyone to do any better than HPE has done. Cisco Systems and Dell both had their own issues in their most recent quarters, and IBM is not really in this game the way those three companies are anymore. No company is immune to the shutdown and supply chain issues. At some point this year, Compute and Storage and HPC & AI will all hit the cylinders at the same time, and HPE will probably turn in a very solid quarter. IBM had some quarters like that, you will recall. They are the exception, not the rule, and they make it palatable to be a conglomerate with a mix of ups and downs or flat spots, as the case may be.

The HPC & AI division had its issues, as it always has and as it always will. In the quarter, sales were up 3.6 percent to $710 million, but this division shifted to an operating loss of $40 million compared to an operating gain of $19 million in the year ago period. Pricing on HPC systems is set, so HPE has to eat the supply chain issues, but the machines in the whopping $3 billion backlog (up 18 percent year on year) that HPE is sitting on in its HPC & AI division were set at different prices and fulfilling that backlog over the next couple of years should be more profitable than deals signed several years ago. At constant currency, HPC & AI sales were up 5 percent and HPE reiterated its goal of this business exceeding the 11 percent compound growth rate of the HPC and AI sector in the time spanning its fiscal 2021 through 2024 years.

HPE’s storage business was off 3.4 percent to $1.1 billion and operating income was down 27.7 percent to $138 million. Sales of flash and hyperconverged arrays and special machines for data analytics had double-digit growth, and the record-level backlog in storage (which HPE did not quantify) was tilted to “margin-rich” products laden with the company’s own intellectual property. (The richness is relative, of course. HPE does not have the kind of high margins that near monopolies – IBM mainframes, Microsoft Windows and Windows Server, Google search, Facebook and Google in advertising, and Amazon Web Services in cloud – can command.

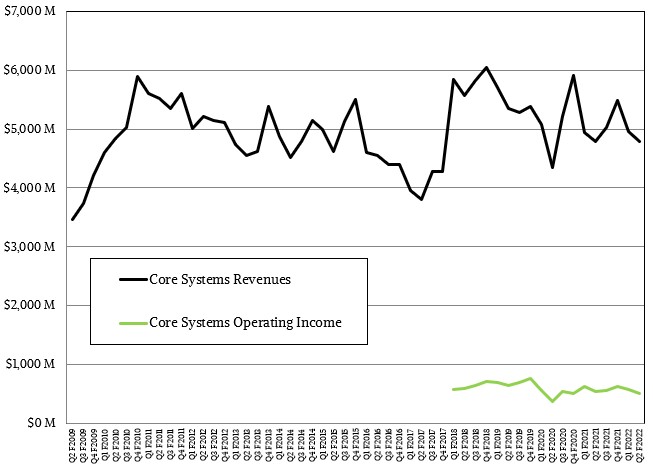

As usual, the core HPE systems business – the one that it has burned to boats to focus on – plugs along, and by our estimates, was off a mere one-tenth of a percent to $4.79 billion, with operating income off 5.9 percent to $513 million.

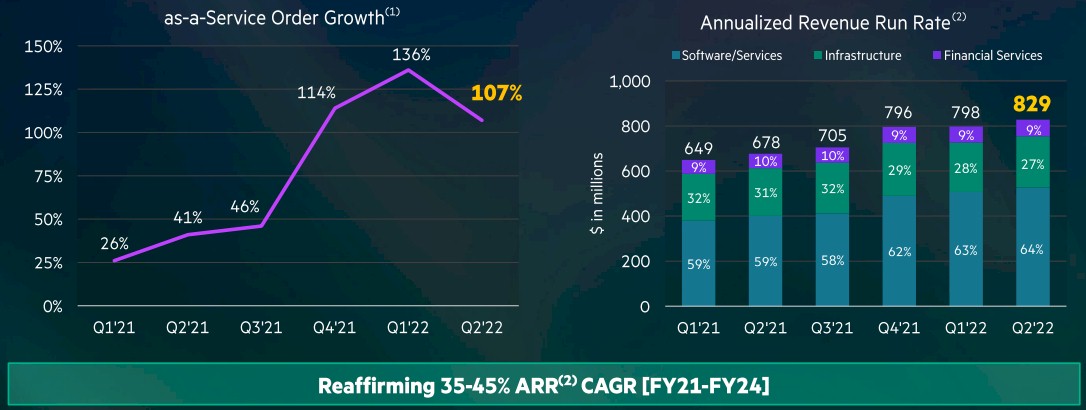

The utility priced part of HPE’s business – we find the “As A Service” or AAS abbreviation annoying and wish we could all agree on a word here – continues to grow up and to the right, as you can see from the chart above. The order growth rate has been in the triple digits in the past three quarters, although it did slow in fiscal Q2, but that annualize revenue run rate keeps rising, ever so slowly. HPE did not call out the number of customers it had added for its GreenLake utility model, which has HPE retain ownership of the machines and customers pay a subscription to use them on-premises or in a co-lo of their choice, and it does not yet provide revenues for GreenLake, but when it becomes material, we expect for HPE to do that. What Antonio Neri, HPE’s chief executive officer, did say on a call with Wall Street that it has $6 billion in GreenLake hardware, software, and services on its balance sheet.

“Obviously, those bookings eventually will unwind from the balance sheet and through the P&L,” Neri explained. “And the other important fact here is that our mix of GreenLake is shifting every single quarter to more software and services, which obviously comes with a significant higher margin than just the hardware.”

The annualize run rate for utility priced stuff is growing at 25 percent at constant currency, which is 17X faster than the growth rate of HPE’s overall business at the same constant currency metric. That HPE can maintain steady revenues in such an adverse environment while at the same time embracing subscription pricing and throwing so much stuff onto its balance sheet is actually a bit of a feat.

This is the best strategy that HPE can do. It could have borrowed tens of billions of dollars to build a cloud that could not compete against AWS, Microsoft Azure, and Google Cloud, or it could take all the best parts of the cloud/utility approach and bring it to the corporate datacenter and partner with clouds for on-premises and co-lo systems and carry a huge balance sheet of gear (which will probably be on the order of building a fairly large cloud infrastructure). It took HPE a few years to figure out the second strategy was better after trying, unsuccessfully, to execute the former. But we think HPE has a pretty good response to market needs and expect for this transition to GreenLake to be a successful one.

Now, that does not necessarily mean HPE will suddenly be more profitable, although there is a possibility that profits could rise. The core businesses that HPE are in are not particularly – X86 servers and HPC systems in particular. But we do think that subscriptions can deliver more money that product sales because you have to pay to weigh down HPE’s balance sheet on not your own. That is a kind of utility, too. This is one of the reasons why AWS is so profitable, and there is no reason to think that HPE cannot get at least some of that action and do so across hundreds of thousands of customers who don’t want to own hardware and software anymore but who do want to pay for possession and control of these.

Be the first to comment