Does Michael Dell want to be Intel’s largest shareholder? Maybe, just maybe. And there could be an interesting turn of events once VMware is spun off to shareholders in Dell (the company), leaving Dell (the man) as VMware’s largest shareholder, with an approximate 42 percent stake. Imagine, if you will, that Pat Gelsinger, the former head of Intel’s Data Center Group and recently the former head of VMware and now the current chief executive officer at Intel, wants to do virtual CPUs and virtual network ASICs as much as he wants to do physical CPUs and physical switch ASICs.

Imagine, in fact, that Intel decides it wants to buy VMware back from Wall Street, to create a physical and virtual powerhouse.

This is what an intrepid reader of The Next Platform proposed to us and said we should do some game theory simulations on the idea. And once we stopped laughing, we thought, well, why not think about Intel buying VMware? It may end up being more like chaos theory, but here goes.

For the past decade and a half, nothing has curtailed sales of X86 server processors quite like VMware’s ESX Server, GSX Server, and ESXi hypervisors, which came into the market just ahead of the Great Recession, which started in late 2007 and continued through early 2010 or so (in the IT sector at least). Back then, VMware hypervisor running on a single physical server could double or triple utilization by cramming multiple, whole server environments into virtual machines, which allowed many companies to forego a whole generation of server buying at a time when the economy was really messed up and IT workloads were changing like crazy and expanding rapidly. That timing, along with the “Nehalem” Xeon E5500 processors – finally a good X86 server chip from Intel – also launched in 2009, set Intel on the path to dominance in the enterprise datacenter that has been up until now, when that dominance is being called into question by the re-emergence of AMD and the rise of Arm in the datacenter.

Let’s talk about that spinoff for a second. Under the proposal, VMware will distribute a cash dividend of $11.5 billion to $12 billion to VMware shareholders, of which Dell Technologies is the largest, with an 81 percent stake. The rest was sold off to the public by EMC, which technically should have been illegal as far as we are concerned. Why? Because when EMC bought VMware in 2004, EMC shareholders already owned all of VMware and it should have been illegal to sell the initial 15 percent stake of VMware separately to Wall Street, which grew to 19 percent over the years. This was always a bit too much like Max Bialystock from The Producers for our taste. (You can’t sell 25,000 percent of anything, even if it isn’t a flop. Or as one of our mentors used to say, “Anything worth selling once is worth selling two or even three times. . . .”) With the spinoff, Dell (the company) gets $12 billion or so, and $9.7 billion of that goes to Dell Technologies. In exchange, the individual Dell shareholders plus the existing VMware shareholders take control of VMware, which is a separate company already trading on Wall Street separately, and a part of the $67 billion EMC-VMware acquisition that Dell did back in October 2015 unwinds.

When this is done, Michael Dell will control 42 percent of VMware personally and his long time cash line provider, private equity firm Silver Lake Partners, will control 11 percent. This means that as long as Silver Lake agrees with Michael Dell, Michael Dell really runs VMware, not Raghu Raghuram, a long-time top executive from VMware who we have known forever and who was just appointed chief executive officer, replacing Gelsinger. Dell, the man, may be happy to have Raghuram actually run VMware, as he was happy to let Gelsinger do it before him. But make no mistake about who is in control.

Now, if Michael Dell really wanted to up his game and get in on the ground floor of a company in transition, and possibly help Dell, the company, as well, he might approach Gelsinger and propose that Intel take over VMware. And with Nvidia spending $40 billion (mostly in stock) to buy Arm Holdings and with AMD spending $35 billion (mostly in stock) to buy Xilinx, we think there is probably a way for Intel to acquire VMware mostly in stock and not use a lot of cash it needs to ramp up its Intel Foundry Services business to take on Taiwan Semiconductor Manufacturing Corp and Samsung Electronics in advanced semiconductor manufacturing, as is the plan Gelsinger has come up with along with creating better chips for clients and servers.

As we go to press, Intel has a market capitalization of $216.5 billion and has issued just over 4 billion shares on Wall Street. As it exited the first quarter, Intel had a trailing twelve month revenue of $77.7 billion, $20.3 billion in operating profit, and $18.7 billion in net income. As for Intel’s balance sheet, the important things are $5.2 billion in cash, $2.4 billion in short-term assets, and $14.8 billion in trading assets that can be liquidated as need be. Ditto for Intel’s additional $5.4 billion in equity investments and $1.4 billion in other investments. Add that up, and it is $29.2 billion. Intel has promised to spend $20 billion on foundry expansion and stop its share buyback nonsense, and it keeps generating more than $4.5 billion a quarter beyond that. So it can blow a lot of its cash because the coffers will refill for a while – so long as the IT market is expanding.

VMware has 77.7 million shares on Wall Street today and a market capitalization of $65.6 billion, which would make an acquisition very expensive. More expensive than what Michael Dell did to do the EMC-VMware deal, the biggest one in IT history. Intel would have to massively dilute its shares to cover the bulk of a VMware acquisition, but the good news is that there is very little chance another buyer would emerge. But clearly, to take control of VMware requires the consent of Michael Dell and Silver Lake because they own more than 51 percent as a pair.

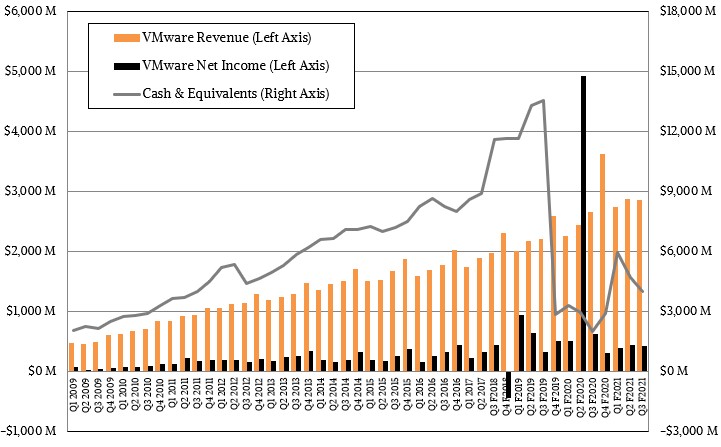

In its trailing twelve months (which runs through the end of October 2020 because VMware has not yet reported the end of its fiscal 2021 year), VMware has $12.1 billion in revenues, operating income of $1.7 billion, and net income of $1.6 billion. At this point, it is a steady freddy, legacy systems software platform with over 300,000 customers in the enterprise datacenters of the world. In 2013, there were 36 million VM guests on the ESXi hypervisors of the world, and we estimated in 2018 that had nearly doubled to around 60 million guests. It is probably closer to 90 million guests these days. VMware has not reported numbers for the vSAN virtual storage and NSX virtual networking bases in a long time, but vSAN could be in the range of 30,000 customers these days and NSX could be in the range of 10,000. Those are pretty big bases, even if only a fraction of the VMware ESXi installed base.

What VMware only has left is just under $4 billion in cash as it has already paid out a huge wonking dividend to shareholders, as you can see in the chart above. Cash in the acquired company is always part of the equation, and in this case, it doesn’t change the price of the deal all that much.

The VMware business would snap right into Intel’s Data Center Group, which may be particularly important if many of the hyperscalers, who represent on the order of 35 percent to 40 percent of CPU sales for Intel in any given quarter, start designing chips and having them fabbed for their own private use, as Amazon Web Services does for CPU and DPU chips today as well as for AI training and inference. Something has to fill that revenue and profit gap, which we think is going to open up, and doubling down on enterprise customers who will absolutely pay a lot for legacy platforms so they don’t have to change them. Enterprises like to evolve things very slowly, achingly slowly over decades, until they can’t stand it anymore. Then, they try to throw it out – and a lot of the times, they still can’t. IT is not their business, as it most certainly is for hyperscalers and cloud builders.

In the trailing twelve months, Intel’s Data Center Group had $24.7 billion in sales and $8.4 billion in operating profit and that operating profit is coming down and it is going to keep coming down as AMD competes hard in servers and the Arm collective (represented by Ampere Computing and those who are building their own Arm server chips like AWS) keep hammering on Intel. In fact, VMware operating profit is rising and converging on where Intel’s Data Center Group profit is heading, so blending them somewhere around 2022 would not hurt either company. And, after Intel sells off the NAND flash business to SK Hynix (no, you do not get to randomly uncapitalize a proper noun, sorry) for $9 billion, the combination of Data Center Group and VMware would create a bigger datacenter business than a client business at Intel. If that matters.

We think it might matter to Gelsinger, who is looking for wins, and who knows VMware better than he does? Who knows better the competitive issues it faces? Or the beauty of a legacy platform that can be milked?

The question is, does Michael Dell appreciate this, and does he want to be the largest shareholder of Intel but lose his controlling stake in VMware as part of the bargain. Just to pay for VMware without a premium, Intel would have to issue 1.2 billion shares, which is a lot. The premium might have to come from cash, and Michael Dell would get his 42 percent of that to put into his own pocket, so that is a motivation. But his stake in Intel, unless he already owns a lot of it privately, would only be around 10 percent. Still, that is probably a lot of sway separate from the control Dell, the man, has over the largest OEM server and PC supplier in the world.

Intel could certainly use VMware to do a better job attacking virtual storage and virtual networks, and to come up with a coherent and enterprise-friendly DPU story.

Intel buying VMware once it is set free is an interesting idea, and not the stupidest thing we ever heard, considering all of the chess pieces on the board. For all we know, this is the plan that is cooking. And if not, you can bet Dell and Gelsinger are thinking about it right now.

One final thing. Here is the secret decoder ring to decipher the title. The following are the architectural generations of X86 processors relevant to the datacenter, subject to debate we realize. So this crazy idea ranking is a bit of an Easter egg. We are only counting architecture “tocks” and not process shrink “ticks” as CPU generations.

- 8086: The beginning of it all, also known as the iAPX 86. (1979) The 8088, launched in the same year with a skinnier I/O bus, is a variant of this, and it is arguable that it is really that different by modern standards.

- 80186: Also known as the iAPX 186. (1982)

- 80286: Also known as the iAPX 286. (1982)

- 80386: Renamed the i386 because, you know, marketing people gotta do something. (1985)

- 80486: Officially named the i486, but no one cared and called it the 80486 anyway. (1989)

- 80586: Officially the Pentium 5 or P5, and bringing you the architecture of the first credible servers based on the X86 architecture. (1993)

- 80686: Pentium Pro (1995) and Pentium II (1997), called the P6 architecture internally.

- 80786: NetBurst or P68 architecture, used in Pentium 4 chips for desktops and servers. (2000)

- 80886: Core architecture (2006), the laptop saves the server day with the “Nehalem” Xeon E5500 (2009)

- 80986: Sandy Bridge architecture (2011)

- 81086: Haswell architecture (2013)

- 81186: Skylake architecture (2015)

- 81286: Ice Lake architecture (early 2021). Yes, that is a mighty big gap, but not as big as the one Intel left between the 32-bit Xeons and the 64-bit Itaniums that AMD drove a Sledgehammer, a Bulldozer, and a Piledriver through with the Opterons. The hole Intel left this time around with the Xeon SPs was Epyc enough, though, to point out that the Intel emperor was wearing a tankini like Borat. (No, you can’t unsee that image.)

- 81386: Sapphire Rapids architecture (late 2021)

- 81486: VMware represents a new architectural layer under Intel’s control and on top of X86. Maybe we call it 81ESX? (2022?)

Thanks for playing.

Maybe Michael Dell could buy Intel instead. Much simpler.

The thought had occurred to me. But why buy the whole cow when you can buy a rump roast….

Intel eight now is desperate. This is a seminal moment in history. Destroyed by Apple’s technological superiority, clobbered by AMD, Intel is being squeezed from all sides. It is time for Intel to give up the fight for X86. VMware has a future. Intel does not. This is reminiscent of the day IBM decided to stop making PC’s. Will Intel do the right thing ?

Intel had a choice between Moore’s law and x86. It wrongly picked x86 , maybe to please the board. It is irreparably damaged, the barbarians are in the building. It has one shot to redemption and Microsoft designing its own has opened this marriage for infidelity, i.e. acquisitions of the Vmware kind. But the question is what can it do to compete with Nvidia and all the fabless designers who will flood with market with chips.

Your architecture road map is a little off. After the 80486, Intel dropped that naming convention because they were contractually bound to share architectural information with competitors. By moving away from the 80×86 nomenclature, they were able to sidestep that obligation.

And I forced it right back in again as a joke. See?

Interesting.. but given Intel is signing up for $100++BILLION for 2-3yrs to try and catchup to AMD (Intel can’t yet do 7nm manufacturing !!?.. and next year’s CPU is STILL 10nm, while AMD will be at 5nm CPU’s !!).. they already have too much on their plate and DEBT. Dell never will, since they already have way too much DEBT on their plate from the EMC buy years back.. the reason why they are forced to sell VMware (and now EMC is DOA since storage is dying rapidly and moving to cloud or SDS, aka VMware vSAN..), so Dell would never want Intel (far behind AMD), nor more debt.

You neglected supply chain issues. Post-acquisition, Dell could (if they don’t already) get MFC (most favored customer) pricing from Intel for server & PC chips (CPUs & GPUs, and WifI, & Thunderbolt & vPro, etc., etc.) resulting in massive savings. What’s that worth to Dell to get better pricing from Intel than their rivals? And, Dell could also use that as leverage against AMD & Nvidia. INTC has been milking the cash cow that has been client for the past several years. They’ve been banking on server growth (esp. under Swan). Vertical integration on the design & sourcing of key components (see Apple) can be a big win.

If AMD and some ARM server/client vendors have competitive products to Intel and they treat the customers better ( no insider deals for Dell because they are a larger stockholder), then lower costs for Dell probably won’t help Intel overall stakeholders. Pretty likely even more customers will leave and “lower margin” Dell will represent an even larger share of the customer base.

That would good move to put more money in Micheal Dell’s pocket. Probably wouldn’t do much for the rest of Intel stockholders ( or employees long term) .

Even if Intel claws its way back into a position were not getting steady market share losses due to some major tech development leadership gap it is still unlikely to get back to the 2010’s status where vendors had to go on bended knee to grovel and beg favor of Intel. At best Intel can stop the “bleed” but are unlikely to recover all of the losses over the next 2-4 years.

( barring AMD and/or major ARM vendors majorly shooting themselves in the foot. More than one competitor means it is less likely that all of them stumble and fall flat so that Intel can easily just walk over them all. )

> What’s that worth to Dell to get better pricing from Intel than their rivals?

Dell doesn’t control Intel’s treasury. If Dell too their VMWare IPO money and plowed it into buy Intel share’s would that be a good way to get deeper disscounts? Probably not. Dell did sink gobs of money into buying Intel shares before and going forwarly likely isn’t any different.

Going the other way ( Intel dumping money into Dell’s pockets) doesn’t do a whole lot for Intel either. Trying to ‘buy’ captive customers usually doesn’t work well. Intel already tried that with the previous 3rd party foundry business with rather weak overall results. Another example, spending tons of money to buy Atom placement in very high mobility platforms didn’t work out for Intel in the long term either.

Dell ending up being a major stockholder is more about billionaire/”large company” personality status and that story’s “theme” of legacy players with the same name , than something substantive to Intel’s long term strategic interest.

Intel having a single customer as a major stockholder is a similar negative slippery slope as Nvidia owning ARM. That is going to generation blowback that there are special ‘insider’ deals and folks will go looking for other options if available. ( Nvidia is trying to negate that with ‘promises’ that they’ll let ARM operate independently. Unenforceable promises probalby isn’t going to cut it. )

Will kill intel even faster, all other PC vendors will abandon it right away and there are anti-trust laws and racketeering laws.

Well, as I was advising my Intel friends in both St Clara and Hillsboro 2 decades ago, they should’ve abandoned the sinking ship Itanic and pushed forward the superior Alpha architecture – you know, that Shenwei here in China, now with world’s first fully operational Exascale supercomputer, is “greatly inspired by Alpha” let’s put it this way. ISA choice does matter.

Your VMWare point actually makes a good strategic sense. Intel needs a major competitive advantage over AMD and Nvidia.

I lead the audit to assess Alpha in 1997 now under foundry responsibility of Samsung Semiconductor on acquisition from Compaq and all 400 participants involved in that 3 month audit supported continuation on examples of traction everywhere. All Samsung had to do was produce Alpha in volume in relation Drake, Tanner, Cascades and yes Cascades refers too “crush”. Unfortunately, Intel had already infiltrated Samsung Semiconductor on North 1st Street in San Jose through former employees aimed to put Alpha to bed, for Intel, parallel Ziff Davis engaged in systematic mass market destruction of Alpha through Ziff Davis lackey system integrator named Enorex. Samsung is not repeating that error on Ampere. mb

This two huge misadventures when it comes to strategic context.

1. Intel is committed to being in the leading edge fab business. Having approximately $8 billion in profit looks like a first class drunken sailor spending spree money right up until realize that a new 2-3nm fab is going to put Intel back about twice that amount ( at least). [ TSMC is spending $100B over next 2-3 years. Samsung another far larger than $8B . Intel continues to stumble they could be in 3rd place in high density , but also high volume business. ] Intel has triple digit Billion capital costs coming up over the next 4-6 years. Intel doesn’t have lots of excess cash with those kind of liabilities on the horizon. ( they will probably still do company acquisitions , just not very large ones. )

Sell off NAND for $9B and drop $10B on EUV fab expansion in AZ .. where is the huge pile of excess cash from that swap? Plus any possible clean up and factoring of the 3D Xpoint (Optane) business to something to better long term growth path ( less proprietary and broader industry competitive pressures to make it more resilent. Using Optane as a cash cow , higher margin crutch has worked for now, but going forward it highly likely won’t be as effective. ). Intel is *WAY* behind on capital spend on EUV fabrication infrastructure if they want to be a large volume player. And when you spend the money matters because can’t just arbitrarily buy bleeding edge EUV fab equipment on the spot market. If you don’t have money down on a future production slot. you’re not getting any. If Intel gets the kinks out of their 7nm (5nm) and can’t get equipment to do volume that isn’t going to be maximally productive.

This low synergy, tangent chasing is the same kind of “eye off the ball” strategy that assisted in digging the hole that Intel is in now. ( “We’ve got a 2 year fab process lead on everyone so let’s get distracted with other tangential shiny objects. ” ).

Intel doesn’t have a “how do we spend the extra money off the ‘print money machine’ ” problem anymore. Going forward the competition is steeper and the margins are going to feel some pressure. Grossly over paying for something just because they can is probably in the past for Intel. (at least until they fix some major issues. )

Intel couldn’t make the 3rd foundry business work so threw money at buying up FPGA, MobileEye, AI chips , etc. to herd business into the foundry. Buying VMWare largely smacks of the same mindset. Lacking in very clear ‘win-win’ synergies where would get more than additive impact on long term future revenues. Instead of fixing the core problem ( bad 3rd foundry biz approach), they just threw cash at captive customers to feed the broken biz. Intel needs to fix the core of the house with as much spending as necessary before going off into major acquisitions.

2. VMWare is also in a bit the inflection point zone. Seamlessly migrating VM images over almost completely homogeneous Intel x86-64 data center is easy. VMWare hasn’t really have a deep moat of a successful track record in highly heterogeneous hardware context. Additionally, more data center computational workload disappearing into DPUs (where VMWare isn’t a major player) also contributes to the inflection point. VMWare can make the transition to being multiple platform focused , but they need to build the appearance of being more hardware “neutral” rather than more single vendor focused.

Dell is separating at VMWare at a probably high point ( at least a local max in time) . They are “getting while the getting is good”. That doesn’t mean Intel should buy them ( at some substantive mark-up price).

VMWare has gone from propping up EMC stock price to propping up Dell stock price. Once VMWare gets independent, it is unclear why the stockholders with long term interest would want to jump back into a prop up some other stock duty. VMWare is at the point where more of their profits need to go into staying relevant in the core business they are in while that business goes through a major inflection point VMWare is also in the context going forward where it won’t have loads of “excess” profits to contribute to paying back for gross overspending of the parent company. (e.g., paying back what over paid for. )

Weaning off the VMWare cash cow is a good move for Dell/EMC (and silverlake). Milking a cash cow on a stable market is fine. Milking a cash cow on a shifting market is far more likely to kill the cow ( not a guarantee to kill the cow, but more risky than old status quo).

P.S. if Gelsinger is feeling nostalgic about running a Software company, then Intel has more software folks than AMD has hardware ones. There is a quite large software stack inside of Intel. ( different software than VMWare , but base infrastructure software ). Both the hardware and software stacks need work and attention. Taking a giant chunk of stockholder money to go buy your previous job really doesn’t bolster confidence in solving the problems in front of him. If he deson’t solve Intel’s core problematic issue buying VMWare probably won’t save Intel. It would likely just be money spent with low to negative return on investment.

Interesting analysis. Though the right play would be for Apple to buy VMware and not Intel imho. VMware has some nice hypervisor technology (helpful in dense data centers, yet not so necessary), in addition to a lot of acquired IP (which is mostly enterprise ‘bloatware’) – Intel buying VMware would be only an emotional decision from Pat, and as I know he is not too emotional. Apple has a lot of cash, and is lagging in providing enterprise solutions. Acquiring VMware’s aging customer base is one step, as is acquiring DropBox enterprise customers. If this is done, they will be at par with Microsoft.

Dell is already Intel’s largest stakeholder, first dib on every Intel next generation processor, preferential grade SKU access, volume allocation, del credere broker dealer to offset the cost : price of those components Dell wants for system integration in relation those secured in sales package as Intel close incentive for resale to others as Intel’s primary system and component sales department for three decades.

I think you need to give some consideration to the fact that Kubernetes and Docker are winning the very race VMWare started, I still don’t see the future value of this merger unless they want to become the IBM of x86 servers while the world moves on to containers. I am giving my opinion as an engineer.

Bulldozer came out around the same time as Sandy Bridge Xeon. 16bit 5200MT/s HyperTransport for 10GB/s I/O or 80 lanes of PCIe 3.0 for 80GB/s I/O (assuming a dual socket server). Not even a contest. Plus Intel 32nm has gate last (gloflo 32nm doesn’t) for much better power efficiency regardless of supposed comparable performance in some workloads. Hence Bulldozer quickly plummeted to 0 sales, right?

Not so crazy afterall, huh ? You had the semiconductor part of the equation correct as well 🙂

Hears hoping Intel wakes up and realizes they should be making this move afterall.