The good news, and we all need to be looking at the bright sides of things a bit these days is that the biggest IT shops in the world want to buy a lot of datacenter gear from Cisco Systems. Across the board with large enterprise and commercial accounts, the demand is strong and the order backlog just keeps growing and growing as companies widen their time horizons and pre-order well in advance of when they actually need gear.

The bad news is that there is rampant inflation in the wake of the economy being overheated from the economic stimuli provided by the governments as they tried to insulate us all from the economic side effect of the coronavirus pandemic, and a war in Europe, which is making governments, companies, and consumers alike a bit jumpy and testy.

As usual, Wall Street overreacted to the news that Cisco’s demand exceeded its supply thanks to it shutting down operations in Russia and Belarus and to the COVID lockdowns in China, which are affecting sales as well as production of IT components. On a call going over Cisco’s numbers for the third quarter of fiscal 2022 ended in April, Scott Herren, Cisco’s chief financial officer, said that shutting down business in Russia and Belarus – and we have to assume that sales in Ukraine are also nil given the war – cost the company about $200 million in sales in the quarter, which represents about 2 percent growth that Cisco was expecting that it didn’t get. Herren added that historically sales to Russia, Ukraine, and Belarus generate about 1 percent of its sales. So this is not a big part of Cisco’s business. The same quarter last year had an extra week of business, too, so that was another 3 percent of tough compare in the period.

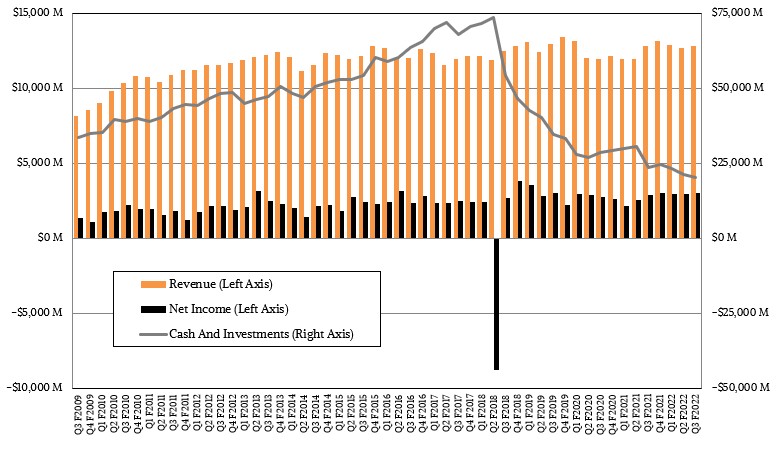

In the quarter, Cisco’s sales only rose by two-tenths of a point to $12.84 billion, but net income rose by 6.3 percent to just a tad over $3 billion. Cisco blew $1.8 billion in cash in the quarter, with $250 million of that on share repurchases and the remaining $1.55 billion on its very high dividend, which Cisco is doing to keep Wall Street at bay.

Five quarters ago, Cisco had $30.59 billion in the bank, and now it only has $20.11 billion, and this is just a far cry from the $71.85 billion it had in the second quarter of fiscal 2017. This is the lowest amount of cash that Cisco has had in the bank in recent memory. Anyway, the till has 14.7 percent less dough in it than it did a year ago.

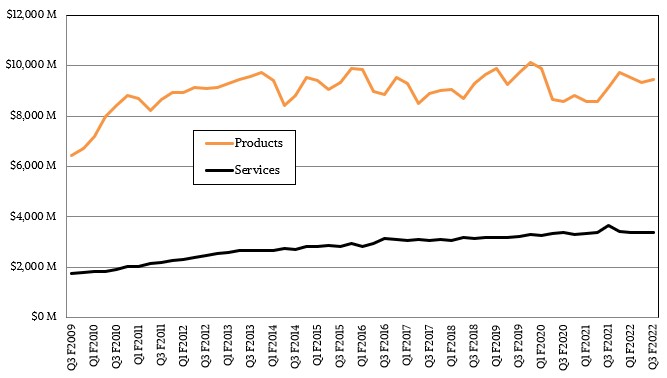

In the third fiscal quarter, product sales rose by 3.4 percent to $9.45 billion, while services sales fell by 7.6 percent against a very good Q3 last fiscal year. The services sales in the current quarter were consistent with that of the prior couple of quarters, but this needs to grow more than it has been.

The backlog at Cisco, as we said, continues to grow. Herren said that as Q3 came to a close, Cisco had $15 billion in deferred product revenues and another $2 billion in deferred software revenues – meaning things customers have paid for but which it cannot put on its books as yet because it cannot deliver the products. And it has another $30 billion in remaining performance obligations, or RPOs, which are on the books but can only be recognized as services and products are delivered under a contract. That is nearly one year’s worth of revenues, just waiting for Cisco to fulfill against it. That’s not an IBM Global Services backlog, which was on the order of 2X of IBM’s revenues at any given time for many, many years, but it is not a molehill of pennies, either.

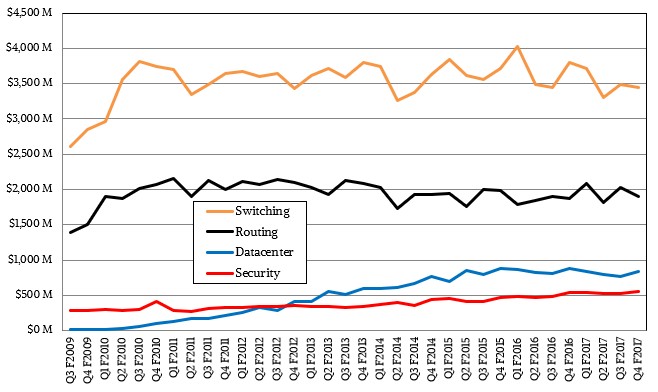

It is tough to tell how Cisco’s “real” datacenter business is doing these days, and it gets tougher each time the company rejiggers its financial reporting categories. Here is what Cisco’s financials used to look like until 2017:

Look at how easy it is to see how switching and routing just shuffle along and that the Datacenter group – meaning Unified Computing System (UCS) integrated servers and switching, adapters, and peripherals and systems – was what was really growing since Cisco introduced them during the Great Recession. It was a great run, and Cisco is still an important systems supplier, but the growth engine is done there, and it is among the top ten server manufacturers, like IBM, but it is not among the top five, also like IBM.

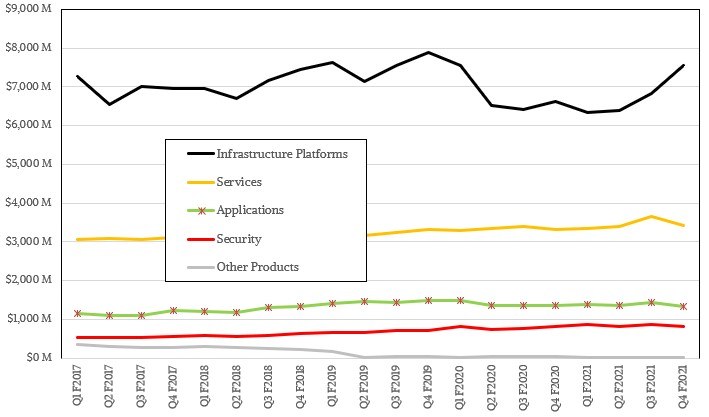

Here is how the financials were changed in 2019, backcast into 2018:

Cisco changed the way it characterized its businesses, and frankly, to obfuscate its numbers a bit to keep competitors and probably Wall Street guessing some. Servers, datacenter and campus and edge switching, and datacenter and campus routing were all put into one pile with a while bunch of software, and now we couldn’t see them as clearly.

And now, this is the new categorizations that Cisco put together last year:

It is very hard for us to not call Secure Agile Networks “servile networks,” welcome to our brain, have a nice day. In any event, this includes datacenter and campus switching, enterprise routing, servers, and wireless networking. Internet For The Future includes Cisco’s Silicon One merchant silicon, optical routing, 5G gear sold to telcos and governments, and various optics. Collaboration was called Hybrid Work and includes things like GoToMeeting, video conferencing systems, and other collaboration tools.

What this shows is that Cisco is just plugging along, with one quarter pretty much looking like the prior couple of quarters, with some wiggles here and there to keep us from nodding off or getting agitated. (There is something to be said for being steady, but Wall Street values growth above all else because how else to justify crazy stock valuations in the face of perplexing economic times?

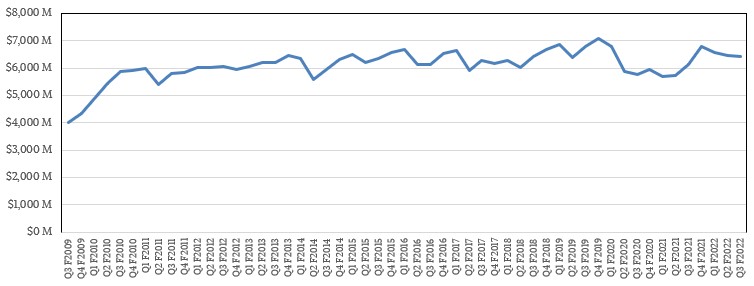

Since we started monitoring Cisco’s financials here at The Next Platform, which we backcast to the Great Recession, we have added together servers, switching, and routing to get a datacenter revenue proxy, and we have continued to do this through all these categorization changes on behalf of the changing top brass at Cisco. Here is what it looks like:

This is like investing in Consolidated Edition or Commonwealth Edison – power utility companies – in the 20th century. Which stands to reason given Cisco’s place in the datacenters and on the campuses of governments, academic institutions, and enterprises. If you squint, there is a slight uptick on the right, but in recent quarters the ups are not pulling up the downs, and this is because of supply chain issues. For whatever reason, Cisco is getting hit hardware by this than some of its upstart networking peers, like Arista Networks, for instance. Herron said that Cisco has around 41,000 unique components it has to buy for its gear and about 350 of them “have potential supply concerns right now.”

One of them cited by Chuck Robbins, Cisco’s chief executive officer, was power supplies made in China for various equipment. Cisco took a $300 million revenue hit in the quarter because it had 11,000 circuit boards built for gear and could not get power supplies because of the COVID lockdowns in China.

For want of a screw, a quarter was, well, not lost, but diminished. But, where ya gonna go to get better supply if you are buying servers, switches, or routers? Everyone else has the same problems, to varying degrees.

We wonder how much double and triple booking is going on in the IT industry, given all of this. In any event, Cisco’s revenues were down by more than $1 billion for Q3 fiscal 2022, and no one is happy about it on Wall Street or at Cisco.

Herron did drop some tidbits to give us a sense of how different parts of the datacenter business at Cisco was doing. Cisco had “solid growth” in servers, but enterprise routing was down. Datacenter switching grew, particularly the Nexus 9000 line, and campus switching grew led by the Catalyst 9000 and Meraki lines. Wireless networking (not a datacenter but a campus thing) was up in the double digits.

In its customer segments, sales to enterprises – what we would call large enterprises – were flat in the quarter, but sales in the commercial segment (the rest of companies) was up 19 percent, to service providers was up 8 percent, and to governments and academia was up 4 percent. Oh, and the effect of two price increases announced in fiscal 2022 so far have taken effect, and revenue was boosted about 1.6 percent. (Which means volumes actually fell because revenues did not rise by much – math Cisco confirmed was correct.)

The flatness in enterprise spending has heads turning to the side a bit, and Robbins piped up on this one.

“Our customers are not signaling any real shift at this point, we are not hearing that from them,” Robbins explained. “We had our global customer advisory board just a couple of weeks ago, where we had one hundred of our biggest customers, and they were all talking about projects in the strategic nature, of everything they are trying to accomplish. The last thing I would point out is on the enterprise side, last quarter we grew 37 percent. Just to keep in mind the way we define enterprise is a finite list of named customers. So it tends to be more lumpy. If I look at how the industry defines enterprise, that would reflect a combination of our enterprise and our commercial business. So, for comparisons to what we are hearing in the marketplace, I thought we would give you that combined number. If you combine enterprise and commercial together, we grew 9 percent, but without the Russia impact, we actually grew 12 percent and on a trailing 12 months basis, it grew 28 percent. So we are still comfortable with the demand signals that we are seeing and our customers aren’t telling us anything differently right now.”

Be the first to comment