Open source hardware is something that is intellectually satisfying as well as economically rewarding, but it is clearly not something for everyone. At least not yet. But the Open Compute Project ecosystem that social network and hyperscale application provider Facebook started back in April 2011 has always taken the very long view, and infrastructure needs at telcos and other service providers as well as at the edge might do as much for open hardware adoption as the initial push by Facebook, early adoption by Rackspace Hosting and Goldman Sachs, and the big follow-up by Microsoft that both doubled the OCP ecosystem as well as forking it.

So how is that OCP ecosystem doing, nine years on? With IT organizations large and small being pretty conservative, about as good as can be expected but not as well as had been hoped by those who wanted to see “vanity free” and less expensive iron wash through the datacenters of the world. But, step by step, the OCP ecosystem keeps growing and improving on every key metric, and the base of customers and the amount of money that companies are spending on OCP iron – including servers, storage, switches, edge cell sites, and network interface cards – is also growing as a consequence.

Good luck trying to figure out how much, and the OCP market analysis and ecosystem provider survey done my Omdia (formerly IHS Markit) only provides some insight into what is happening in the market in that it does not include data about the OCP board members who are, entirely not coincidentally, the largest consumers of OCP gear: Facebook, Microsoft, Rackspace Hosting, Goldman Sachs, and Intel. (Those are in rough order of the consumption of servers. We talked to a bunch of people, and our best guesses are that Facebook consumed about 1 million OCP servers in 2019, and Microsoft did somewhere between 800,000 and 900,000 units. The numbers slip off very fast after that, and maybe the OCP board members consumed maybe 2.2 million units in total, with about 350,000 coming from Rackspace, Goldman Sachs, and Intel. There are probably another 400,000 units a year that come out of Facebook and Microsoft and are resold in third world countries through “renew” programs. The rest of the entire OCP market – the piece that the Omdia study focused on, which was unveiled at the recent virtual Open Compute Summit – is probably on the order of 400,000 units. Tops. Call it a cool 3 million units sold in 2019 for the sake of argument.

If these numbers are correct – and we are not suggesting that these are any more than estimates – then that means a few different things. First, that means that OCP gear represented about 25 percent or so of the 11.7 million server shipments in 2019. Second, it also means that actual OCP customers buying new iron accounted for maybe 10 percent of the base and another 16.7 percent or so of the base was for downstream users buying second-hand gear on the cheap. The other 73.3 percent slice of OCP server shipments were for the OCP board members mentioned above.

Don’t jump to the wrong conclusions. All OCP machines are by definition ODM machines, but not all ODM machines are OCP compliant, and moreover, not all hyperscalers and cloud builders and HPC centers and large enterprises buy all of their machines from the tradition ODMs like Quanta Computer, Foxconn, Inventec, WiWynn, Hyve Solutions, Jabil Circuit, and a handful of others. Some buy from a mix of ODMs and from the customizable portions of the OEMs (which Dell, Hewlett Packard Enterprise, Lenovo, and Inspur all have). In fact, for years ahead of when Facebook decided to go the Open Compute route, it was buying all of its machines custom made from Dell’s Data Center Solutions division, which we first wrote about in 2008 and which we profiled in-depth in 2012 shortly after the Open Compute Project was launched and when that unit was pushing more than $1 billion in iron.

If you look at the IDC data for server sales in 2019, the ODMs (as defined above) pushed 3.06 million units, or about 26 percent of the number of machines shipped worldwide, and that brought in $21 billion, or about 23.4 percent of the revenue. Obviously, the average selling price of the ODM machines is a bit lower, given the volumes and the usually vanity free nature of the machines, which don’t tend to have expensive baseboard management controllers or RAID controllers or anything extraneous like an enterprise server, which might be the datacenter for a particularly application and is therefore more of a pet than a cow, as they say in the datacenter server farm lingo. The 2018 ODM figures from IDC were almost the same, $21 billion for 11.8 million units, and 2017 was a lot smaller for the ODMs at $14.8 billion against 10.2 million units.

You might be thinking, then, that the ODMs account for most of the OCP sales. Not so fast there, iron horses. A fair amount of the hyperscalers and cloud builders, and a bunch of service providers a little less than that scale, buy from Supermicro, which is sometimes and OEM and sometimes an ODM and which has IBM Cloud as its biggest customer, or from the OEMs as we pointed out. Baidu and Tencent buy from Inspur, Tencent and Microsoft buy from Dell, HPE is still selling its own hyperscale designs to companies like eBay, and so forth. The ODMs as characterized by IDC are a proxy for the hyperscalers and cloud builders, but they are not the totality of what the Super 8 and their peers are doing. And the data presented by Omdia is not the totality of what the Open Compute ecosystem is doing.

But we can bridge some of the numbers. Follow along.

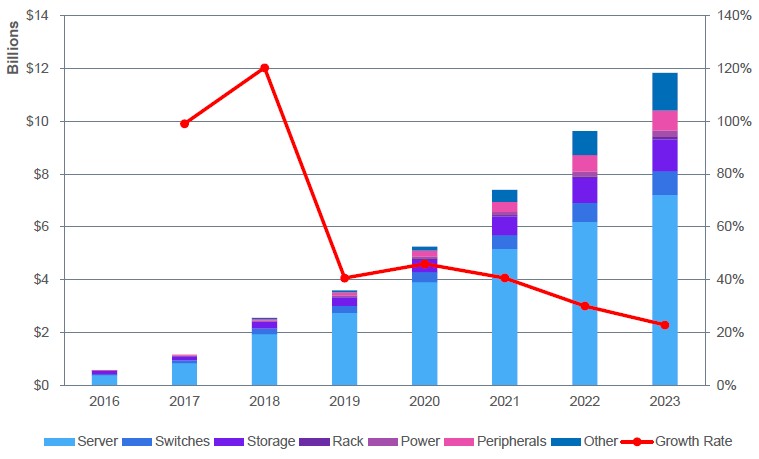

Let’s dig into the Omdia data presented at the most recent Open Compute Summit by Cliff Grossner, executive director of research and analysis, and Vlad Galabov, principal analyst. More than $1 billion in servers, storage, network, rack, power, peripherals, and other gear was sold in 2018 for the non-board members, according to their market casing across the OCP ecosystem. It looks like about $2.6 billion in the latest model and forecast, which is shown below, with servers being slightly less than $2 billion of that. In 2019 it grew to $3.6 billion. The researchers reckon that this represented 2.25 percent of the $160 billion in total market. Now, here is the breakdown of OCP non-board sales by product type:

If you look at those numbers above, a couple of things pop out. The first is that OCP iron outside of the board adopters – mostly Facebook and Microsoft, who contribute most of the server designs – was growing very fast from small numbers in 2017 and 2018 but growth rates moderated in 2019 and are expected to rise a bit in 2020, oddly enough, and then as the market grows, the pace of growth will slow as many markets do as they reach their natural levels. We will consider the forecast further in a moment, but right now we are looking at server sales for 2019, which were about $2.8 billion for the non-board members.

Now, assume that Facebook and Microsoft and the other board members pay about what the other hyperscalers and cloud builders do, on average, given the similarity of their configurations and workloads. The average ODM machine cost $6,850 according to the IDC figures for server sales last year. So that is around $6.85 billion in servers for Facebook and another $5.8 billion for Microsoft. If you add up the rest of the 300,000 or so OCP servers we think were sold last year (not including the 500,000 takeouts from Facebook, Microsoft, Rackspace, and others that are renewed in third world countries) to the other OCP board members, that’s another $2 billion or so in sales. We can reverse that average ODM price into the OCP non-board buyers and find that around 400,000 servers were sold to them.

So, the entire OCP server ecosystem was about 2.6 million new units, or about 22.1 percent of units shipped last year, and it came to $17.45 billion for all of the machines, or about 19 percent of revenues. There are some very big error bars in some of these estimates, mind you, but no one else has brought all these numbers together to try to sort it. Our point is that the OCP should be bragging about the fact that around a fifth of the iron going into datacenters is being driven by OCP designs – not just talking about the non-board members. Their strategy with this market study that Omdia is commissioned to do makes Open Compute look weaker than it is. The OCP board could give the complete data set for the OCP ecosystem by presenting OCP board members as a group instead of carving then out of the data. It’s not very smart, and Omdia is just doing what it is paid to do, so the only people to blame are the secretive OCP board members who should know better. But they are a secretive lot about things that do not need to be hushed, and they would rather there be rough estimates than hard facts because that serves their competitive posturing needs.

That, ultimately, is what this is about. Yes, Facebook and Microsoft contribute. But they gain more than they give from this ecosystem that they have fostered, and they give more than most so they are, so it would seem, beyond any kind of rebuke. Not in The Next Platform. The server OEMs can’t make much in the way of profits in the enterprise anymore thanks to the ODMs and the margins they are willing to take, and the ODMs, whether or not they push OCP gear, probably are living on the edge and are definitely trying to move into the enterprise with their OCP gear to try to get some higher profits for all their effort. This suited the needs of the hyperscalers and cloud builders to undermine the whole OEM market and make it tougher for smaller companies – meaning the Global 20,000 – always have to pay a lot more money for iron, which in a world dominated by IT means they can never compete on iron. This is just another manifestation of might makes right, and you have to be clever with a product or service to overcome that. Thankfully, millions of people do that every day. At least with OCP, you get some of the benefit of Facebook’s and Microsoft’s might to wield against others in the competitive market of business.

That, more than anything else we think, is what is really propelling Open Compute, and it is why the ambitious forecast above for the non-board OCP equipment sales does not violate out sensibilities.

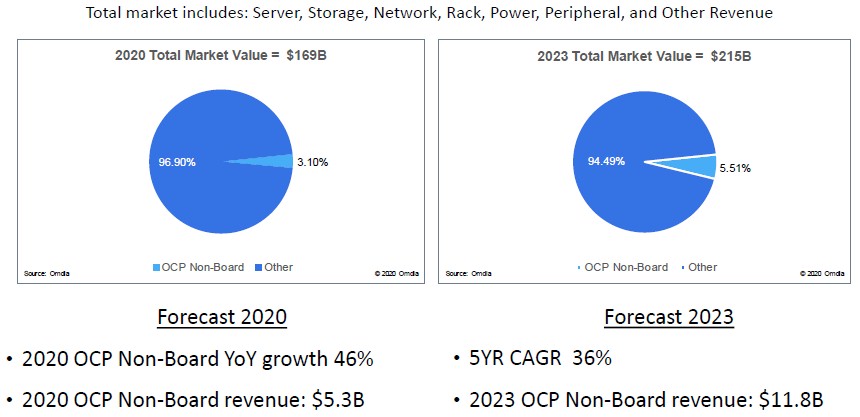

Across all the places where OCP designs and OCP supply chain partners play, Omdia believes that the total addressable market will expand by 5.6 percent but the OCP portion of that market will increase by 37.8 percent, or by a factor of 6.7X faster than the growth in the TAM, to reach $5.3 billion. And in the five years from 2019 and 2023, inclusive, the compound annual growth rate of 36 percent, the OCP share of datacenter and now edge spending will rise to 5.51 percent of a $215 billion market, or $11.8 billion in sales. The funny thing is that this will still be considerably lower than the $14.65 billion that the OCP board members spent on servers alone in 2019, by our estimates. The growth in OCP share is more than three times as high as in the TAM overall, which is also expanding in the market. And that, we think, is because OCP edge is taking off and telcos and other service providers are adopting OCP designs faster than enterprises are now expected to do. The optimism was high early on with large enterprises. The racks were just too weird.

And eventually, the hyperscalers and cloud builders in Asia/Pacific region – and particularly in China – are going to catch on to OCP. But there is every bit as good of a chance that the “Project Scorpio” rackscale computing effort from Alibaba, Baidu, and Tencent turns into its own Open Compute for China and finds its way into emerging markets in the Middle East, Africa, and South America. Why not? There can be more than one kind of Open Compute, as Facebook and Microsoft have demonstrated. And it doesn’t have to be done under Facebook’s and now Microsoft’s tent, although it might be. The possibilities are wide open.

WTF is ODM? Stop using acronyms and assuming everyone knows what they are.

Fair enough. But this one is not new, I did provide context, and we do have search engines. I will update for you.

This Wiki page has a pretty good definition of ODM: https://en.wikipedia.org/wiki/Original_design_manufacturer

In the future, please be more respectful when you ask a question. Mr. Morgan shares with us incredible tech insights on this site; let’s show some appreciation/respect.

I really liked the analysis you’ve provided, thank you for writing this!

I’m curious to what extent you believe that factoring in the non-server sectors of the OCP total revenue would shift the split in revenue between board members and non-members?

Not sure, but probably not by as much as we might think.