Ever since Nutanix, the first virtualized server-storage smashup, dropped out of stealth in 2011, we have been watching with great interest to see if this hyperconverged infrastructure would take the world by storm. Or, at the very least, become pervasive among small and medium businesses and more than a few large enterprises who wanted more of a complete platform stack running on commodity hardware than they had been able to get up until Nutanix came on the scene.

By some measures, Nutanix has been very successful. First and foremost, by establishing the hyperconverged infrastructure market in the first place — which put a virtual SAN inside of the same virtual machines as a virtual server cluster, creating an extensible server and storage fabric that was integrated, easy to use, and in theory less expensive.

Nutanix uncloaked from stealth mode a little more than a decade ago after three years of development with the Nutanix Complete Cluster and its integrated Scale-Out Converged Storage, or SOCS — a distributed block storage system that could use both disk and flash storage. The storage and compute ratios were fixed at different points in different appliances crafted by Nutanix itself, which sold its Complete Cluster as a full hardware and software stack, as the name implies. Think of it as the modern, X86 equivalent to the full stack approaches of the IBM AS/400 and DEC VAX minicomputers or the IBM mainframe. And initially, because of the simplicity and scalability that it brought, the Nutanix appliances were very expensive, and most of that was in the software licensing.

Over time, the Nutanix base grew steadily, but not explosively, but its success — and the fear that Nutanix would hockey stick at any moment — finally convinced VMware to get its vSAN act together. This, more than anything else, helped to justify the hyperconverged infrastructure, or HCI, market, as it is now called — but at the same time, it gave Nutanix some real competition and also spawned a dozen or so contenders, most of which who have been bought up by incumbent server and storage makers. Nutanix remains freestanding and publicly traded, so this is how we get some insight every quarter into what is happening with HCI. Nutanix raised $350 million in five rounds of funding, went public in 2016 raising another $237 million, broke through $1 billion in annual sales in 2018, and got $750 million in debt financing from Bain Capital a year ago to help it try to grow its way to profitability.

Such profitability has been elusive, in part due to the changing nature of storage appliance and enterprise software sales and in part because of HCI has not taken off to the degree that many had expected.

We have nothing but respect for company founders and technology innovators, having several iterations of companies under our own belts here at The Next Platform, so it is important to not take this the wrong way. Like Nutanix, we are a hopeful people. (Who else would launch a high tech publication in 2015?) But it is fair to say that this has not been an easy path for Nutanix. The company has consistently grown sales of its HCI platform, which has had many names over the years. (That is always another sign of trouble in the IT business.)

Nutanix has created its own variant of the KVM hypervisor to get VMware out of its mix, thus lowering the cost and increasing integration of its HCI stack. And it has made two major product transitions that have been jarring to its top and bottom lines. The first transition in its fiscal 2018 year (so only four years ago) was to get rid of appliances and shift to sales of software on more standard OEM configurations. This coincided with a loosening of the static compute-storage ratios that existed in the Nutanix appliances. Compute and storage have to be able to scale independently, at least to some degree, to meet the wide variety of workloads in the field. Nutanix did appliances for the same reason other storage makers do: to limit the support matrix for hardware. You can go broke trying to support too many variations.

There are, however, many ways to go broke for a startup, and when customers consistently asked to run the Nutanix stack on their OEM hardware, finally Nutanix relented and ate the cost. And then, only a year later, it switched from perpetual software licensing to software subscriptions, which now drive the company.

For better or worse.

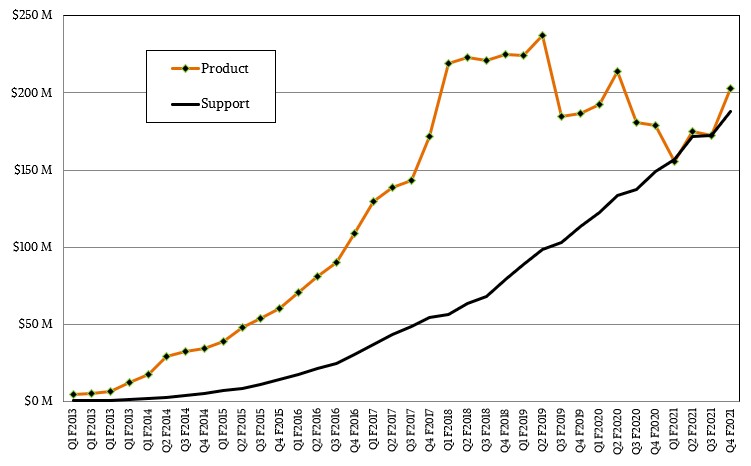

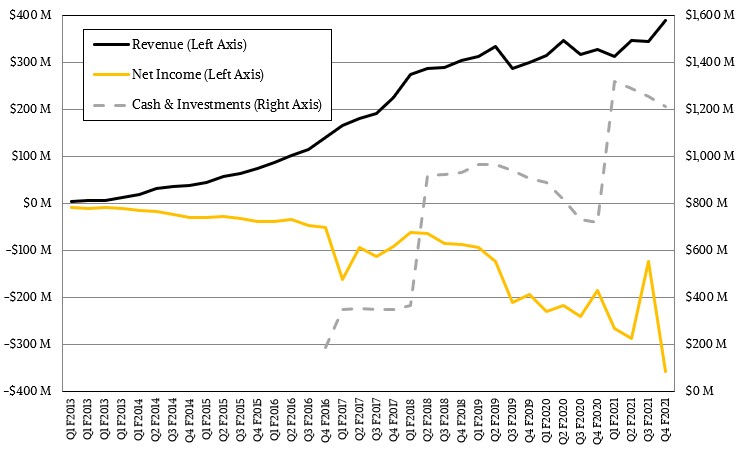

In the fourth quarter of fiscal 2021 ended in July, Nutanix had $203 million in product sales, up 13.3 percent year on year, and support sales of $187.8 million, up 26.2 percent. The company’s pile of cash has been shrinking a little but still stood at $1.21 billion as the quarter came to a close, which is pretty close to the $1.39 billion in revenues for the trailing twelve months. Nutanix has plenty of cash to ride out storms.

But good heavens, is it ever bleeding money, as it has been for most of its history. In the fourth quarter, Nutanix lost $358.2 million dollars, which was nearly as large as its revenue stream. And to make it clear, it brought in that $390.7 million for products and services, spent that, dipped into its cash a little bit, and spent that, and then posted a loss of $358.2 million on top of that. From fiscal 2013 through fiscal 2021, Nutanix has brought in $6.71 billion in revenues, but lost a staggering $3.7 billion.

In the quarter, Nutanix finished with 20,130 customers, which is a pretty big number by some measures, and it is a number that has grown pretty steadily 800 to 900 customers per quarter in fiscal 2017 through 2018, but has tapered off to around 700 customers per quarter more recently. It is not for want of spending on sales and marketing, which drives about two-thirds of those losses (which is real costs as well as stock-based compensation to retain employees, the latter of which is not a small number).

In a prior time, such as the minicomputer revolution of the early 1980s through the early 1990s, when many companies were commercializing their back office operations for the first time, or the Unix server revolution of the middle 1980s through the end of the 1990s, the aggregate installed bases of the major platforms numbered hundreds of thousands of unique customers. Let me be precise: hundreds of thousands of customers for each platform. There were 250,000 IBM System/3X customers and then 275,000 IBM AS/400 customers; probably an equal number of DEC VAXen. And then the aggregate Unix system installed base was probably closer to 400,000 customers, split across multiple vendors, with HP and Sun dominating.

Even if there are 50,000 HCI customers in the world, this is a drop in the bucket compared to a much larger IT installed customer base some decades later.

At this point in the evolution of HCI, we would have expected for the customer base for Nutanix to be an order of magnitude bigger — and we strongly suspect that Dheeraj Pandey, the co-founder and former CEO at Nutanix who stepped down from that role last year, expected a much larger customer base too. The customers that love the Nutanix stack love it — just like IBM AS/400, DEC VAX, and Hewlett Packard MPE customers did back in the day or even Sun Microsystems Solaris, Hewlett Packard HP-UX, and IBM AIX customers did a few days later. But for some reason, Nutanix has not been able to get that hockey stick of adoption.

It is a bit of a mystery. Some of that has to do with being caught in the pincers between Microsoft’s Windows Server stack and VMware having virtual compute, storage, and networking. Both companies offer alternatives to the Nutanix stack, and they own much larger enterprise computing bases. The kind we are talking about. And IBM, now with control of Red Hat, would seem poised to try to do the same. But in recent months, Nutanix and IBM have worked together to make OpenShift the preferred Kubernetes platform for Nutanix.

At some point, don’t be surprised if IBM ends up acquiring Nutanix. But not now, with Nutanix having a nearly $8 billion market capitalization and possibly commanding a $10 billion acquisition cost. If IBM wanted to do what all the cool kids are doing, it could burn some of its $125 billion in market capitalization, buy Nutanix in an all-stock deal and use the Nutanix cash pile to reinvest in the product line and expand it into the Red Hat and IBM systems sales channels. It is not a very good fit anywhere else, excepting perhaps Dell. Hewlett Packard Enterprise and Cisco Systems already have bought their HCI stacks, and Inspur and Lenovo show no inclinations to being software players.

Or maybe, in the long scope of time, hyperconverged infrastructure will be a technology suited to a very precise moment in time — like server virtualization will eventually be — and the world will embrace disaggregated but composable servers and storage, with bare metal servers running containers to provide compute and storage services – all interlinked by DPUs. Maybe the base is not as big as we think it should be for a good reason: people are waiting for a better, cheaper answer. One that the hyperscalers and cloud builders have already proved out.

So many ways for customer to solve their problems, but HCI’s Working pretty well on our end. Just sayin. #vxrail

Your focus is on Nutanix and not HCI in general. Cisco HX, Dell VXRail, Rancher Harvester, VMware VSAN….

If you have ever used Nutanix, you wouldn’t have wrote such a misleading article. Nutanix is half baked product, full of bugs and failures at each component level. Be it Stargate, Cassendra, etc. They have very basic level of logical failures at each level and even though theg say that they have one click upgrade process, in reality its all manual because there dark bundles and upgrade process have too many issues which never goes as advertised.

Just ot say it is the well known Cassandra not “Cassendra” and i’m using Nutanix since 2015 without seeing all the “bugs” you are talking about, it’s a robust and very well supported (NPS > 90 for the last 7 years) solution compared with all the competitors, so i guess your comment is a fake.

The real reason it hasn’t hockey sticked is because of 2 things, both people related: 1.IT Staff doesn’t want to learn new things- why bother when you can sit happily using vcenter your whole career, and 2. Job protection. Legacy storage admins are scared to death of HCI as it makes them mostly unnecessary, but to be fair SSDs started that trend even in 3tier. Who calculates spindles now? Lol. My vdi team owns our infra completely and we went all in on nutanix and it’s been great not having to engage a storage admin to carve out luns anymore.

One factor limiting HCI is its modest scalability. I have never heard of of a HCI cluster greater than 64 nodes. All that metadata chatter to keep the distributed storage replicated and synchronized takes its performance toll. That makes it great for some point applications, but is hardly full elasticity and data center scale.

Hyperconverged Storage may not have become pervasive simply because of its restrictions: the tie to a specific hypervisor preventing the flexibility of bare metal or native container support; and the high consumption of valuable compute server CPU, memory and networking resources. If your company needs more than a specific hypervisor (and therefore has to buy other external storage solutions) or it is worried about buying up to 30% more compute servers and associated software licenses to overcome HCI overhead, then pretty quickly Nutanix and VxRail become too limiting. That is why the external Storage market has stayed so strong so long. Nebulon smartInfrastructure (I admit I am a founder) was founded to address both these challenges in a server embedded solution that also gives on-premises IT customers a public cloud-like experience through a SaaS management interface. You can run any type of application, anywhere, on the servers of your choice. It may be the first server based solution that has the complete flexibility of external storage without the cost overheads of HCI or three tier architectures.

I prefer converged infrastructure, disaggregated HCI, composable disaggregated infrastructure, and most of all hyperscale, over hyper-converged infrastructure.

Composable disaggregated infrastructure might be the final stage in the evolution of IT infrastructure.

Agreed. And at some point, when that is all normal, we can go back to calling it “infrastructure.” HA!

Is hyperscale the same as disaggregated HCI? If not, what’s the difference? Is Commvault Hyperscale X an example of disaggregated HCI?